Complete Guide to Guidelines for First-Time Buyers

Over 40 percent of american first-time buyers mistakenly believe they need a massive down payment before purchasing a home. Myths like this add to the stress of buying a house for the first time, making the process seem almost out of reach. Understanding what really defines a first-time buyer and setting aside these common misconceptions can help you approach homeownership with confidence and clarity right from the start.

Table of Contents

- Defining First-Time Buyers And Common Myths

- Types Of Mortgages Available Today

- Eligibility Criteria And Pre-Approval Process

- Essential Steps In The Homebuying Journey

- Financial Responsibilities And Hidden Costs

- Avoiding Common First-Time Buyer Mistakes

Key Takeaways

| Point | Details |

|---|---|

| Understanding First-Time Buyers | First-time buyers often lack real estate experience and are more price-sensitive, making them seek comprehensive mortgage guidance. |

| Mortgage Options | Various mortgage types, such as FHA, VA, and conventional loans, provide diverse down payment options, enabling accessibility to homeownership. |

| Pre-Approval Importance | The pre-approval process is essential for assessing purchasing potential and understanding maximum loan amounts and interest rates. |

| Financial Responsibilities | Homeownership entails ongoing costs beyond the mortgage, including taxes, insurance, and maintenance, emphasizing the need for thorough financial planning. |

Defining First-Time Buyers And Common Myths

A first-time buyer represents an individual taking their initial step into homeownership, a significant milestone that comes with unique opportunities and challenges. According to Wikipedia, first-time buyers are typically favored in real estate markets across the United States, Canada, and other countries due to their absence of a property chain, which can simplify transaction processes.

Contrary to popular belief, becoming a first-time homebuyer isn’t as intimidating as many assume. Brookfield Residential highlights one prevalent myth: the misconception that a 20% down payment is mandatory. In reality, numerous lenders now offer mortgage options with significantly lower down payment requirements, making homeownership more accessible than ever before.

Key characteristics of first-time buyers often include:

- Limited prior real estate investment experience

- Higher likelihood of seeking comprehensive mortgage guidance

- More price-sensitive compared to experienced property investors

- Increased interest in starter homes and more affordable property segments

Understanding these nuances can help prospective homebuyers navigate the complex landscape of real estate transactions more confidently. While the journey might seem overwhelming, partnering with experienced mortgage professionals can transform this potentially stressful experience into an exciting adventure toward building personal wealth and securing a permanent residence.

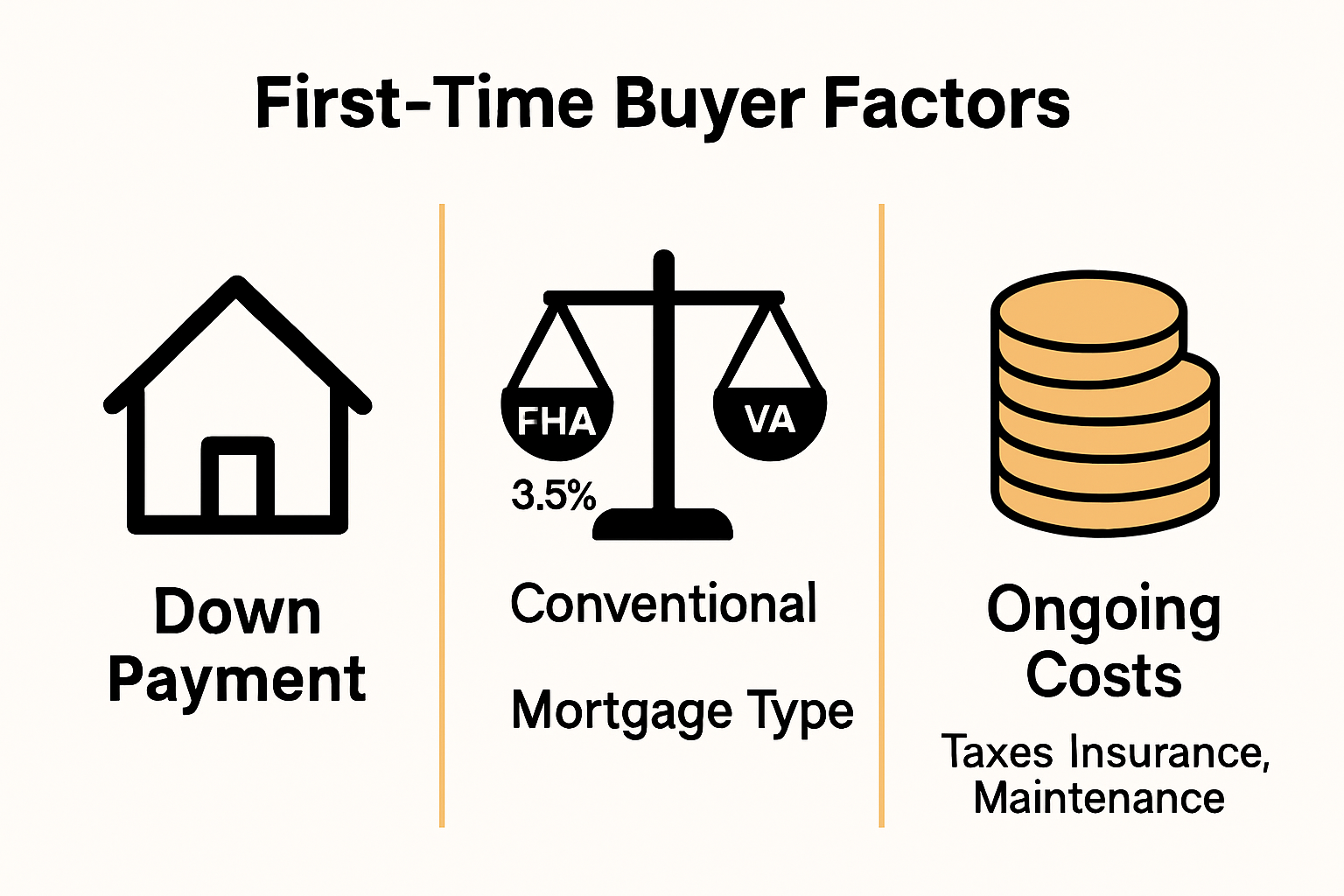

Types Of Mortgages Available Today

Navigating the mortgage landscape can feel complex, but understanding the available mortgage types empowers first-time homebuyers to make informed decisions. Richmond American highlights several accessible mortgage options designed to accommodate diverse financial situations and buyer needs.

The primary mortgage categories include conventional loans, FHA loans, and government-backed mortgage programs. Conventional loans typically require stronger credit profiles, while FHA loans offer more flexible qualification standards. According to Richmond American, FHA loans can be obtained with as little as 3.5% down payment, and VA loans provide zero down payment options for eligible veterans.

Mortgage options for first-time buyers often feature unique advantages:

- Conventional Loans: Standard mortgages with competitive interest rates

- FHA Loans: Lower down payment requirements, more lenient credit standards

- VA Loans: Exclusive to veterans, featuring no down payment

- USDA Loans: Rural property financing with potential zero down payment

- First-Time Homebuyer Programs: Special state and federal assistance initiatives

While each mortgage type presents distinct benefits, selecting the right option depends on individual financial circumstances, credit history, and long-term homeownership goals. Consulting with a mortgage professional can help buyers identify the most suitable mortgage strategy tailored to their specific needs.

Learn more in our guide to mortgage qualification, which provides comprehensive insights into navigating these complex financial decisions.

Learn more in our guide to mortgage qualification, which provides comprehensive insights into navigating these complex financial decisions.

Eligibility Criteria And Pre-Approval Process

The mortgage pre-approval process represents a critical milestone for first-time homebuyers, serving as a strategic financial assessment that determines purchasing potential. International Journal of Scientific Research and Management highlights that first-time buyers often struggle with understanding the intricate requirements and financial evaluations involved in mortgage eligibility.

To qualify for a mortgage, lenders typically examine several key financial indicators. These include credit score, income stability, debt-to-income ratio, employment history, and available savings. Most lenders prefer a credit score of 620 or higher for conventional loans, though some programs accommodate lower scores with additional requirements. The pre-approval process involves a comprehensive financial background check that helps determine the maximum loan amount and potential interest rates a buyer might qualify for.

Critical eligibility factors for mortgage pre-approval include:

- Credit Score: Minimum 620 for conventional loans

- Debt-to-Income Ratio: Typically under 43%

- Employment Verification: Stable income for past two years

- Down Payment: Ranging from 3.5% to 20% depending on loan type

- Asset Documentation: Proof of savings and financial reserves

Preparing for the pre-approval process requires careful financial planning and documentation. Buyers should gather recent pay stubs, tax returns, bank statements, and employment verification letters. Learn more about mortgage qualification strategies in our comprehensive guide, which provides detailed insights into navigating this complex financial journey.

Essential Steps In The Homebuying Journey

The homebuying journey is a complex process that demands strategic planning and careful navigation. BC Television emphasizes the critical importance of understanding each stage of the home purchasing process to make informed decisions and avoid potential pitfalls that can derail first-time buyers.

The journey typically unfolds through several key sequential stages. Initially, buyers must assess their financial readiness, which involves examining credit scores, establishing a realistic budget, and determining affordable price ranges. This preliminary phase includes obtaining mortgage pre-approval, a crucial step that provides a clear understanding of borrowing capacity and signals serious intent to sellers. Following pre-approval, buyers begin the property search, working closely with real estate professionals to identify homes that match their financial parameters and lifestyle requirements.

Critical steps in the homebuying journey include:

- Financial Assessment: Review credit, establish budget

- Mortgage Pre-Approval: Determine borrowing capacity

- Property Search: Identify suitable homes

- Home Inspection: Evaluate property condition

- Negotiation: Make competitive offer

- Closing: Complete legal and financial transactions

Successful home purchasing requires patience, research, and professional guidance.

Explore our first-time homebuyer strategies to understand how to navigate this complex journey with confidence and minimize potential challenges along the way.

Financial Responsibilities And Hidden Costs

Buying a home involves far more financial planning than simply saving for a down payment. Brookfield Residential emphasizes that first-time buyers must understand the comprehensive financial landscape beyond the initial property purchase, including numerous unexpected expenses that can significantly impact long-term affordability.

The true cost of homeownership extends well beyond the mortgage payment, encompassing a range of recurring and potential expenses that first-time buyers must carefully budget for. Ongoing financial responsibilities include property taxes, homeowners insurance, private mortgage insurance, utilities, regular maintenance, and potential renovation costs. These expenses can add thousands of dollars annually to a homeowner’s financial obligations, making it crucial to develop a comprehensive financial strategy that accounts for more than just the monthly mortgage payment.

Key financial responsibilities and hidden costs include:

- Property Taxes: Annual assessments varying by location

- Homeowners Insurance: Mandatory protection for property

- Maintenance Costs: Regular upkeep and unexpected repairs

- Utility Expenses: Electricity, water, gas, internet

- Private Mortgage Insurance: Required for low down payment loans

- Homeowners Association Fees: Applicable in certain communities

- Closing Costs: Initial one-time expenses during purchase

Successful homeownership requires careful financial planning and a realistic understanding of total ownership costs. Learn more about mortgage qualification strategies to help you navigate the complex financial landscape of first-time home buying with confidence and preparedness.

Avoiding Common First-Time Buyer Mistakes

Navigating the homebuying journey requires strategic awareness and proactive planning. Richmond American highlights that first-time buyers frequently underestimate the complexities of property acquisition, often falling into predictable financial traps that can derail their homeownership dreams.

BC Television emphasizes that many first-time buyers make critical strategic missteps during their purchasing process. These mistakes frequently involve skipping crucial steps like comprehensive home inspections, failing to secure mortgage pre-approval, and neglecting to thoroughly explore diverse mortgage options that could potentially offer more favorable financial terms. Understanding and anticipating these potential pitfalls can significantly improve a buyer’s chances of a successful and financially sound home purchase.

Common first-time buyer mistakes to avoid include:

- Skipping Home Inspections: Overlooking potential property issues

- Maxing Out Mortgage Qualification: Borrowing beyond comfortable limits

- Neglecting Credit Preparation: Failing to optimize credit score before application

- Insufficient Emergency Savings: Not maintaining financial buffer

- Ignoring Additional Ownership Costs: Underestimating maintenance expenses

- Rushing the Purchase: Making emotional instead of strategic decisions

- Avoiding Professional Guidance: Attempting to navigate process independently

Explore strategies to prevent the biggest homebuying mistakes and ensure a smoother, more confident path to homeownership.

Empower Your First-Time Homebuying Journey with Expert Mortgage Solutions

The Complete Guide to Guidelines for First-Time Buyers highlights the challenges of navigating mortgage eligibility, hidden costs, and common pitfalls. Many first-time buyers struggle with understanding credit requirements, choosing the right loan type, and preparing for the pre-approval process. These concerns can make homeownership feel overwhelming and stressful. You deserve a clear path and personalized guidance to transform your homebuying experience into a confident and rewarding milestone.

Discover how Craigburn Capital can help you overcome these obstacles with tailored mortgage solutions designed specifically for first-time buyers. Whether you need assistance with credit preparation, selecting competitive mortgage options, or managing unexpected expenses, our experts provide exclusive rates and support every step of the way. Do not wait until confusion or hidden costs hold you back. Take action today by exploring our first-time homebuyer assistance and detailed mortgage qualification strategies. Make your dream of owning a home a reality now with trusted advice and personalized service from Craigburn Capital.

Frequently Asked Questions

What is considered a first-time buyer?

A first-time buyer is typically someone purchasing a home for the first time, characterized by limited real estate investment experience and a higher need for mortgage guidance.

What types of mortgages are available for first-time buyers?

First-time buyers have access to several mortgage types, including conventional loans, FHA loans, VA loans, USDA loans, and special first-time homebuyer programs, each with unique benefits tailored to different financial situations.

What are the eligibility criteria for mortgage pre-approval?

Eligibility for mortgage pre-approval usually includes a credit score of at least 620, a debt-to-income ratio under 43%, stable employment history, and sufficient savings for a down payment and closing costs.

What common mistakes should first-time buyers avoid?

First-time buyers should avoid skipping home inspections, maxing out their mortgage qualification limits, neglecting credit preparation, underestimating additional ownership costs, and rushing their purchasing decisions.