Mortgage Insurance in Canada – How It Impacts Homebuyers

Many Canadian homebuyers are surprised to discover that mortgage insurance rules differ sharply from American practices, with nearly 35 percent needing insurance simply due to low down payments. This key difference can shape how quickly families enter the housing market. Understanding Canada’s unique mortgage insurance requirements helps you avoid costly mistakes and gives you the clarity needed to plan smarter for your future home.

Table of Contents

- Mortgage Insurance In Canada Explained

- Types: CMHC, Private, And Lender Solutions

- Eligibility, Application Process, And Coverage Triggers

- Costs, Premiums, And Financial Impact On Borrowers

- Legal Protections, Exclusions, And Obligations

- Common Missteps And Alternatives For Buyers

Key Takeaways

| Point | Details |

|---|---|

| Mortgage Default Insurance is Mandatory | Canadian homebuyers with down payments less than 20% must obtain mortgage default insurance to secure financing. |

| Primary Providers | The Canada Mortgage and Housing Corporation (CMHC) is the main provider, alongside private insurers Sagen and Canada Guaranty, offering varying premium structures. |

| Eligibility Criteria | Insurance eligibility primarily hinges on down payment size and factors like credit score and income stability, impacting approval and premiums. |

| Financial Impact | Mortgage insurance premiums increase overall borrowing costs, necessitating careful financial planning for homebuyers to assess affordability. |

Mortgage Insurance in Canada Explained

Mortgage insurance in Canada plays a crucial role in helping homebuyers secure financing when they cannot provide a substantial down payment. Mortgage default insurance is a specialized protection mechanism that enables lenders to approve mortgages for buyers with down payments less than 20% of a property’s value.

Unlike optional life or disability insurance products, mortgage default insurance is mandatory for homebuyers with smaller down payments. This insurance protects the lender, not the borrower, by guaranteeing that the mortgage will be repaid even if the homeowner defaults. Optional mortgage insurance products remain separate and can be purchased to cover additional risks like job loss or critical illness.

The primary provider of mortgage default insurance in Canada is the Canada Mortgage and Housing Corporation (CMHC). When you make a down payment between 5% and 19.99%, you are required to purchase this insurance, which is typically rolled into your mortgage payments. The insurance premium varies based on the size of your down payment, with smaller down payments resulting in higher insurance costs. Homebuyers should budget for these additional expenses when planning their mortgage strategy.

For many first-time homebuyers, mortgage insurance represents a critical pathway to homeownership. By allowing individuals to purchase homes with lower initial capital, this insurance model helps Canadians enter the real estate market more quickly and with greater financial flexibility. Understanding how mortgage insurance works can help you make more informed decisions about your home purchasing journey.

Types: CMHC, Private, and Lender Solutions

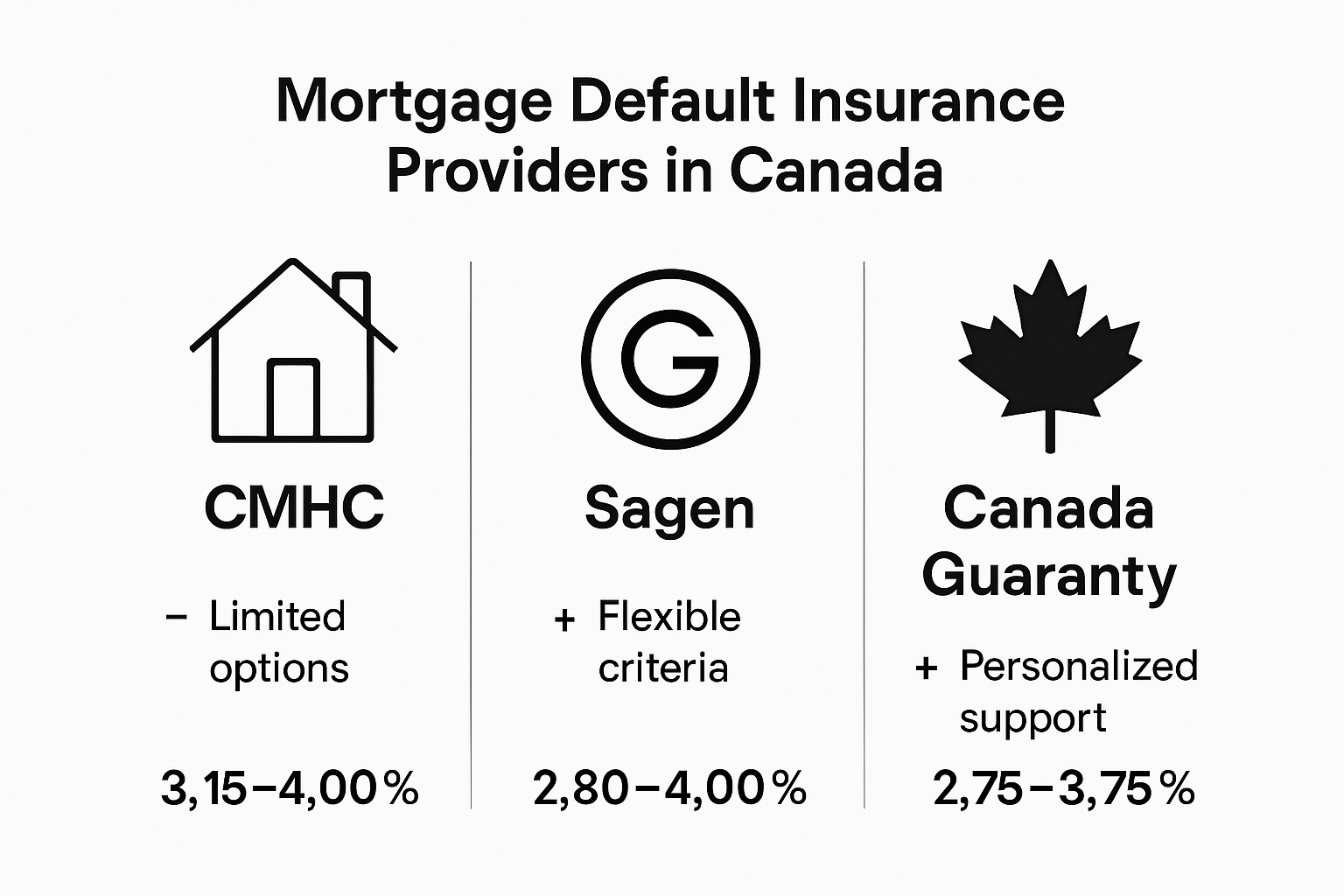

Mortgage insurance in Canada encompasses three primary providers, each offering unique approaches to protecting lenders and enabling homebuyers to secure financing. Mortgage default insurance is strategically offered by the Canada Mortgage and Housing Corporation (CMHC), a government-backed Crown corporation, and two private insurers: Sagen and Canada Guaranty.

The CMHC stands as the most prominent mortgage default insurance provider, functioning as the national housing agency. As a government entity, CMHC offers the most comprehensive and widely recognized insurance product. Private insurers Sagen (formerly Genworth Canada) and Canada Guaranty provide alternative options, creating a competitive landscape that benefits homebuyers by offering multiple insurance pathways. These providers enable lenders to extend mortgages to borrowers with down payments lower than the traditional 20% threshold.

Each mortgage insurance provider has distinct characteristics and pricing structures. CMHC typically offers the most standardized rates, while private insurers might provide more flexible terms for unique borrower situations. Homebuyers should carefully compare insurance premiums, which vary based on factors like down payment size, credit history, and property type. Private lending options can also intersect with mortgage insurance strategies, providing additional flexibility for borrowers who might not qualify through traditional channels.

Understanding the nuanced differences between CMHC, Sagen, and Canada Guaranty is crucial for making informed mortgage decisions. While all three providers essentially offer the same core product—protection for lenders against potential mortgage defaults—their specific terms, premium calculations, and approval processes can vary significantly. Homebuyers are encouraged to work closely with mortgage professionals who can help navigate these complex insurance landscape and identify the most suitable option for their unique financial circumstances.

Eligibility, Application Process, and Coverage Triggers

Mortgage insurance eligibility in Canada primarily depends on several critical factors, with the most significant being the size of a homebuyer’s down payment. Optional mortgage insurance products provide additional protection that borrowers can voluntarily select during mortgage application or renewal processes.

To qualify for mandatory mortgage default insurance, homebuyers must meet specific criteria. Down payment is the primary determinant, with insurance required for purchases where the down payment is less than 20% of the property’s value. Lenders will typically assess additional factors including credit score, income stability, and debt-to-income ratio. Borrowers with credit scores below 600 might face more stringent requirements or potentially higher insurance premiums, making it crucial to maintain a strong credit profile.

The application process involves several key steps. First, potential homebuyers must provide comprehensive financial documentation, including proof of income, employment verification, and detailed credit history. Mortgage default insurers like CMHC, Sagen, and Canada Guaranty will evaluate these documents to assess risk. Private lending options can offer alternative paths for those who might not meet traditional insurance qualification standards, providing additional flexibility in the mortgage acquisition process.

Coverage triggers for mortgage insurance vary depending on the specific type of protection selected. Mandatory default insurance protects lenders in case of borrower default, while optional insurance products can cover scenarios such as job loss, critical illness, or death. Homebuyers should carefully review the specific terms of each insurance product, understanding exactly what circumstances would activate the coverage and what financial protections are included. The goal is to create a comprehensive safety net that provides financial security during unexpected life challenges.

Costs, Premiums, and Financial Impact on Borrowers

Mortgage insurance premiums represent a significant financial consideration for Canadian homebuyers, directly impacting the overall cost of homeownership. Optional mortgage insurance products can add substantial expenses to a borrower’s monthly budget, necessitating careful financial planning and assessment of individual risk tolerance.

The premium structure for mortgage default insurance is typically calculated as a percentage of the total mortgage amount, with rates varying based on down payment size. Homebuyers with down payments between 5% and 19.99% will face higher premiums, often ranging from 2.4% to 4% of the total mortgage value. These costs can be substantial – for a $400,000 mortgage, insurance premiums could translate to $9,600 to $16,000, which can be either paid upfront or rolled into the mortgage payments, increasing the overall borrowing expenses.

Factors influencing mortgage insurance premiums extend beyond down payment size. Credit score, property type, loan purpose, and borrower occupancy status all play critical roles in determining final costs. 7 Essential questions to ask mortgage brokers can help borrowers understand the nuanced pricing mechanisms and potential ways to minimize insurance expenses. Self-employed individuals or those with non-traditional income streams might encounter more complex premium calculations.

While mortgage insurance adds a financial layer to home purchasing, it simultaneously enables many Canadians to enter the housing market who would otherwise be unable to secure financing. The trade-off between higher upfront or ongoing costs versus the opportunity to own a home creates a complex financial calculus that requires strategic thinking. Borrowers should carefully model these additional expenses, understanding how insurance premiums impact their long-term financial planning and monthly budget allocations.

Legal Protections, Exclusions, and Obligations

Mortgage insurance in Canada operates under a complex legal framework designed to protect both lenders and borrowers. Optional mortgage insurance products come with specific regulatory guidelines that ensure consumers have clear rights and cannot be unduly pressured by financial institutions.

The legal landscape for mortgage default insurance includes critical restrictions and requirements. Mortgage default insurance regulations specify that insurance is mandatory for home purchases with down payments less than 20%, but unavailable for properties valued over C$1.5 million. Borrowers must meet stringent credit and debt service requirements, with lenders prohibited from arbitrarily denying coverage. These regulations create a structured approach that balances risk management with consumer protection.

Important exclusions and obligations define the scope of mortgage insurance coverage. Key legal protections include restrictions preventing lenders from compelling borrowers to purchase optional insurance products as a condition of mortgage approval. This means consumers must provide explicit consent for additional insurance, protecting them from potential predatory lending practices. Self-employed individuals, investors, and borrowers with non-traditional income streams may face more complex qualification processes, requiring careful documentation and financial transparency.

Navigating the legal intricacies of mortgage insurance demands careful attention to detail. Borrowers should understand that while mandatory default insurance protects lenders, it does not provide direct financial protection for the homeowner. The insurance ensures mortgage availability for those with smaller down payments but does not cover personal financial risks. Consulting with mortgage professionals who can interpret these nuanced legal requirements becomes crucial in making informed decisions about home financing and insurance obligations.

Common Missteps and Alternatives for Buyers

Homebuyers often encounter complex challenges when navigating mortgage insurance options, with several common missteps potentially compromising their financial strategy. Optional mortgage insurance products require careful assessment to ensure they truly align with individual financial circumstances and risk management needs.

One significant misstep involves blindly accepting default insurance without exploring alternative protection strategies. Mortgage protection can take multiple forms, including personal life insurance, disability coverage, and specialized financial instruments that might offer more comprehensive or cost-effective protection. Guidelines for first-time buyers emphasize the importance of comparing multiple insurance products and understanding their specific terms, rather than accepting the first option presented by a lender.

Self-employed individuals and those with non-traditional income streams face unique challenges in mortgage insurance selection. These borrowers must be particularly vigilant about understanding exclusions, coverage limitations, and potential gaps in protection. Alternative strategies might include building larger down payments, maintaining robust emergency funds, or exploring private mortgage insurance options that offer more flexible underwriting standards. Sophisticated buyers often combine multiple risk management tools to create a comprehensive financial safety net.

Ultimately, successful mortgage insurance navigation requires a proactive approach. Buyers should conduct thorough research, consult multiple financial professionals, and develop a holistic strategy that addresses both mandatory default insurance requirements and personal risk management needs. The goal is not just securing a mortgage, but creating a sustainable long-term financial framework that provides security and flexibility.

Take Control of Your Mortgage Insurance Journey Today

Understanding mortgage insurance in Canada is essential for overcoming the challenges of securing financing with a smaller down payment. If the cost of mortgage default insurance premiums or the complexity of comparing providers like CMHC, Sagen, and Canada Guaranty feels overwhelming mortgage solutions tailored to your specific situation can make all the difference. Whether you are a first-time homebuyer navigating mandatory insurance or a self-employed individual seeking flexible options there are smarter ways to manage these costs and protect your investment.

Discover personalized lending strategies and expert guidance at Craigburn Capital where competitive rates and exclusive programs are designed to empower you through every step of your homebuying journey. Don’t let mortgage insurance premiums hold you back. Get clear answers and customized mortgage options now by exploring private lending solutions or reviewing our essential questions to ask mortgage brokers. Take action today to turn the mortgage insurance challenge into your pathway to homeownership.

Frequently Asked Questions

What is mortgage insurance and why is it mandatory for some homebuyers?

Mortgage insurance is a type of protection required for homebuyers who make a down payment of less than 20% of the property’s value. It protects the lender by guaranteeing that the mortgage will be repaid even if the borrower defaults.

How do mortgage insurance premiums vary based on down payment size?

Mortgage insurance premiums are calculated as a percentage of the total mortgage amount. Borrowers with down payments between 5% and 19.99% face higher premiums, which typically range from 2.4% to 4% of the mortgage value.

What are the different types of mortgage insurance available in Canada?

The main types of mortgage insurance in Canada include mandatory mortgage default insurance provided by the Canada Mortgage and Housing Corporation (CMHC) and two private insurers: Sagen and Canada Guaranty. Each provider has unique terms and pricing structures.

What factors affect eligibility for mortgage default insurance?

Eligibility for mortgage default insurance primarily depends on the size of the down payment. Homebuyers need a down payment of less than 20%, and lenders also consider credit score, income stability, and debt-to-income ratio when assessing risk.