How to Structure Commercial Mortgage for Success

Most American business owners discover that nearly 80 percent of commercial loan applications are delayed or denied due to incomplete paperwork or unclear financial goals. Securing the right mortgage involves much more than finding a willing lender. If you want your American business to move forward with confidence, understanding every step of the process is crucial. This guide walks you through clear strategies to prepare, evaluate, and negotiate your commercial mortgage so you can secure funding efficiently.

Table of Contents

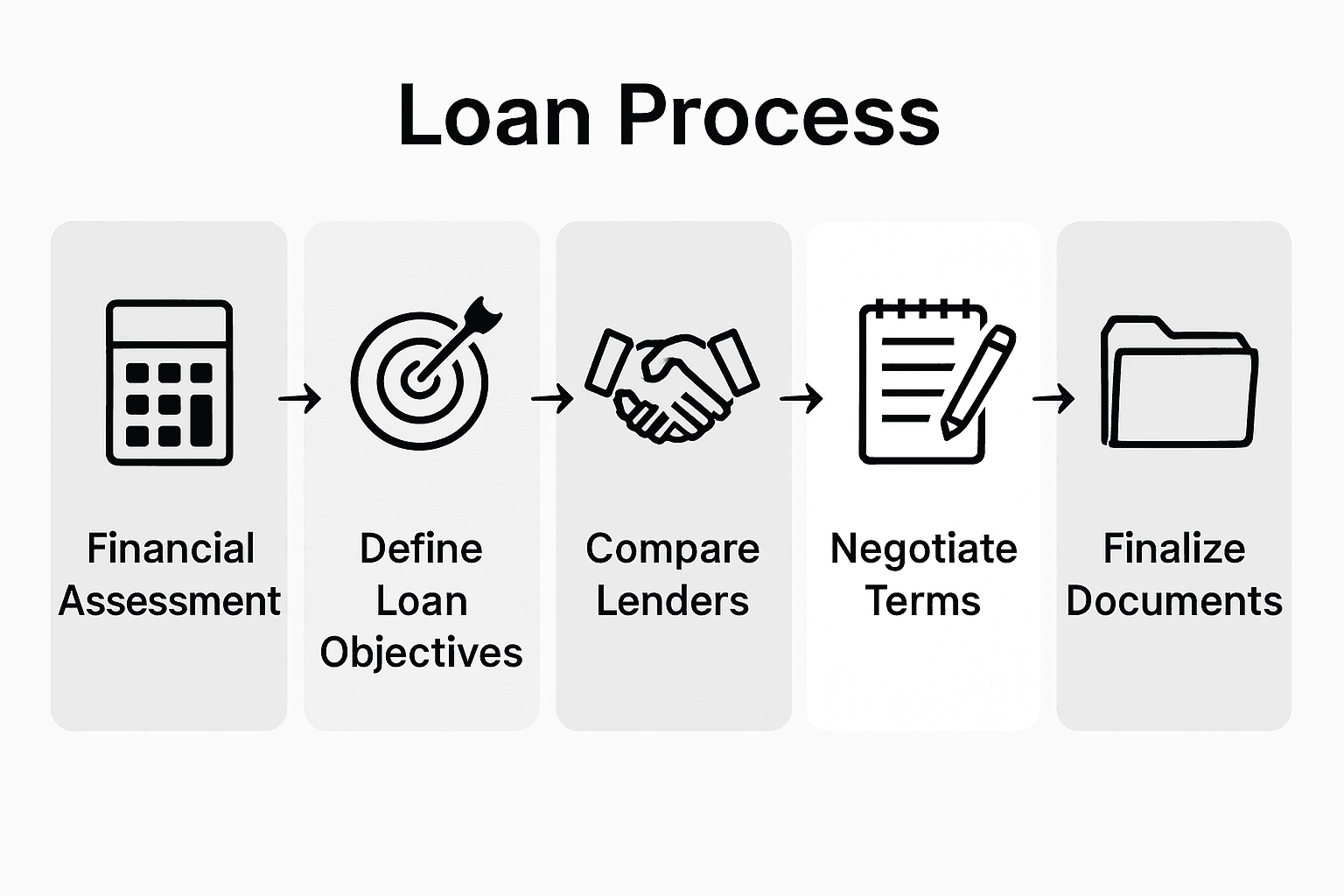

- Step 1: Assess Financial Position And Property Value

- Step 2: Define Loan Objectives And Requirements

- Step 3: Evaluate Lending Options And Terms

- Step 4: Negotiate Rates And Key Conditions

- Step 5: Complete Documentation And Finalize Funding

Quick Summary

| Key Point | Explanation |

|---|---|

| 1. Gather Comprehensive Financial Documentation | Assemble tax returns, balance sheets, and cash flow analyses to demonstrate your business’s fiscal health and stability for lenders. |

| 2. Define Clear Loan Objectives | Outline your specific financing needs including amount, terms, and intended use to align with lenders’ expectations. |

| 3. Compare Various Lending Options | Evaluate different loan structures based on interest rates, terms, and fees to identify the best fit for your business. |

| 4. Negotiate Terms Effectively | Prepare to discuss interest rates and terms with lenders, leveraging your financial strengths and market understanding. |

| 5. Prepare Accurate Final Documentation | Organize essential documents like appraisals and financial statements to streamline the submission process and ensure lender confidence. |

Step 1: Assess financial position and property value

Before securing a commercial mortgage, you need to conduct a comprehensive financial assessment that lenders will scrutinize carefully. This step involves gathering detailed financial documentation and understanding how your business’s financial health and property value impact your loan potential.

Start by compiling a robust financial package that demonstrates your business’s fiscal strength and stability. This means collecting several years of tax returns, profit and loss statements, balance sheets, and comprehensive cash flow analyses. Lenders want to see consistent revenue streams and your ability to manage debt effectively. You’ll also want to prepare detailed financial statements that showcase your business’s earning potential and existing assets. Pro tip: Create a clean, organized financial portfolio that tells a clear story of your business’s financial trajectory and demonstrates your preparedness for significant lending consideration.

Step 2: Define loan objectives and requirements

Defining clear loan objectives is a critical step in securing a successful commercial mortgage. This process involves carefully outlining your financial needs, understanding potential lending parameters, and aligning your business goals with appropriate financing strategies.

Start by developing a comprehensive loan proposal that articulates your specific financial requirements. Your objectives should encompass more than just the loan amount. Consider factors like desired repayment terms, interest rate expectations, and how the funding will specifically support your business expansion or property acquisition. You will want to demonstrate precise financial planning that shows lenders you have a strategic approach to utilizing borrowed capital. This means providing detailed documentation about how the loan funds will be deployed, potential revenue generation, and your business’s capacity to manage the additional financial obligation.

Pro tip: Anticipate potential lender questions by preparing a robust narrative that connects your loan request directly to tangible business growth opportunities and demonstrates a clear path to loan repayment.

Step 3: Evaluate lending options and terms

Navigating the complex landscape of commercial mortgage lending requires a strategic approach to understanding and comparing different financing options. Your goal is to find a lending solution that aligns perfectly with your business financial objectives and property investment strategy.

Commercial real estate loans offer diverse structures and terms that cater to varying business needs. You will want to carefully examine multiple aspects including interest rates, loan duration, repayment schedules, and qualifying criteria. Some key considerations include fixed versus variable rate options, balloon payment structures, and potential prepayment penalties. Pay close attention to how each lending option impacts your cash flow, considering not just the immediate financing terms but the long term financial implications for your business.

Commercial loan structures can significantly impact your financial planning, so take time to compare offerings from multiple lenders. Request detailed quotes, understand the total cost of borrowing, and evaluate how each option supports your specific business growth objectives. Look beyond just the interest rate and examine origination fees, closing costs, and potential future refinancing opportunities.

Here’s a summary comparing key types of commercial mortgage loan structures:

| Loan Structure | Typical Term Length | Common Interest Rate Type | Unique Consideration |

|---|---|---|---|

| Fixed-Rate Mortgage | 5-25 years | Fixed | Predictable payments over time |

| Variable-Rate Mortgage | 3-10 years | Variable | Payments may increase with rates |

| Balloon Payment Loan | 3-7 years | Fixed or Variable | Large final payment required |

| Bridge Loan | 6-36 months | Usually Variable | Short-term, quick funding option |

Pro tip: Create a comprehensive spreadsheet comparing loan terms from at least three different lenders, allowing you to objectively analyze and compare the financial implications of each offering.

Step 4: Negotiate rates and key conditions

Negotiating commercial mortgage rates and conditions represents a critical opportunity to optimize your financial arrangement and protect your business interests. This phase requires strategic preparation, clear communication, and a thorough understanding of your financial position and leverage points.

Commercial loan agreements demand careful negotiation of terms that align with your business objectives. Focus on key negotiable elements including interest rates, loan duration, prepayment penalties, and flexibility in repayment structures. Understand that lenders expect well prepared borrowers who can articulate their financial strengths and demonstrate a comprehensive understanding of the lending landscape.

Effective negotiation strategies involve comprehensive documentation and clear financial representations that highlight your business’s creditworthiness. Prepare detailed financial statements, cash flow projections, and a compelling narrative about your business growth potential. Be prepared to discuss alternative terms, such as adjustable rate options or shorter loan periods that might provide more favorable conditions. Remember that negotiation is a collaborative process where both parties seek a mutually beneficial arrangement.

Pro tip: Practice your negotiation script with a trusted financial advisor before meeting with lenders, anticipating potential questions and rehearsing confident responses that showcase your financial acumen.

Step 5: Complete documentation and finalize funding

The final stage of securing a commercial mortgage involves meticulously preparing and submitting comprehensive documentation that demonstrates your financial readiness and meets all lender requirements. This critical phase transforms your mortgage strategy from theoretical planning to actual funding.

Loan agreements require precise documentation that validates your financial capability. You will need to compile an extensive package including personal and business tax returns, financial statements, property appraisals, business plans, and detailed cash flow projections. Ensure every document is current, accurate, and professionally formatted. Lenders will scrutinize these materials to assess your creditworthiness and the potential risk associated with your loan.

The table below outlines essential documents often required in the final stage of securing a commercial mortgage:

| Document Type | Purpose | Preparation Tip |

|---|---|---|

| Tax Returns | Verify personal and business income levels | Use most recent, complete filings |

| Property Appraisal | Assess collateral property value | Hire a licensed, local appraiser |

| Financial Statements | Demonstrate business financial health | Ensure clarity and professional format |

| Business Plan | Show use of proceeds and growth strategy | Highlight revenue projections |

Finalizing commercial loan documentation involves understanding complex legal requirements and compliance standards. Carefully review all loan agreement terms, paying special attention to clauses related to prepayment penalties, interest rate adjustments, and potential default conditions. Consider consulting a legal professional who specializes in commercial real estate transactions to help you navigate these complex agreements and protect your business interests.

Pro tip: Create a dedicated digital folder with clearly labeled, high resolution scans of all required documents to streamline the submission process and demonstrate your organizational professionalism to potential lenders.

Secure Success With Expert Commercial Mortgage Guidance

Structuring a commercial mortgage can be a complex challenge that demands attention to financial details like loan objectives, interest rates, and negotiation terms. If you feel overwhelmed by comparing loan structures or finalizing documentation to ensure the best outcome for your business, you are not alone. The article “How to Structure Commercial Mortgage for Success” highlights critical steps such as assessing your financial position, evaluating lending options, and negotiating key conditions to protect your investment and growth potential.

At Craigburn Capital, we understand these specific pain points and offer tailored solutions designed to simplify this process. Whether you are navigating fixed or variable rate mortgages, seeking competitive interest rates, or crafting a strategic loan proposal, our experienced mortgage brokers will guide you every step of the way. Benefit from our exclusive access to unadvertised rates and personal financial strategies that align perfectly with your goals.

Take control of your commercial financing journey today. Visit Craigburn Capital to explore our services, download free resources, and connect with mortgage experts ready to help you turn complex loan structures into clear business opportunities.

Ready to shape a successful commercial mortgage? Contact us now to get personalized advice and start building your financial future with confidence.

Frequently Asked Questions

How can I assess my financial position before applying for a commercial mortgage?

To assess your financial position, compile key financial documents such as tax returns, profit and loss statements, and balance sheets. Organize these materials to clearly demonstrate your business’s financial health and prepare for lender scrutiny.

What should I include in my loan objectives for a commercial mortgage?

Your loan objectives should detail not only the amount you are seeking but also repayment terms, interest rate expectations, and how the loan will support your business goals. Clearly outline the anticipated use of funds and expected revenue generation to strengthen your proposal.

What factors should I consider when evaluating lending options for a commercial mortgage?

When evaluating lending options, consider interest rates, loan duration, repayment schedules, and any potential fees. Create a comparison chart to analyze the total cost of borrowing and identify which option aligns best with your business’s financial needs.

How can I effectively negotiate rates and terms for a commercial mortgage?

Effective negotiation involves being prepared with comprehensive documentation that showcases your business’s creditworthiness. Articulate your financial strengths and be open to discussing alternative terms that might provide more favorable conditions for your loan.

What documents do I need to compile for finalizing a commercial mortgage?

You need to compile documents such as personal and business tax returns, financial statements, property appraisals, and your business plan. Ensure that all documents are current and professionally formatted to facilitate lender review.

What should I do after submitting my commercial mortgage application?

After submitting your application, follow up with the lender to ensure they have received all required documents. Maintain open communication for any questions they may have, and be prepared to provide additional information if necessary.

Recommended

- 7 Essential Commercial Mortgage Tips 2025 for Success – Craigburn Capital

- Commercial Mortgage Explained: Complete Guide for 2025 – Craigburn Capital

- Why Choose Commercial Mortgages for Business Growth – Craigburn Capital

- Master the Commercial Financing Workflow for Success – Craigburn Capital

- Commercial Gutter Cleaning – Why Property Health Depends On It