First-Time Homebuyer Assistance: Unlocking Homeownership

Over half of American renters believe owning a home is out of reach, yet more options exist than many realize. As housing prices rise, the gap between dreams and reality can feel huge for first-time buyers. First-time homebuyer assistance programs offer vital support that helps American families move from renting to owning. By demystifying these programs, you open the door to life-changing benefits and smarter financial decisions.

Table of Contents

- Defining First-Time Homebuyer Assistance Programs

- Main Types of Homebuyer Assistance Available

- Eligibility Rules and Application Process Explained

- Financial Benefits and Long-Term Implications

- Common Pitfalls and How to Avoid Them

Key Takeaways

| Point | Details |

|---|---|

| First-Time Homebuyer Assistance Programs | Designed to make homeownership attainable by providing financial and educational support to new buyers. |

| Types of Assistance Available | Includes government loans, down payment assistance, tax credits, and occupation-based benefits targeting various demographics. |

| Eligibility Requirements | Applicants must meet specific income, credit score, and educational criteria that vary by program. |

| Common Pitfalls | Prospective buyers should avoid incomplete documentation and misunderstanding program requirements to ensure a successful application. |

Defining First-Time Homebuyer Assistance Programs

First-time homebuyer assistance programs represent strategic financial initiatives designed to transform homeownership dreams into achievable realities. These programs are specifically crafted to support individuals entering the housing market for the first time, providing critical resources that bridge financial gaps and educational barriers.

At their core, first-time homebuyer assistance programs offer comprehensive support through multiple channels. Typical benefits include down payment assistance, reduced interest rates, educational workshops, and specialized mortgage products tailored to new homeowners. These programs recognize that purchasing a first home involves more than financial transactions—they aim to empower buyers with knowledge and financial tools.

The key components of most first-time homebuyer assistance programs generally encompass:

- Financial Grants: Direct monetary support for down payments and closing costs

- Low-Interest Loans: Specialized mortgage products with favorable terms

- Credit Counseling: Free or reduced-cost guidance on improving creditworthiness

- Educational Resources: Workshops and seminars about home purchasing processes

- Flexible Qualification Standards: More inclusive eligibility requirements compared to traditional lending

By providing these multifaceted support mechanisms, first-time homebuyer assistance programs play a crucial role in expanding homeownership opportunities. They transform what might seem like an insurmountable financial challenge into an achievable milestone for many aspiring homeowners.

Main Types of Homebuyer Assistance Available

Government-backed loan programs represent one of the most comprehensive approaches to helping first-time homebuyers navigate the complex real estate landscape. These specialized financing options provide critical support by offering more flexible qualification standards, reduced down payment requirements, and favorable interest rates designed to make homeownership more accessible to individuals who might struggle with traditional mortgage parameters.

The primary types of homebuyer assistance available encompass several strategic financial support mechanisms. These diverse programs include:

- Government Loans: FHA, VA, and USDA loans with unique benefits

- Down Payment Assistance: Direct grants and low-interest loans for initial home purchase costs

- Tax Credits: Financial incentives that reduce overall home buying expenses

- Matched Savings Programs: Initiatives that multiply personal savings for home purchases

- Educational Resources: Free counseling and home buying workshops

- Occupation-Based Benefits: Special programs for specific professional groups

Unique assistance opportunities extend beyond traditional financing, with nonprofit and faith-based organizations also offering targeted support. These programs recognize that financial barriers can prevent talented, responsible individuals from achieving homeownership. By providing comprehensive assistance—ranging from monetary support to educational resources—these initiatives transform homeownership from an intimidating challenge into a realistic goal for many aspiring homeowners.

Eligibility Rules and Application Process Explained

Navigating the eligibility requirements for first-time homebuyer assistance programs demands careful preparation and understanding of complex financial criteria. Most assistance programs establish specific parameters that applicants must meet, including income thresholds, credit score minimums, and first-time homebuyer status verification.

Typical eligibility requirements generally encompass several key components:

- Income Limits: Strict household income ranges that vary by program

- Credit Score Requirements: Minimum credit scores typically between 620-680

- First-Time Buyer Definition: Usually meaning no home ownership in the past three years

- Residency Status: Proof of legal citizenship or permanent residency

- Homebuyer Education: Mandatory completion of approved housing counseling courses

- Property Restrictions: Limitations on home type, purchase price, and intended use

The application process for homebuyer assistance involves multiple strategic steps. Prospective buyers must compile comprehensive documentation including tax returns, employment verification, bank statements, and detailed financial history. Successful applicants typically demonstrate financial stability, responsible credit management, and a genuine commitment to homeownership through their comprehensive application package.

Unique programs often have nuanced qualification criteria that extend beyond basic financial metrics. Some initiatives target specific professional groups, provide additional support for first-generation homebuyers, or offer specialized assistance for individuals in critical community service roles. Understanding these intricate details can significantly enhance an applicant’s chances of securing valuable homebuyer assistance and transforming their homeownership aspirations into reality.

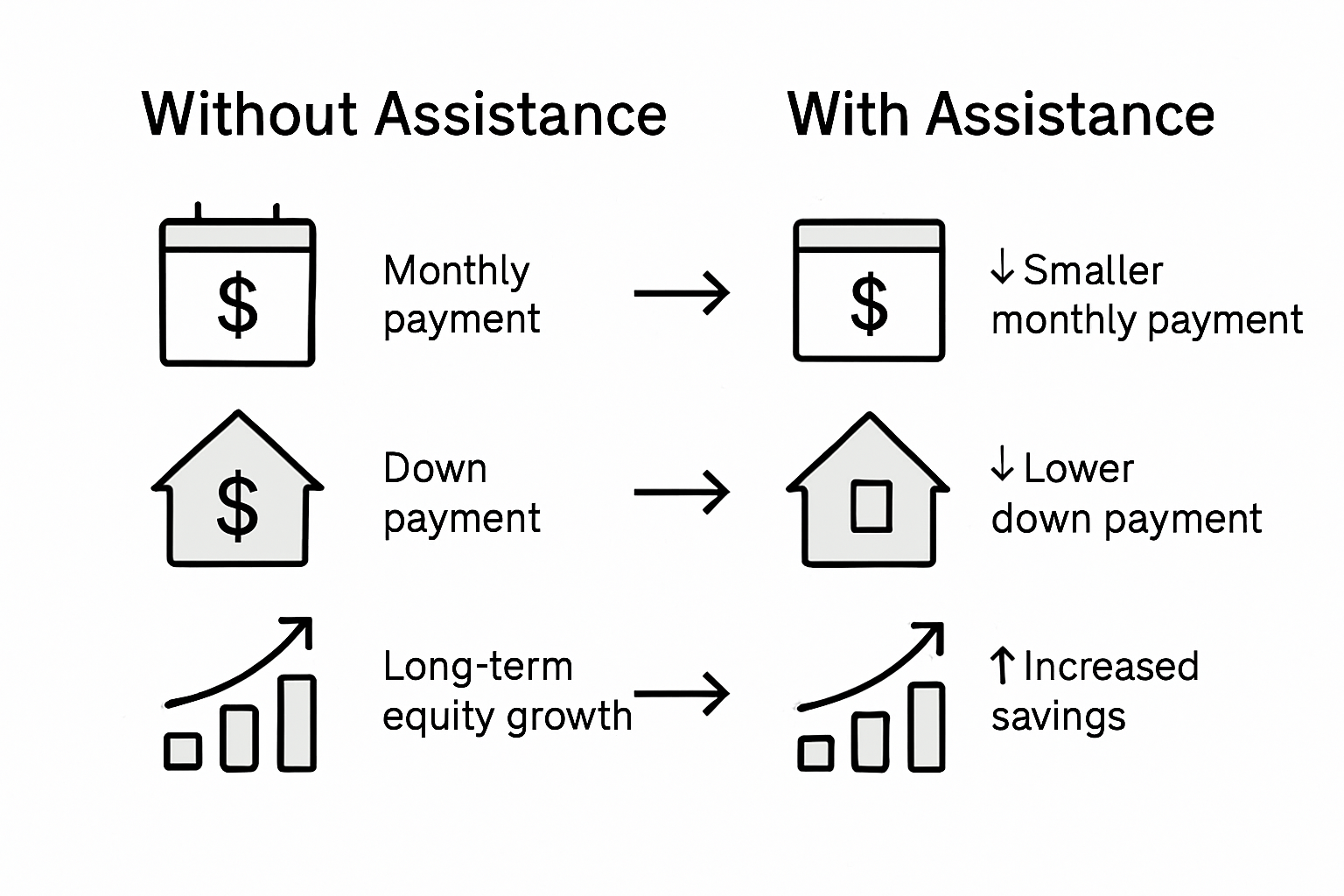

Financial Benefits and Long-Term Implications

Government loan programs unlock substantial financial advantages that extend far beyond initial home purchase support. These specialized initiatives provide first-time homebuyers with strategic opportunities to build wealth, reduce upfront costs, and establish a robust financial foundation through carefully designed assistance mechanisms.

The primary financial benefits of homebuyer assistance programs include:

- Reduced Down Payment Requirements: Minimizing initial cash outlays

- Lower Interest Rates: Decreasing long-term borrowing expenses

- Tax Credit Opportunities: Generating additional financial savings

- Equity Building: Accelerating personal wealth accumulation

- Credit Score Improvement: Establishing positive financial history

- Mortgage Insurance Waivers: Reducing ongoing monthly expenses

Long-term financial implications require careful consideration beyond immediate monetary benefits. Potential homebuyers must evaluate program-specific requirements, potential repayment obligations, and the broader impact on personal financial trajectories. Some assistance programs may include contingencies like residency requirements, income restrictions, or mandatory holding periods that could influence future financial flexibility.

Beyond immediate financial relief, these programs represent strategic investments in personal economic empowerment. By providing accessible pathways to homeownership, first-time homebuyer assistance transforms what might seem like an insurmountable financial challenge into a realistic opportunity for building generational wealth and long-term financial stability.

Common Pitfalls and How to Avoid Them

First-time homebuyer assistance programs offer incredible opportunities, but navigating their complex landscape requires strategic awareness and proactive planning. Potential homebuyers must remain vigilant about potential challenges that could derail their homeownership dreams or create unexpected financial complications.

The most critical pitfalls first-time buyers should anticipate include:

- Incomplete Documentation: Failing to prepare comprehensive financial records

- Credit Score Mismanagement: Neglecting credit health before application

- Overlooking Hidden Costs: Underestimating expenses beyond mortgage payments

- Program-Specific Restrictions: Misunderstanding eligibility requirements

- Inadequate Financial Planning: Stretching budget beyond sustainable limits

- Rushing the Application Process: Submitting incomplete or inaccurate information

Successful navigation of homebuyer assistance requires meticulous preparation and a comprehensive understanding of program nuances. Prospective buyers should invest time in financial counseling, thoroughly research available programs, and develop a strategic approach that addresses potential weaknesses in their application profile. This proactive strategy involves maintaining stable employment, minimizing debt, and building a robust savings history that demonstrates financial responsibility.

Ultimately, avoiding common pitfalls demands a combination of education, patience, and strategic financial management. By approaching homebuyer assistance programs with careful planning and a detailed understanding of potential challenges, first-time buyers can transform potential obstacles into stepping stones toward successful homeownership.

Take the First Step Toward Homeownership with Expert Mortgage Solutions

Navigating the complex world of first-time homebuyer assistance programs can feel overwhelming. You may be dealing with tight income limits, credit score requirements, or the challenge of completing all necessary documentation. Understanding terms like down payment assistance, low-interest loans, and homeowner education workshops is critical but often confusing. At Craigburn Capital, we specialize in transforming these challenges into opportunities by offering personalized mortgage solutions tailored specifically for first-time buyers facing these hurdles.

Do not let the fear of paperwork or financial barriers hold you back. Visit Craigburn Capital now to explore how our competitive rates and exclusive programs can unlock your path to homeownership. Our experienced team provides free resources and strategic advice that empower you to avoid common pitfalls and maximize every available assistance program. Take control of your future today by contacting us and discovering options designed just for you.

Frequently Asked Questions

What are first-time homebuyer assistance programs?

First-time homebuyer assistance programs are financial initiatives designed to help individuals buy their first home. They typically offer down payment assistance, reduced interest rates, educational workshops, and specialized mortgage products tailored for new homeowners.

What types of assistance are available for first-time homebuyers?

Types of assistance often include government-backed loans (like FHA, VA, and USDA loans), down payment assistance grants, tax credits, matched savings programs, educational resources, and benefits for specific occupations.

What are the common eligibility requirements for these assistance programs?

Eligibility requirements usually include strict income limits, minimum credit score thresholds (generally between 620-680), proof of first-time buyer status, residency status, and completion of homebuyer education courses.

How can first-time homebuyer assistance programs benefit me financially in the long term?

These programs can lead to reduced down payment requirements, lower interest rates, tax credits, and help in building equity. They also provide opportunities for improved credit scores, which can significantly impact your financial growth over time.