Master the Commercial Property Loan Process 2025

Every American commercial property investor knows the pressure when financing demands rise and deals get more complex. With markets tightening and lender standards evolving for 2025, missing a single detail can cost you thousands or jeopardize closing. Over 80 percent of commercial loan applications face additional scrutiny under stricter underwriting rules. If you want strategic guidance to secure funding, this article outlines the essential steps for building lender trust and completing smooth transactions even when your portfolio needs are far from simple.

Table of Contents

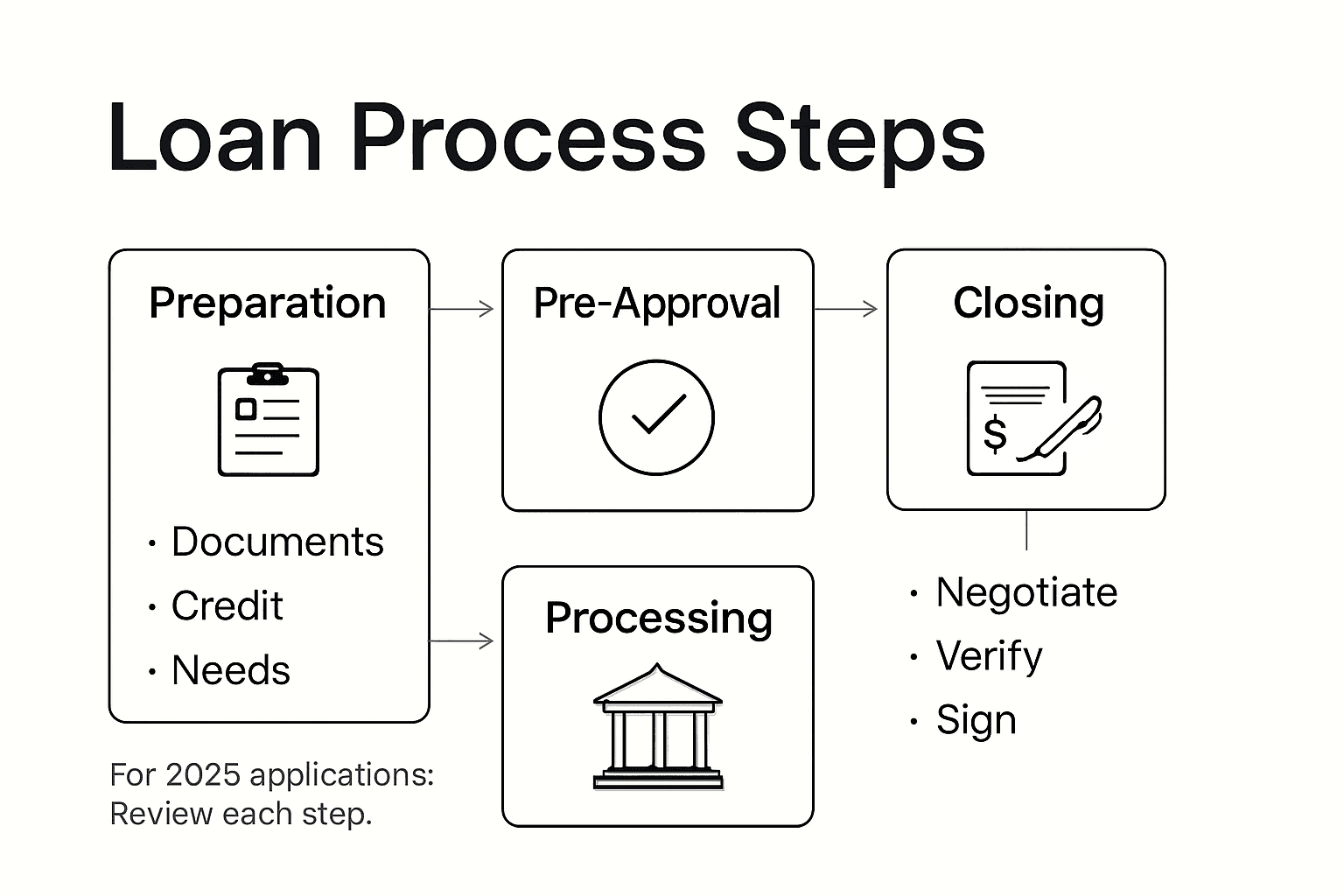

- Step 1: Assess Financial Readiness And Property Needs

- Step 2: Compile Required Documents And Credit Reports

- Step 3: Select Potential Lenders And Compare Offers

- Step 4: Submit Applications And Negotiate Terms

- Step 5: Complete Due Diligence And Finalize Closing

Quick Summary

| Key Insight | Explanation |

|---|---|

| 1. Assess Financial Readiness First | Conduct a thorough financial analysis to understand your investment capability and align with lender expectations. |

| 2. Compile Comprehensive Documentation | Gather all necessary financial records and credit reports to showcase your lending worthiness to potential lenders. |

| 3. Compare Different Lenders | Research and compare lenders based on interest rates, loan terms, and conditions to find favorable financing options. |

| 4. Negotiate Loan Terms Advantageously | Approach negotiations collaboratively to secure optimal loan conditions that align with your investment strategy. |

| 5. Complete Due Diligence and Closing | Ensure meticulous verification of all transaction elements to guarantee legal security and financial reliability before closing. |

Step 1: Assess financial readiness and property needs

Successfully navigating commercial property financing starts with a comprehensive financial and property needs assessment. This crucial step helps you understand your investment potential and align your goals with lender expectations.

Begin by conducting a thorough financial viability analysis that examines your current financial standing. Evaluate key metrics including your credit score, existing debt levels, income stability, and cash reserves. Lenders will scrutinize these factors to determine your borrowing capacity and risk profile. Focus on documenting stable income streams, minimizing outstanding debts, and maintaining strong credit history.

Next, perform a rigorous commercial property needs assessment that aligns your investment objectives with potential property characteristics. Analyze market conditions, location potential, operational requirements, and scalability. Consider factors like property type, intended use, potential rental income, maintenance costs, and long term appreciation potential. This strategic approach ensures you select properties that match both your immediate financial constraints and future growth strategies.

Pro tip: Create a detailed financial readiness portfolio that includes tax returns, bank statements, investment records, and property investment business plan to demonstrate comprehensive preparedness to potential lenders.

Step 2: Compile required documents and credit reports

Preparing a comprehensive document package is critical for successfully securing a commercial property loan. This step involves gathering detailed financial records and credit documentation that lenders will use to evaluate your lending worthiness.

Start by assembling a systematic legal documentation checklist that covers all essential loan requirements. Your documentation package should include personal and business tax returns for the past three years, comprehensive financial statements, profit and loss records, and detailed balance sheets. Obtain official credit reports from all three major credit bureaus to understand your complete credit profile. Request a comprehensive business credit report that provides insights into your company financial history and creditworthiness.

Ensure you have supporting documentation like bank statements, investment account records, existing lease agreements, and proof of income. Organize these documents chronologically and create digital and physical copies for easy reference. Lenders will scrutinize these materials to assess your financial stability, income consistency, and ability to manage commercial property investments.

Pro tip: Digitize all financial documents and create a secure cloud backup to ensure quick retrieval and protect against potential loss during the loan application process.

Step 3: Select potential lenders and compare offers

Selecting the right commercial property lender can make or break your investment strategy. This critical step requires strategic research and careful comparison of multiple financing options to secure the most favorable terms for your specific investment goals.

Begin by exploring comprehensive commercial real estate loan options across different lender categories. Traditional banks, credit unions, Small Business Administration (SBA) programs, and alternative lenders each offer unique advantages. Evaluate each lender based on key criteria including interest rates, loan terms, maximum loan to value ratios, approval speed, and flexibility in underwriting standards. Pay close attention to specialized programs that might align with your specific property type or investment profile.

Create a detailed comparison spreadsheet that tracks interest rates, loan fees, prepayment penalties, loan duration, and qualification requirements for each potential lender. Request official loan estimates from multiple sources to understand the full financial landscape. Consider factors beyond just the interest rate including customer service reputation, experience with commercial property investments, and potential future banking relationship opportunities. Prioritize lenders who demonstrate a nuanced understanding of your specific investment strategy and show willingness to customize loan structures to meet your unique needs.

Pro tip: Schedule initial consultations with at least three different lenders and request comprehensive loan estimates to gain a comprehensive understanding of your financing options.

Use this table to compare common lender types for commercial property loans:

| Lender Type | Typical Loan Range | Approval Speed | Flexibility |

|---|---|---|---|

| Traditional Bank | $500K–$20M+ | Weeks | Strict policies |

| Credit Union | $250K–$10M | Weeks | Relationship-based decisions |

| SBA Program | $50K–$5M | Months | Special incentives, strict rules |

| Alternative Lender | $100K–$10M | Days | High speed, more lenient criteria |

Step 4: Submit applications and negotiate terms

Submitting commercial property loan applications requires strategic precision and careful preparation. This stage transforms your financial groundwork into actual funding opportunities and demands a calculated approach to presenting your investment potential.

Begin by understanding the comprehensive commercial loan application and negotiation process, which involves multiple intricate steps beyond simple paperwork submission. Carefully prepare your application package, ensuring every document is meticulously organized and presents a compelling narrative about your investment strategy. Include detailed property appraisals, comprehensive financial statements, projected income analysis, and a clear business plan that demonstrates your ability to generate consistent revenue and manage the proposed property effectively.

When entering negotiations, approach the process as a collaborative partnership rather than an adversarial transaction. Focus on material terms that significantly impact your financial flexibility, such as interest rates, prepayment penalties, loan duration, and covenant requirements. Be prepared to discuss and potentially compromise on specific terms while maintaining clear boundaries about your core financial objectives. Request a formal term sheet that outlines all proposed conditions, and carefully review each clause to understand potential long term implications for your investment strategy.

Pro tip: Consider hiring a commercial real estate attorney to review loan documents and help you negotiate terms that protect your financial interests and minimize potential future risks.

Step 5: Complete due diligence and finalize closing

The final stage of your commercial property loan journey demands meticulous attention to detail and comprehensive verification of all transaction elements. This critical phase transforms your potential investment into a legally binding and financially secure acquisition.

Begin by executing a comprehensive commercial real estate closing checklist that systematically verifies every aspect of the transaction. Conduct thorough property inspections, including structural assessments, environmental evaluations, zoning compliance reviews, and detailed title searches. Verify all financial documentation, ensuring absolute alignment between your loan terms, property valuation, and investment projections. Pay special attention to legal compliance requirements, entity authority verification, and potential encumbrances that could impact your future property ownership.

Collaborate closely with your legal and financial advisors during the closing process to review all final documents and ensure complete understanding of your contractual obligations. Carefully examine the closing statement, loan documents, title insurance policies, and any recorded agreements. Confirm that all negotiated terms are accurately reflected in the final paperwork, and do not hesitate to request clarification on any points that seem unclear or potentially problematic. Prepare all required funds for closing, including down payments, closing costs, and any additional fees specified in your loan agreement.

Pro tip: Request a final walk through of the property immediately before closing to confirm its condition matches the initial inspection and verify no unexpected changes have occurred since your initial assessment.

Here’s a quick overview of key steps and their objectives in commercial property financing:

| Step | Primary Objective | Success Indicator |

|---|---|---|

| Assess Readiness | Identify financial health | Clear investment potential |

| Compile Documents | Prepare complete application | All lender requirements met |

| Compare Lenders | Find best loan terms | Favorable rates and flexibility |

| Negotiate Terms | Secure optimal conditions | Terms align with goals |

| Due Diligence & Closing | Ensure legal and financial security | Smooth, compliant transaction completion |

Take Control of Your Commercial Property Financing Today

Mastering the commercial property loan process involves more than understanding financial readiness and lender comparisons. You need expert guidance to confidently navigate complex applications and negotiate terms that protect your investment goals. If you are facing challenges like compiling exhaustive documentation, selecting the right lender, or ensuring a smooth closing, Craigburn Capital is here to simplify every step.

With specialized expertise in commercial financing, Craigburn Capital offers tailored mortgage solutions designed to meet your specific financial situation. Whether you are self-employed, have less-than-perfect credit, or seek exclusive competitive interest rates, our team can empower you with personalized advice and access to private lending options. Don’t let uncertainty delay your investment success. Visit Craigburn Capital now to explore how our dedicated professionals can help you unlock financing opportunities and bring your commercial property ambitions to life. Start your journey with confidence by reviewing our comprehensive resources and speaking directly with an expert today.

Frequently Asked Questions

How can I assess my financial readiness for a commercial property loan?

To assess your financial readiness, conduct a financial viability analysis that examines your credit score, existing debt levels, income stability, and cash reserves. Document key financial metrics to demonstrate your stability to potential lenders.

What documents do I need to compile for a commercial property loan application?

You need to compile personal and business tax returns for the past three years, comprehensive financial statements, profit and loss records, and your credit reports. Organize these documents carefully to present a complete and compelling case for your loan application.

How do I compare different lenders for commercial property loans?

To effectively compare lenders, explore different types of financing options including traditional banks, credit unions, and alternative lenders. Create a spreadsheet tracking key criteria such as interest rates, loan fees, and approval speed to facilitate an informed decision.

What should I include when negotiating terms with lenders?

During negotiations, focus on material terms that impact your financial flexibility, such as interest rates, loan duration, and prepayment penalties. Prepare to discuss your investment goals and potential compromises, making sure to protect your core financial objectives.

What steps should I take during the due diligence process before closing?

During due diligence, verify all aspects of the transaction by conducting property inspections and ensuring alignment between loan terms and property valuation. Collaborate with legal and financial advisors to review all final documents for compliance and clarity.

How can I ensure a smooth closing process for my commercial property loan?

To ensure a smooth closing process, prepare all required funds, including down payments and closing costs, in advance. Conduct a final walkthrough of the property just before closing to confirm its condition matches your expectations.