How to Qualify for a Mortgage: Step-by-Step Guide for Buyers

Almost half of all homebuyers admit that qualifying for a mortgage is more stressful than saving for a down payment. Understanding the steps to secure a mortgage can feel confusing, especially with strict income and debt guidelines in place. By breaking down each stage of the process, this guide gives you a clear roadmap to assess your readiness, organize your documents, and improve your approval chances with confidence.

Table of Contents

- Step 1: Assess Your Financial Readiness

- Step 2: Organize and Verify Documentation

- Step 3: Strengthen Your Credit Profile

- Step 4: Choose Suitable Mortgage Solutions

- Step 5: Submit and Track Your Application

Quick Summary

| Key Point | Explanation |

|---|---|

| 1. Assess Financial Readiness | Review your finances to determine mortgage eligibility and comfort in managing payments. |

| 2. Organize Key Documentation | Gather and systematically arrange financial documents for a clear application narrative, ensuring accuracy and completeness. |

| 3. Strengthen Your Credit Profile | Pay bills on time and reduce debt to enhance your credit score, which is vital for favorable mortgage terms. |

| 4. Choose the Right Mortgage | Evaluate various mortgage types to identify the best fit for your financial situation and future goals. |

| 5. Submit Application and Follow Up | Prepare a comprehensive application and maintain good communication with lenders to address any additional requests promptly. |

Step 1: Assess Your Financial Readiness

Qualifying for a mortgage starts with a comprehensive review of your financial health. This critical first step determines your borrowing potential and sets the foundation for a successful home purchase.

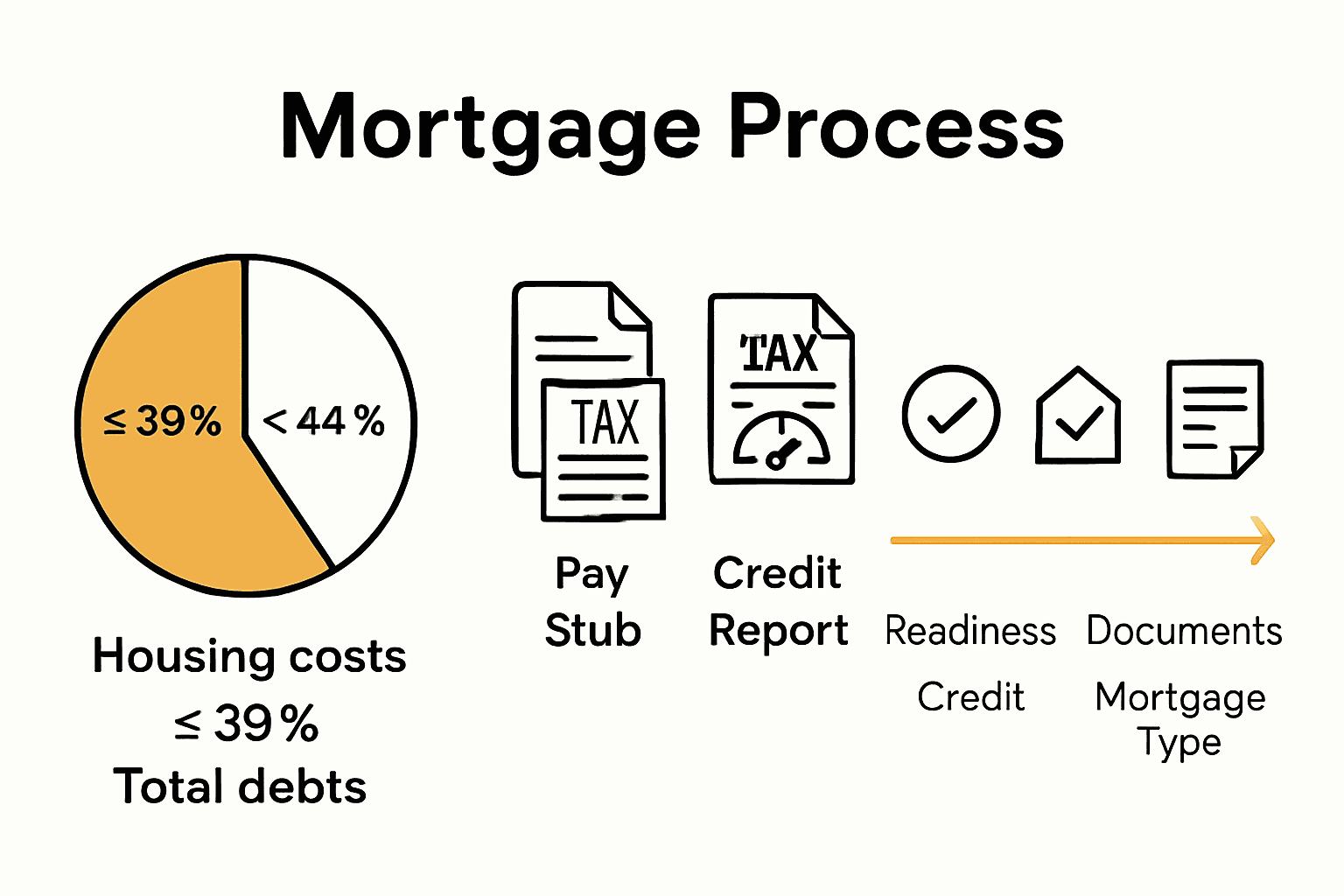

According to Canada.ca, prospective homebuyers need to carefully evaluate several key financial factors before applying for a mortgage. Your total monthly housing costs should not exceed 39% of your gross household income, and your overall debt load must remain under 44% of your gross income. These guidelines help ensure you can comfortably manage mortgage payments without financial strain.

To assess your financial readiness, start by gathering critical financial documents. This includes recent pay stubs, tax returns, bank statements, and a detailed record of your monthly expenses. Check your credit report for accuracy and review your credit score. According to Consumer Financial Protection Bureau, lenders typically look for consistent income over at least two years and a good credit history.

Pro Tip: Create a comprehensive budget that accounts for not just your potential mortgage payment, but also property taxes, homeowners insurance, potential maintenance costs, and utilities. This holistic approach will give you a realistic picture of your true housing expenses.

As you move forward, remember that financial readiness is about more than just meeting minimum requirements. It is about feeling confident and prepared to take on the responsibility of homeownership. The next step will involve calculating your exact borrowing capacity and understanding how lenders will evaluate your financial profile.

Step 2: Organize and Verify Documentation

Preparing a comprehensive and well-organized set of financial documents is crucial to streamlining your mortgage application process. This step transforms your financial story into a clear narrative that lenders will review and evaluate.

Consumer Financial Protection Bureau recommends gathering critical documentation that provides a complete picture of your financial health. Start by collecting the following key documents: recent pay stubs from the past two months, W2 forms or tax returns from the past two years, bank statements showing all account balances, documentation of additional income sources like bonuses or freelance work, and a detailed list of your current debts and monthly obligations.

Organize these documents systematically in a dedicated file or digital folder. Make sure all documents are current clean copies with no smudges or partial information. For digital files scan documents at high resolution and save them as PDFs to ensure clarity. Double check that your name social security number and other identifying information match exactly across all documents to prevent any potential verification issues.

Pro Tip: Create a checklist and verify each document against lender requirements. Some mortgage professionals recommend keeping digital and physical copies as a backup strategy in case of unexpected loss or technical issues.

Remember that thorough documentation demonstrates financial responsibility and can significantly speed up your mortgage approval process. The next step will involve understanding how lenders will scrutinize these documents and what specific details they will be analyzing.

Step 3: Strengthen Your Credit Profile

Strengthening your credit profile is a strategic process that can significantly improve your mortgage approval chances and potentially secure more favorable lending terms. This critical step involves carefully managing and improving your financial reputation.

According to CNBC Select, improving your credit score requires consistent financial discipline. Begin by ensuring all bill payments are made on time every single month. Late payments can dramatically reduce your credit score and signal potential risk to lenders. Focus on reducing existing debt, particularly credit card balances. Aim to keep your credit utilization below 30% of your total available credit limit.

Review your credit report meticulously for any potential errors or inaccuracies. Independent recommends obtaining a comprehensive credit report and carefully examining your financial history for the past five years. If you discover any discrepancies, contact the credit reporting agencies immediately to dispute and correct them. Adding a brief explanatory statement can provide context for any historical financial challenges.

Pro Tip: Avoid opening new credit accounts or making large purchases during the months leading up to your mortgage application. Each new credit inquiry can temporarily lower your credit score and potentially raise red flags for lenders.

Remember that building a strong credit profile takes time and consistent effort. Your goal is to demonstrate financial reliability and responsible credit management.

The next step will involve understanding how lenders specifically evaluate your credit worthiness and translate your credit score into lending terms.

Step 4: Choose Suitable Mortgage Solutions

Selecting the right mortgage solution is a critical decision that can impact your financial future for decades. This step involves carefully evaluating various mortgage types to find the perfect match for your unique financial situation and long-term goals.

Consumer Financial Protection Bureau advises prospective homebuyers to thoroughly assess how much they want to spend on a home and determine the most appropriate mortgage type. Consider fixed-rate mortgages for predictable monthly payments and stability, or adjustable-rate mortgages if you anticipate shorter-term ownership or expect potential income increases. Each mortgage type comes with unique advantages some offer lower initial rates while others provide long-term payment consistency.

Canada.ca emphasizes the importance of understanding how the mortgage stress test impacts your qualification. This means evaluating your ability to make payments at a higher interest rate than the current market rate. Compare different lenders mortgage offerings carefully look beyond just the interest rate and consider factors like prepayment options, penalty clauses, and overall loan flexibility.

Pro Tip: When exploring tailored financial solutions, request detailed loan estimates from multiple lenders. This allows you to compare true costs beyond just the advertised interest rates and understand the complete financial picture of each mortgage option.

Remember that the right mortgage solution is not just about finding the lowest rate but discovering a financial product that aligns with your personal financial strategy and future goals. The next step will involve getting pre-approved and solidifying your mortgage application.

Step 5: Submit and Track Your Application

Submitting your mortgage application marks a critical milestone in your home buying journey. This step transforms all your careful preparation into a tangible path toward homeownership.

Consumer Financial Protection Bureau recommends creating a comprehensive loan application packet that includes all essential documentation. Compile your documents meticulously ensuring each item is current and clearly legible. This includes recent pay stubs, tax returns from the past two years, comprehensive bank statements, proof of additional income sources, and detailed records of your existing debts.

When submitting your application, be prepared for potential additional requests from lenders. They might require supplemental documentation or clarification on specific financial details. Maintain open communication channels with your loan officer and respond promptly to any inquiries. Some lenders offer online portals where you can track your application status in real time allowing you to monitor progress and quickly address any potential issues.

Pro Tip: Consider using smart advice resources to understand the typical timeline and potential checkpoints in the mortgage approval process. This can help you set realistic expectations and stay proactively informed throughout the application review.

Remember that patience and persistence are key during the mortgage application process. Your thorough preparation has positioned you strongly for success. The next step involves preparing for the final stages of mortgage approval and potential home appraisal.

Take Control of Your Mortgage Journey with Expert Guidance

Qualifying for a mortgage can feel overwhelming with all the financial checks, credit reviews, and paperwork involved. You want to be ready and confident every step of the way. This guide highlights the key challenges buyers face like organizing documentation, improving credit scores, and choosing the right mortgage type. If you are ready to turn these challenges into opportunities, you need a partner who understands your unique situation and can offer tailored financial solutions.

At Craigburn Capital, we specialize in helping buyers like you navigate the complex mortgage process. Whether you are a first-time homebuyer, self-employed, or have less-than-perfect credit, we provide access to competitive rates and exclusive lending options designed for your needs. Don’t wait until paperwork stacks up or your credit concerns grow. Visit Craigburn Capital now to get personalized advice and step confidently toward your homeownership goals. Start your mortgage application with clarity and support today.

Frequently Asked Questions

What financial documents do I need to gather to qualify for a mortgage?

To qualify for a mortgage, you will need to gather recent pay stubs, tax returns from the past two years, current bank statements, and documentation of any additional income sources. Organize these documents neatly to present a clear financial picture to lenders.

How can I assess my financial readiness before applying for a mortgage?

Assess your financial readiness by calculating your total monthly housing costs and ensuring they do not exceed 39% of your gross household income. Create a detailed budget that includes all potential housing expenses to understand your financial capacity better.

What credit score do I need to qualify for a mortgage?

While specific score requirements can vary, aim for a minimum credit score of 620 to increase your chances of qualifying for a mortgage with favorable terms. Check your credit report for any inaccuracies and take steps to improve your credit profile by paying bills on time and reducing existing debts.

How do I choose the right mortgage type for my needs?

To choose the right mortgage type, evaluate whether a fixed-rate mortgage or an adjustable-rate mortgage best suits your financial situation and future plans. Consider factors like potential interest rate fluctuations and your intended length of homeownership to make an informed decision.

What steps should I take after submitting my mortgage application?

After submitting your mortgage application, maintain open communication with your loan officer and be prepared to provide any additional documentation if requested. Use online tracking tools offered by lenders to monitor your application’s progress and respond promptly to any inquiries.

How long does the mortgage approval process typically take?

The mortgage approval process typically takes between 30 to 60 days, depending on the lender and the complexity of your application. Stay proactive by regularly checking in with your loan officer to anticipate any potential delays and prepare accordingly.