Mortgage Terms Explained: Keys to Smarter Home Buying

Most American homebuyers enter the mortgage process with misconceptions that make it harder to find the right loan. Nearly one in three Americans believe only perfect credit can secure a mortgage, yet government-backed options offer flexibility for many first-time buyers. With terminology ranging from principal to adjustable-rate confusion, understanding the basics is critical for making confident decisions. This guide clears up common myths and explains essential mortgage terms to help American buyers avoid costly missteps.

Table of Contents

- Defining Mortgage Terms And Common Misconceptions

- Types Of Mortgage Loans And Rates Explained

- Key Features: Terms, Amortization, And Payments

- Legal Obligations And Borrower Responsibilities

- Financial Implications And Common Pitfalls

Key Takeaways

| Point | Details |

|---|---|

| Understanding Mortgage Terms | Familiarize yourself with key terms like interest rates, principal, down payment, and loan term to navigate the mortgage process successfully. |

| Be Aware of Misconceptions | Many believe perfect credit is necessary for a mortgage; however, various programs cater to diverse financial backgrounds. |

| Evaluate Mortgage Types | Choose from fixed-rate, adjustable-rate, and government-backed loans based on your financial situation and long-term goals. |

| Consider Financial Implications | Recognize hidden costs and prepare a comprehensive budget to manage ongoing expenses beyond the mortgage payment. |

Defining Mortgage Terms and Common Misconceptions

Navigating the mortgage landscape requires understanding key terminology and dispelling prevalent myths. Consumer mortgage terms can vary significantly across different lending environments, making financial literacy crucial for potential homebuyers.

Mortgage terminology encompasses several critical concepts that often confuse first-time borrowers. Interest rates, principal, down payment, and loan term represent foundational elements every homebuyer must comprehend. An interest rate represents the percentage charged by lenders for borrowing money, while the principal reflects the actual amount borrowed. Down payments signify the initial upfront percentage paid toward home purchase, typically ranging between 3% to 20% of total home value. Loan terms specify the duration over which mortgage repayment occurs, commonly structured as 15 or 30-year agreements.

Common misconceptions frequently derail potential homebuyers’ financial planning. Many individuals mistakenly believe they require perfect credit or massive savings to qualify for a mortgage. Government home loan programs offer diverse options that accommodate various financial backgrounds. Another prevalent myth suggests that adjustable-rate mortgages are always riskier than fixed-rate alternatives. While adjustable-rate mortgages can introduce financial variability, they might provide lower initial rates beneficial for specific buyer circumstances.

Understanding these nuanced mortgage terms empowers buyers to make informed decisions. By demystifying complex financial language and challenging widespread misconceptions, potential homeowners can approach mortgage acquisition with confidence and strategic insight.

Types of Mortgage Loans and Rates Explained

Mortgage loan types represent diverse financial pathways for homebuyers seeking tailored borrowing solutions. Understanding these variations enables potential homeowners to select financing strategies aligned with their unique financial circumstances and long-term goals.

The mortgage landscape encompasses several primary loan categories. Fixed-rate mortgages provide consistent interest rates throughout the loan duration, offering predictable monthly payments that simplify financial planning. Adjustable-rate mortgages feature interest rates that fluctuate based on market conditions, potentially starting with lower initial rates but introducing long-term payment uncertainty. Government-backed options like FHA and VA loans provide alternative financing routes for borrowers who might not qualify for conventional mortgage products, often featuring more flexible credit requirements and lower down payment thresholds.

Interest rates play a critical role in determining mortgage affordability and overall borrowing costs. Rates fluctuate based on multiple factors, including credit score, loan term, down payment size, and broader economic conditions. Borrowers with stronger credit profiles typically secure more favorable interest rates, potentially saving thousands of dollars over the loan’s lifetime. Mortgage rate structures vary significantly, making comprehensive research and professional guidance essential for making informed financing decisions.

Selecting the appropriate mortgage type requires careful evaluation of personal financial health, future income projections, and long-term housing objectives. Potential homebuyers should consider factors like job stability, anticipated income growth, and personal risk tolerance when comparing different loan options. Consulting with experienced mortgage professionals can provide personalized insights tailored to individual financial scenarios, helping borrowers navigate the complex landscape of home financing with confidence.

Key Features: Terms, Amortization, and Payments

Mortgage payment structures involve complex financial mechanisms that directly impact long-term financial planning and homeownership sustainability. Understanding these intricate details helps borrowers make informed decisions about their home financing strategies.

Amortization represents a critical concept in mortgage financing, describing how loan payments are structured to progressively reduce principal while covering interest charges. Typically, early mortgage payments allocate a larger percentage toward interest, with subsequent payments gradually shifting to principal reduction. Standard mortgage terms include 15-year and 30-year options, each presenting unique advantages. Shorter-term loans often feature lower interest rates but require higher monthly payments, while longer-term mortgages provide more manageable monthly expenses at the cost of increased total interest paid over the loan’s lifetime.

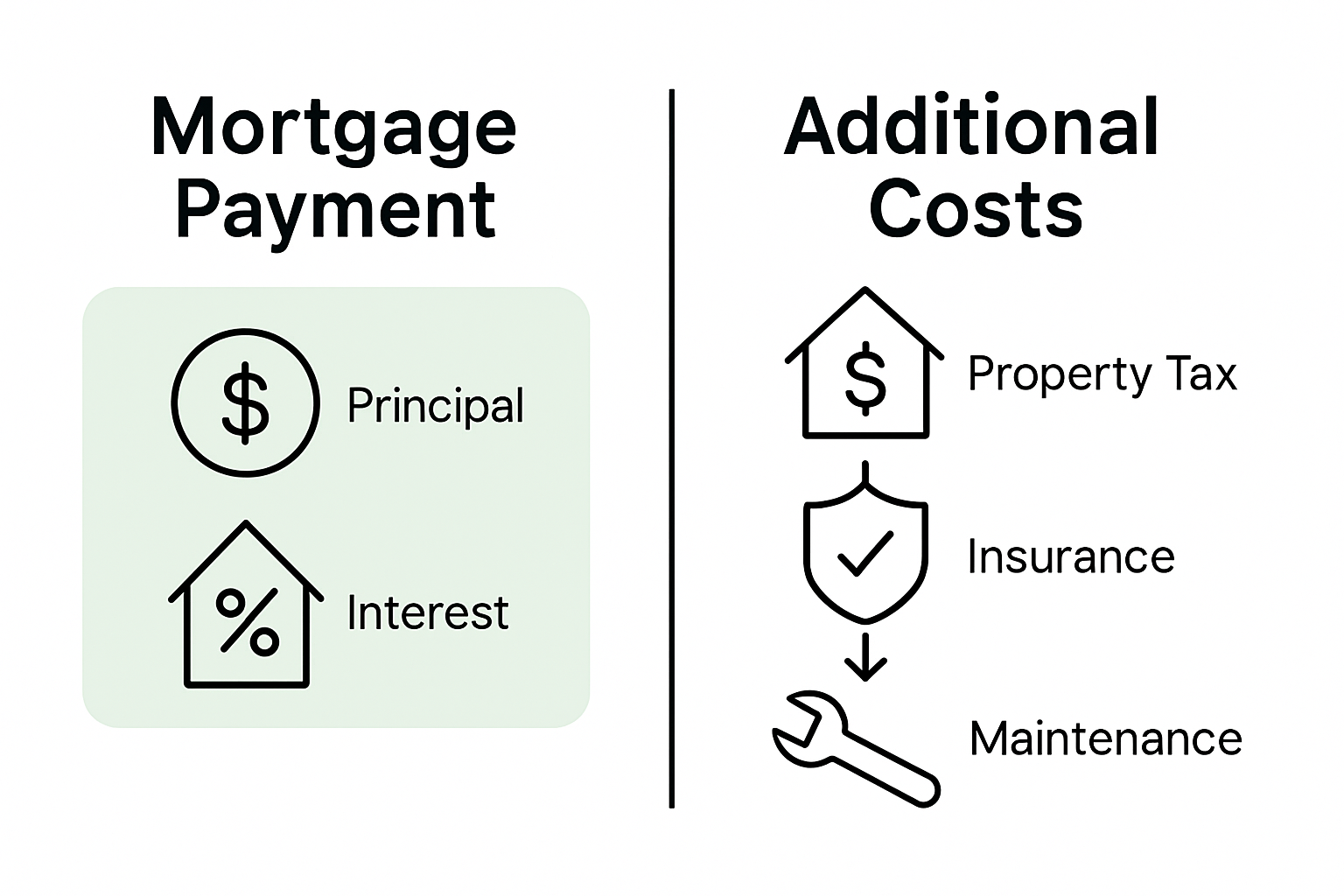

Mortgage payments comprise multiple components beyond simple principal and interest calculations. Property taxes, homeowners insurance, and private mortgage insurance frequently factor into monthly payment structures. These additional expenses can significantly impact overall affordability, with some lenders requiring escrow accounts to manage these supplemental costs. Credit scores play a pivotal role in determining interest rates, with higher credit ratings typically qualifying for more favorable lending terms and potentially reducing long-term borrowing expenses.

Navigating mortgage terms requires careful financial assessment and strategic planning. Borrowers should evaluate their current financial stability, projected income growth, and long-term housing objectives when selecting mortgage structures. Consulting with financial professionals can provide personalized insights, helping individuals identify mortgage solutions that align with their unique financial circumstances and future goals. The right mortgage strategy balances immediate affordability with long-term financial health, transforming homeownership from a complex financial challenge into an achievable personal milestone.

Legal Obligations and Borrower Responsibilities

Mortgage borrowers assume complex legal responsibilities that extend far beyond simple monthly payments. Understanding these obligations protects both lenders and borrowers, ensuring a transparent and legally compliant lending relationship.

Legal documentation forms the cornerstone of mortgage agreements, outlining precise expectations and potential consequences for non-compliance. Borrowers must meticulously review and comprehend loan contracts, which typically include clauses detailing payment schedules, default provisions, and potential foreclosure scenarios. Critical legal responsibilities include maintaining timely monthly payments, preserving property condition, maintaining appropriate insurance coverage, and promptly communicating any financial challenges that might impact repayment capacity. Failure to meet these obligations can result in significant financial penalties, credit score damage, and potential legal action.

Mortgage contracts typically include several key legal protections and requirements for borrowers. Property taxes, homeowners insurance, and mortgage insurance represent mandatory components that borrowers must consistently manage. Credit reporting mechanisms track borrower performance, with late payments potentially triggering negative consequences that extend beyond immediate financial penalties. Borrowers must understand their comprehensive legal responsibilities to maintain good standing and protect their financial future.

Navigating legal obligations requires proactive financial management and consistent communication with lenders. Borrowers should develop comprehensive strategies for meeting all contractual requirements, including establishing emergency funds, maintaining accurate financial records, and seeking professional guidance when facing potential challenges. Understanding the full scope of legal responsibilities transforms mortgage management from a potential source of stress into a structured pathway toward successful homeownership and long-term financial stability.

Financial Implications and Common Pitfalls

Mortgage financial landscapes involve intricate challenges that can dramatically impact long-term financial health. Understanding these complexities helps borrowers navigate potential risks and make more informed financing decisions.

Hidden costs represent a significant pitfall for many homebuyers, extending far beyond simple monthly mortgage payments. Borrowers frequently underestimate expenses like property maintenance, unexpected repairs, homeowners association fees, and annual tax assessments. These supplemental costs can quickly escalate, transforming what appeared to be an affordable mortgage into a financial strain. Smart buyers develop comprehensive budget projections that account for these additional expenses, creating financial buffers to manage potential economic fluctuations.

Interest rate structures pose another critical financial consideration for potential homeowners. Adjustable-rate mortgages can initially appear attractive with lower introductory rates, but long-term financial implications demand careful evaluation. Borrowers must carefully analyze potential rate increases, understanding how future market changes might impact monthly payments. Credit scores significantly influence interest rate offerings, with higher credit ratings typically qualifying for more favorable lending terms. Preparing comprehensive financial documentation, maintaining strong credit profiles, and developing realistic income projections can help mitigate potential lending risks.

Effective mortgage management requires proactive financial strategies and continuous education. Borrowers should establish emergency savings funds, maintain flexible financial approaches, and remain prepared to adjust strategies as economic conditions evolve. Professional financial counseling can provide valuable insights, helping individuals develop personalized approaches that align mortgage commitments with broader financial goals. By understanding potential pitfalls and maintaining strategic financial perspectives, homebuyers can transform mortgage acquisition from a potential source of stress into a structured pathway toward long-term wealth building.

Unlock Smarter Home Buying with Expert Mortgage Solutions

Understanding complex mortgage terms like interest rates, amortization, and legal obligations is the first step toward confident homeownership. If you feel overwhelmed by financial jargon or worried about finding the right mortgage fit—especially if you face challenges like imperfect credit or uncertain income—Craigburn Capital is here to help. We specialize in tailoring mortgage solutions that turn confusing terms into clear, manageable plans designed around your goals.

Take control of your home financing journey today by visiting Craigburn Capital. Access competitive and exclusive mortgage rates, explore options for first-time homebuyers, self-employed individuals, and those needing flexible lending. Don’t let myths or hidden costs hold you back. Connect now for personalized guidance that empowers you to make smarter home buying decisions with confidence.

Frequently Asked Questions

What is a mortgage and what key terms should I know?

A mortgage is a loan specifically used to purchase real estate, and important terms include interest rate, principal, down payment, and loan term. Understanding these terms is crucial for navigating the mortgage process effectively.

What are fixed-rate and adjustable-rate mortgages?

Fixed-rate mortgages maintain a consistent interest rate throughout the loan term, resulting in predictable payments. Conversely, adjustable-rate mortgages have varying interest rates that may change based on market conditions, offering lower initial rates but potential long-term uncertainty.

What are common misconceptions about qualifying for a mortgage?

Many believe they need perfect credit or a large down payment to qualify. However, there are government home loan programs available that cater to diverse financial situations, often requiring less stringent credit and down payment criteria.

What additional costs should I consider when budgeting for a mortgage?

Homebuyers should account for hidden costs like property taxes, homeowners insurance, maintenance, and any homeowner association fees. These expenses can significantly affect overall affordability beyond the monthly mortgage payments.

Recommended

- Complete Guide to Guidelines for First-Time Buyers – Craigburn Capital

- 7 Essential First-Time Homebuyer Tips for Smart Financing – Craigburn Capital

- 7 Essential Steps in a First-Time Homebuyer Checklist – Craigburn Capital

- 7 Essential Questions to Ask Mortgage Brokers Before You Apply – Craigburn Capital

- Lack of liquidity hits Danish mortgage bonds – Future Family Office