First-Time Homebuyer Programs: Unlocking Homeownership Opportunities

Most American first-time buyers face a daunting obstacle when it comes to securing a home, with over 60 percent citing the down payment as the biggest barrier. Navigating the maze of assistance programs can feel confusing, but understanding your options opens new possibilities for affordable homeownership. This guide breaks down the essential facts, reveals surprising eligibility details, and shows how American families are leveraging special programs to turn their dreams into reality.

Table of Contents

- Defining First-Time Homebuyer Programs

- Major Program Types And Key Differences

- Eligibility Criteria And Required Documentation

- Financial Benefits And Potential Savings

- Common Mistakes And How To Avoid Them

Key Takeaways

| Point | Details |

|---|---|

| First-Time Homebuyer Programs | These programs provide financial support through down payment assistance, favorable mortgage terms, and educational resources to facilitate homeownership for inexperienced buyers. |

| Types of Assistance | Various options include government-backed loans, state and local grants, and private sector initiatives, each with unique eligibility requirements and financial benefits. |

| Eligibility Requirements | Buyers usually must meet specific income limits and documentation criteria, including proof of income and credit history, to qualify for assistance programs. |

| Common Pitfalls | Many first-time buyers make the mistake of underestimating total homeownership costs; thus, thorough financial planning and research are crucial to avoid common errors. |

Defining First-Time Homebuyer Programs

First-time homebuyer programs represent strategic financial initiatives designed to help individuals transition from renting to homeownership by reducing barriers to entry. These specialized programs provide targeted support through multiple mechanisms, including favorable mortgage terms, down payment assistance, and educational resources tailored to inexperienced buyers. When exploring first-time homebuyer assistance, potential homeowners discover multiple pathways to make their property ownership dreams more accessible.

The core components of first-time homebuyer programs typically include several key financial supports. Down payment assistance remains a critical feature, with many programs offering grants or low-interest loans that help buyers overcome the significant upfront costs associated with purchasing a home. Credit score flexibility represents another crucial element, with some programs accommodating buyers who might not qualify for traditional mortgage products. These initiatives recognize that potential homeowners might have limited credit history or modest financial resources.

Unique program structures vary widely, but most share common objectives of expanding homeownership opportunities. Some programs target specific demographics like young professionals, veterans, or individuals in particular income brackets. Others focus on geographic regions or provide incentives for purchasing homes in developing neighborhoods. Guidelines for first-time buyers can help potential homeowners understand the nuanced requirements and benefits associated with these specialized financing options. By creating more inclusive pathways to property ownership, these programs play a vital role in supporting economic mobility and community development.

Successful navigation of first-time homebuyer programs requires thorough research and strategic planning. Prospective buyers should carefully assess their personal financial situation, understand program-specific requirements, and explore multiple assistance options. Consulting with mortgage professionals who specialize in first-time buyer support can provide personalized guidance through this complex landscape. The right program can transform homeownership from an intimidating challenge into an achievable milestone.

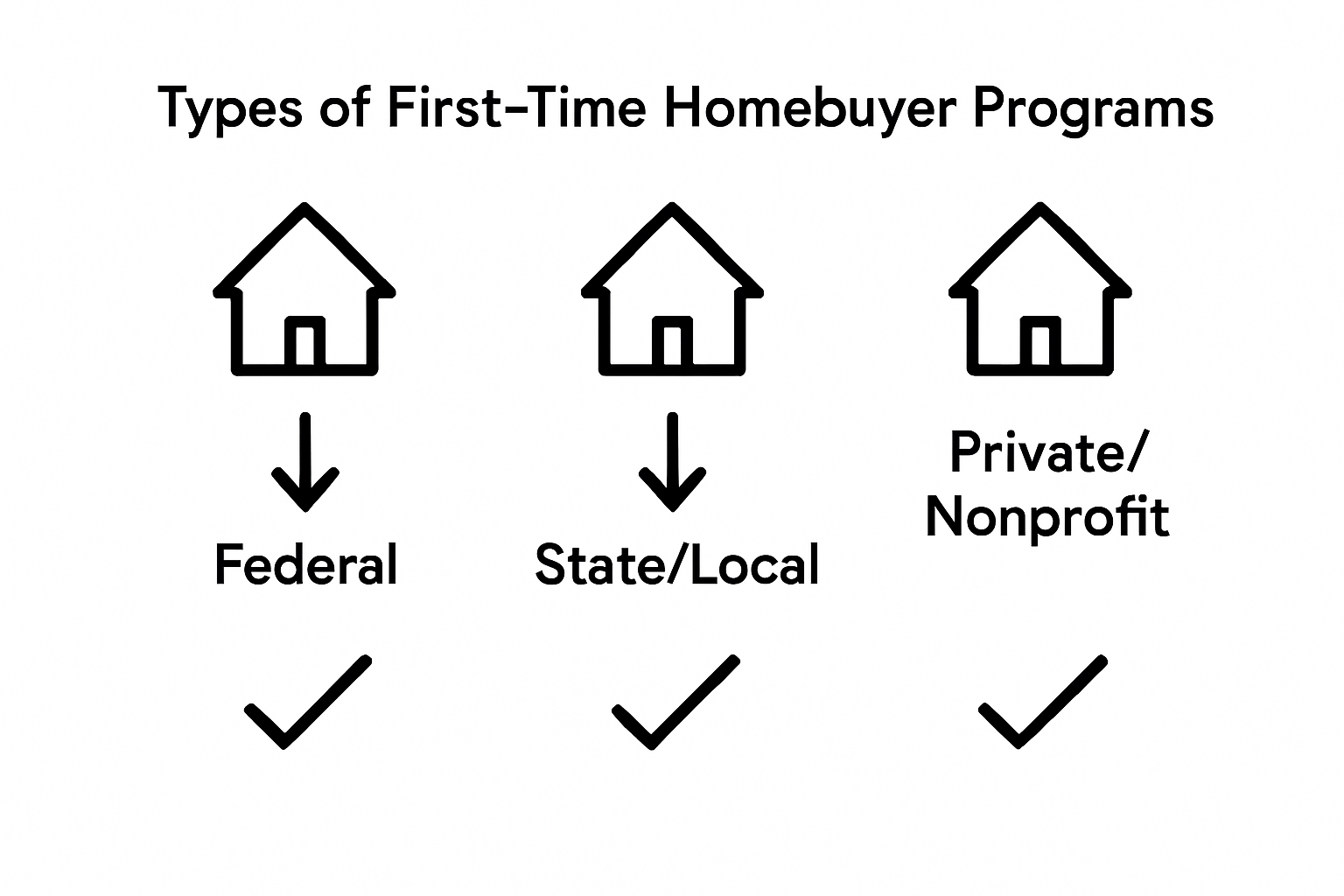

Major Program Types and Key Differences

First-time homebuyer programs encompass a diverse range of financial assistance strategies designed to support individuals entering the housing market. Government-backed loans represent a primary category of support, with Federal Housing Administration (FHA) loans standing out as a particularly accessible option. These specialized loans offer more lenient credit requirements and lower down payment thresholds, making homeownership achievable for buyers who might struggle with traditional mortgage standards.

The landscape of first-time homebuyer programs includes multiple distinct types of financial support. Federal programs like FHA and VA loans provide structured pathways for specific demographics, including veterans and first-time buyers with limited financial resources. State-level initiatives often complement these federal options, offering targeted grants and low-interest loan programs. First-time homebuyer grants emerge as another critical support mechanism, providing direct financial assistance that does not require repayment and helping buyers overcome significant upfront purchasing barriers.

Private sector and nonprofit programs add additional layers of support to the homebuyer assistance ecosystem. Fannie Mae and Freddie Mac offer specialized low down payment programs, while local community organizations frequently develop hyper-targeted assistance models. These programs might focus on specific professions, such as teachers or healthcare workers, or provide incentives for purchasing homes in developing neighborhoods. Some innovative initiatives even combine down payment assistance with financial education, ensuring buyers not only receive monetary support but also develop the knowledge necessary for sustainable homeownership.

Understanding the nuanced differences between program types is crucial for prospective homebuyers. Each assistance model carries unique eligibility requirements, financial terms, and potential long-term implications. Buyers should carefully evaluate their personal financial situation, credit profile, and homeownership goals when exploring these diverse support options. Consulting with mortgage professionals who specialize in first-time buyer programs can provide personalized guidance through this complex landscape of financial opportunities.

Eligibility Criteria and Required Documentation

Qualifying for first-time homebuyer programs involves navigating a complex set of eligibility requirements that vary across different assistance models. First-time homebuyer assistance typically establishes specific parameters to determine program participation, with most initiatives defining a first-time buyer as an individual who has not owned a primary residence in the past three years. Income limitations represent another critical factor, with most programs establishing maximum household earnings to ensure support targets those who genuinely need financial assistance.

Documentation requirements for first-time homebuyer programs are comprehensive and demand meticulous preparation. Prospective buyers must typically compile an extensive portfolio of financial records, including but not limited to:

- Proof of income (recent pay stubs, W-2 forms, tax returns)

- Credit history reports

- Bank statements demonstrating financial stability

- Employment verification

- Identification documents

- Detailed information about current assets and debts

Beyond financial documentation, many programs impose additional eligibility criteria that extend beyond traditional lending standards. Some initiatives require participants to complete homebuyer education courses, which provide crucial insights into responsible homeownership, financial management, and the intricate process of property acquisition. Guidelines for first-time buyers often emphasize the importance of these educational components as a means of ensuring long-term housing stability and financial success.

The complexity of eligibility requirements underscores the importance of thorough research and professional guidance. Potential buyers should anticipate variations across different program types, recognizing that federal, state, and local assistance models may have distinct qualification parameters. Consulting with mortgage professionals who specialize in first-time homebuyer programs can provide personalized insights, helping individuals navigate the nuanced landscape of documentation and eligibility. Patience, meticulous preparation, and a proactive approach to understanding program specifics can transform the seemingly overwhelming process of qualifying for homeownership assistance into an achievable milestone.

Financial Benefits and Potential Savings

First-time homebuyer programs offer substantial financial advantages that can significantly reduce the economic barriers to homeownership. Upfront cost reduction emerges as a primary benefit, with many programs providing strategic mechanisms to minimize the initial financial investment required to purchase a home. These initiatives typically address the most challenging aspects of home buying, including down payment requirements, closing costs, and interest rate structures that can save buyers thousands of dollars during the purchasing process.

The financial benefits of first-time homebuyer programs extend across multiple dimensions of property acquisition. Key savings opportunities include:

- Reduced down payment requirements (sometimes as low as 3-5%)

- Lower interest rates compared to traditional mortgage products

- Potential grants that do not require repayment

- Assistance with closing cost coverage

- Tax credits for first-time homebuyers

- Reduced private mortgage insurance (PMI) rates

First-time homebuyer grants represent a particularly attractive financial support mechanism, providing direct monetary assistance that can dramatically lower the overall cost of home acquisition. These grants offer potential buyers a unique opportunity to receive financial support without the burden of repayment, effectively bridging the gap between savings and homeownership. Some programs provide grants ranging from $5,000 to $25,000, which can be applied directly to down payments, closing costs, or other home-purchasing expenses.

Beyond immediate financial relief, these programs create long-term economic advantages for participants. By reducing initial barriers to entry, first-time homebuyer programs enable individuals to build equity earlier, potentially accelerating personal wealth accumulation. Prospective buyers should approach these opportunities strategically, carefully evaluating program-specific benefits and understanding how each financial advantage aligns with their individual homeownership goals. Consulting with mortgage professionals can help buyers maximize these financial benefits and develop a comprehensive strategy for sustainable homeownership.

Common Mistakes and How to Avoid Them

First-time homebuyer programs can be challenging to navigate, and potential buyers often encounter significant pitfalls that can derail their homeownership journey. Financial miscalculation stands as the most prevalent error, with many buyers underestimating the comprehensive costs associated with purchasing and maintaining a home. Beyond the initial purchase price, prospective homeowners must account for property taxes, insurance, maintenance expenses, potential renovation costs, and unexpected repairs that can quickly erode financial stability.

Common mistakes in the first-time homebuyer process include:

- Failing to get pre-approved for a mortgage before house hunting

- Overlooking additional homeownership expenses beyond mortgage payments

- Neglecting to thoroughly review credit reports and improve credit scores

- Skipping home inspection processes

- Making large financial purchases or changing jobs during mortgage approval

- Emptying entire savings accounts for down payment and closing costs

First-time homebuyer grants can provide critical financial support, but buyers must carefully understand their specific eligibility and program requirements. Many individuals mistakenly assume these grants are universally available or apply broad assumptions about qualification criteria. Successful navigation requires meticulous research, understanding program-specific nuances, and maintaining realistic expectations about the level of financial assistance available.

Mitigating risks in the homebuying process demands a proactive and strategic approach. Prospective buyers should prioritize financial education, seek guidance from experienced mortgage professionals, and develop a comprehensive understanding of their personal financial landscape. Creating a robust financial buffer, maintaining stable employment, and avoiding significant financial disruptions during the mortgage approval process can significantly improve the likelihood of successful homeownership. Patience, thorough preparation, and a willingness to learn can transform potential pitfalls into opportunities for informed decision-making.

Empower Your Journey with Expert First-Time Homebuyer Support

Navigating the complexities of first-time homebuyer programs can feel overwhelming when facing the challenges of down payment assistance, credit flexibility, and eligibility requirements. You want to make informed decisions, avoid costly mistakes, and unlock the financial benefits designed to make homeownership achievable. At Craigburn Capital, we understand these hurdles and specialize in turning these barriers into stepping stones toward your new home.

Take control of your homebuying experience today by partnering with mortgage professionals dedicated to your success. Visit Craigburn Capital to explore tailored solutions including first-time homebuyer assistance and practical guidelines for first-time buyers. Act now to access competitive rates, exclusive programs, and expert guidance designed to maximize your savings and secure your future. Your pathway to homeownership starts here.

Frequently Asked Questions

What are first-time homebuyer programs?

First-time homebuyer programs are financial initiatives designed to assist individuals transitioning from renting to owning a home by reducing barriers such as high down payments and strict credit requirements.

What types of financial assistance do first-time homebuyer programs typically provide?

These programs often offer down payment assistance, favorable mortgage terms, and educational resources tailored to inexperienced buyers, helping make homeownership more accessible.

How can I qualify for a first-time homebuyer program?

To qualify, you typically need to meet specific eligibility criteria, which often include being a first-time buyer (not having owned a home in the past three years), adhering to income limits, and providing comprehensive financial documentation.

What are common mistakes to avoid when applying for first-time homebuyer programs?

Common mistakes include failing to get pre-approved for a mortgage, underestimating homeownership costs, neglecting credit checks, and making major financial changes during the mortgage approval process.

Recommended

- First-Time Homebuyer Assistance: Unlocking Homeownership – Craigburn Capital

- 7 Essential Steps in a First-Time Homebuyer Checklist – Craigburn Capital

- Complete Guide to Guidelines for First-Time Buyers – Craigburn Capital

- 7 Essential First-Time Homebuyer Tips for Smart Financing – Craigburn Capital

- Top Homebuyer Incentives for Toronto and Durham Region 2025 – Fanis Makrigiannis

Realtor®