Why Choose Commercial Mortgages for Business Growth

Over half of American businesses rely on commercial mortgages to secure and grow valuable real estate assets, fueling both expansion and stability. Yet many decision-makers misunderstand how these complex loans differ from residential financing, leading to costly missteps. Gaining clarity on commercial mortgages empowers American entrepreneurs and investors to make smarter choices, avoid common pitfalls, and unlock advantages that build long-term financial strength.

Table of Contents

- Commercial Mortgages Defined And Debunked

- Types Of Commercial Mortgages Explained

- Key Features And Qualification Criteria

- Benefits For Business Owners And Investors

- Risks, Costs, And How To Avoid Pitfalls

- Comparing Commercial Vs. Alternative Financing

Key Takeaways

| Point | Details |

|---|---|

| Commercial Mortgages vs. Residential Mortgages | Commercial mortgages are designed for business purposes, focusing on property revenue potential rather than personal credit scores. |

| Types of Commercial Mortgages | Options include conventional loans, CMHC-insured mortgages, and conduit loans, each with unique advantages suited to different business needs. |

| Qualification Criteria | Lenders assess financial health using metrics like Debt Service Coverage Ratio (DSCR) and Loan-to-Value (LTV) ratios, necessitating extensive documentation. |

| Benefits and Risks | While commercial mortgages offer property control and potential tax benefits, they also come with risks such as market volatility and hidden costs that require careful management. |

Commercial Mortgages Defined and Debunked

A commercial mortgage represents a specialized financing tool designed to help businesses acquire, develop, or refinance properties used for commercial purposes. Unlike residential mortgages, these financial instruments are structured with unique parameters that cater specifically to business investment strategies. Commercial mortgages enable entrepreneurs and companies to secure real estate assets that can drive significant growth and generate long-term financial returns.

Commercial mortgages differ substantially from traditional home loans in several key aspects. While residential mortgages typically focus on individual housing needs, commercial mortgages are tailored to support business objectives. These loans can be used to purchase office buildings, warehouses, retail spaces, apartment complexes, and other income-generating properties. The lending criteria are more complex, often evaluating the potential revenue generation of the property and the financial health of the business, rather than solely examining personal credit scores.

The structure of commercial mortgages involves several critical components that distinguish them from standard lending products. Loan terms are generally shorter, ranging from 5 to 20 years, with interest rates that reflect the perceived risk of the commercial venture. Lenders typically require more substantial down payments, often between 25% to 35% of the property’s total value, compared to residential mortgage requirements. This higher upfront investment ensures that businesses have a significant financial stake in the property and demonstrates their commitment to the investment.

Understanding the nuanced landscape of commercial mortgage applications can significantly improve a business’s chances of securing favorable financing. Potential borrowers should prepare comprehensive documentation including detailed business plans, financial statements, property appraisals, and projected income statements. By presenting a clear, strategic vision and demonstrating robust financial management, businesses can position themselves as attractive candidates for commercial mortgage lending.

Types of Commercial Mortgages Explained

Commercial mortgages encompass a diverse range of financing options designed to meet the unique needs of businesses across different industries and investment strategies. Mortgage types vary significantly based on factors like property type, risk profile, and borrower financial characteristics. Understanding these variations can help businesses select the most appropriate financing solution for their specific commercial real estate objectives.

The primary categories of commercial mortgages include conventional loans, CMHC-insured mortgages, and conduit loans. Conventional loans represent the most traditional financing option, typically requiring substantial down payments and offering competitive interest rates for businesses with strong credit profiles. CMHC-insured mortgages provide additional security for lenders, often enabling borrowers to access more favorable terms by reducing the perceived risk. Conduit loans offer a more flexible approach, characterized by faster processing times and broader loan program selections, making them attractive for businesses seeking rapid financing.

Each commercial mortgage type carries distinct advantages and potential drawbacks. Conventional loans often provide the most straightforward terms but demand rigorous financial documentation and higher credit standards. CMHC-insured mortgages can offer lower interest rates and longer amortization periods, particularly beneficial for stable, income-generating properties. Conduit loans excel in scenarios requiring quick funding and accommodate more diverse property types, though they might include more complex structuring and potentially higher transaction costs.

Businesses considering commercial mortgages should conduct comprehensive financial analysis to determine the most suitable option. Factors like property type, intended use, projected revenue, current market conditions, and the company’s financial health all play crucial roles in selecting the right mortgage product. Consulting with experienced mortgage professionals can help navigate these complex decisions, ensuring businesses secure financing that aligns perfectly with their strategic growth objectives.

Key Features and Qualification Criteria

Commercial mortgages involve a complex evaluation process that goes far beyond traditional lending standards. Key features of commercial mortgage underwriting include comprehensive financial assessments that examine multiple dimensions of both the borrower’s financial health and the property’s potential income generation. Lenders meticulously analyze factors such as business cash flow, credit history, property appraisal, and projected revenue to determine loan eligibility and terms.

The qualification criteria for commercial mortgages typically revolve around several critical financial metrics. Debt service coverage ratio (DSCR) emerges as a fundamental benchmark, measuring a business’s ability to cover mortgage payments through its operational income. Most lenders require a DSCR of 1.25 or higher, indicating the borrower can comfortably manage debt obligations. Loan-to-value ratios represent another crucial element, with most commercial mortgage providers expecting down payments between 25% to 35% of the total property value, demonstrating the borrower’s financial commitment and reducing the lender’s potential risk.

Beyond financial metrics, lenders conduct extensive due diligence that includes reviewing detailed business plans, analyzing market conditions, and assessing the specific property’s potential for generating sustainable income. They examine factors like location, property condition, potential for appreciation, and the borrower’s industry track record. Businesses with established credit histories, consistent revenue streams, and clear growth strategies typically present the most attractive profiles for commercial mortgage approval.

Successful commercial mortgage applications require meticulous preparation and a comprehensive understanding of lender expectations. Borrowers should compile thorough documentation including three years of tax returns, detailed financial statements, business projections, and comprehensive property appraisals. By presenting a robust financial narrative that demonstrates stability, potential for growth, and a strategic approach to property investment, businesses can significantly enhance their chances of securing favorable commercial mortgage terms.

Benefits for Business Owners and Investors

Commercial mortgages represent a powerful financial strategy for businesses seeking to leverage real estate as a strategic asset. Potential investment benefits extend far beyond simple property ownership, offering sophisticated entrepreneurs multiple avenues for financial growth and long-term wealth accumulation. By transforming real estate from a cost center into a potential revenue generator, businesses can unlock significant economic opportunities.

The primary advantages of commercial mortgages include direct property control, equity building, and potential tax benefits. Business owners gain substantial advantages by owning their commercial premises, including the ability to customize spaces, eliminate unpredictable rental increases, and build substantial equity over time. Unlike traditional leasing arrangements, commercial mortgages allow businesses to transform monthly expenses into long-term asset appreciation, creating a powerful wealth-building mechanism that simultaneously serves operational needs.

Investors find commercial mortgages particularly attractive due to their potential for generating stable, predictable income streams. Commercial properties often feature long-term lease agreements that provide consistent revenue, making them an appealing option for risk-conscious investors seeking diversification beyond traditional investment vehicles. The ability to leverage commercial real estate allows investors to spread risk across multiple property types, industries, and geographic locations, creating a robust and resilient investment portfolio.

Beyond financial returns, commercial mortgages offer strategic flexibility that can dramatically enhance business growth potential. Entrepreneurs can use property appreciation to secure additional financing, expand operations, or reinvest in core business activities. The combination of potential tax deductions, equity accumulation, and operational control makes commercial mortgages a sophisticated financial tool for businesses looking to transform real estate from a mere overhead expense into a dynamic strategic asset.

Risks, Costs, and How to Avoid Pitfalls

Commercial mortgages represent a sophisticated financial instrument with inherent complexities that demand careful strategic planning. Understanding potential risks is crucial for businesses seeking to navigate the intricate landscape of commercial real estate financing. Default risk emerges as a primary concern, influenced by broader economic conditions, property market dynamics, and the borrower’s financial stability.

The financial risks associated with commercial mortgages extend beyond simple default potential. Loan selection requires meticulous evaluation of interest rate volatility, underwriting standards, and long-term economic projections. Businesses must conduct comprehensive due diligence, analyzing factors such as potential market fluctuations, property valuation trends, and their own long-term financial projections. Hidden costs can include substantial origination fees, appraisal expenses, legal charges, and potential prepayment penalties that can significantly impact the overall financial burden.

To mitigate potential risks, businesses should implement a multi-layered risk management strategy. This approach includes maintaining robust financial reserves, conducting thorough property and market research, and developing flexible contingency plans. Entrepreneurs should carefully analyze their debt service coverage ratios, ensure consistent cash flow projections, and maintain a conservative approach to borrowing. Diversifying investment strategies, maintaining multiple revenue streams, and establishing strong relationships with experienced financial advisors can provide additional layers of financial protection.

Successful navigation of commercial mortgage risks requires a proactive and strategic approach. Businesses should prioritize transparency in financial reporting, maintain excellent credit histories, and develop comprehensive business plans that demonstrate long-term viability. By understanding potential pitfalls, conducting thorough due diligence, and maintaining financial flexibility, entrepreneurs can transform commercial mortgages from potential financial risks into powerful tools for strategic business growth and asset accumulation.

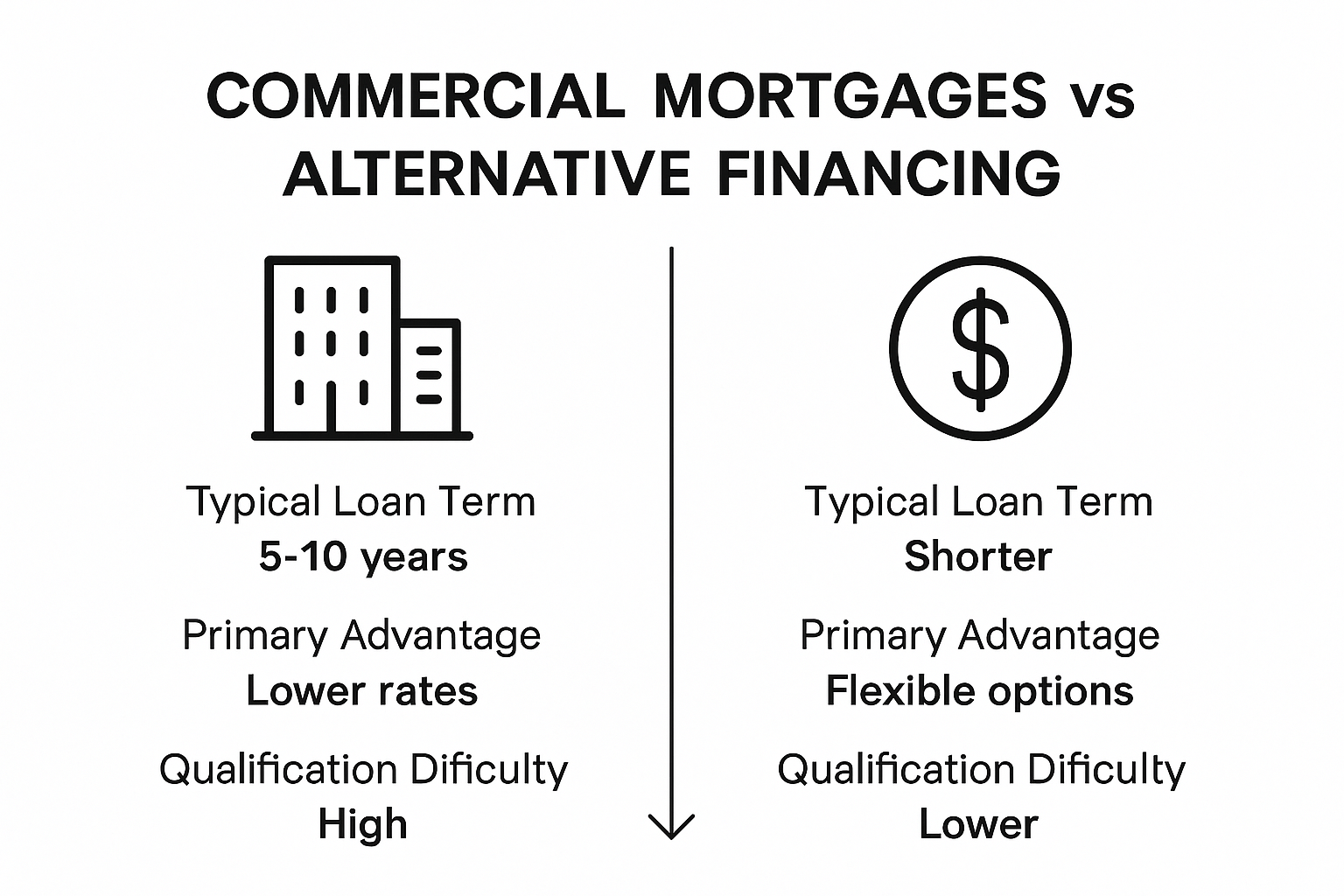

Comparing Commercial vs. Alternative Financing

Business financing represents a complex ecosystem with multiple funding approaches, each offering distinct advantages and challenges. Commercial mortgage markets encompass diverse lending technologies, ranging from traditional bank financing to more innovative non-bank lending solutions. Understanding the nuanced differences between commercial mortgages and alternative financing options can help businesses make strategic funding decisions aligned with their specific growth objectives.

The primary alternatives to commercial mortgages include asset-backed commercial paper programs, private lending, equipment financing, and line of credit options. Asset-backed commercial paper programs operate distinctly from traditional mortgage structures, offering short-term debt instruments that can provide more flexible funding mechanisms. These alternatives often feature different underwriting standards, interest rates, and repayment structures compared to conventional commercial mortgages, allowing businesses to select financing that most closely matches their unique financial requirements.

Commercial mortgages distinguish themselves through several key characteristics that set them apart from alternative financing methods. Unlike unsecured lending options, commercial mortgages are directly tied to real estate assets, providing lenders with stronger collateral protection. This asset-backed nature typically translates into lower interest rates, longer repayment terms, and more substantial borrowing limits. Alternative financing solutions might offer faster approval processes or more flexible qualification criteria, but they often come with higher costs, shorter repayment periods, and more restrictive usage conditions.

Choosing between commercial mortgages and alternative financing requires a comprehensive evaluation of business goals, financial health, and specific funding needs. Businesses should carefully analyze factors such as long-term growth strategies, cash flow projections, asset ownership objectives, and risk tolerance. While commercial mortgages offer stability and potential asset appreciation, alternative financing can provide more immediate liquidity and operational flexibility. The optimal financing strategy often involves a strategic combination of different funding sources, tailored to support the business’s unique financial landscape and growth trajectory.

Unlock Your Business Growth with Tailored Commercial Mortgage Solutions

Securing the right commercial mortgage can feel overwhelming with complex terms like debt service coverage ratio and loan-to-value expectations. You want a financing option that fits your unique business goals, offers competitive interest rates, and reduces risk while maximizing potential returns. At Craigburn Capital, we understand these challenges and specialize in crafting personalized commercial financing strategies that align with your vision and financial health. Whether you are purchasing income-generating properties or refinancing for expansion, we empower you with expert guidance and exclusive mortgage opportunities designed to help you build long-term equity.

Don’t let complicated lending criteria hold your business back. Discover how our specialized commercial mortgage services can simplify the process and put you on the fast track to growth. Visit Craigburn Capital now to explore our full range of lending solutions including private lending and tailored mortgage programs. Take the first step toward financial confidence and secure your commercial property with trusted expertise. Contact us today and transform your real estate goals into thriving assets.

Frequently Asked Questions

What are the benefits of choosing a commercial mortgage for business growth?

Commercial mortgages offer several advantages, including direct property control, equity building, and potential tax benefits. They allow businesses to transform real estate into an asset that appreciates over time and offers a stable income stream.

How do commercial mortgages differ from residential mortgages?

Commercial mortgages are specifically tailored for business purposes, featuring different lending criteria. They generally require larger down payments, shorter loan terms, and consideration of the property’s income-generating potential, rather than just the borrower’s personal credit profile.

What key factors should a business consider when applying for a commercial mortgage?

Businesses should evaluate their financial health, projected revenue, property type, and market conditions. It’s important to prepare comprehensive documentation, including financial statements and detailed business plans, to demonstrate a strategic vision and financial stability.

What risks are associated with commercial mortgages?

Risks include default potential, interest rate volatility, and hidden costs. Businesses should conduct thorough due diligence and maintain financial reserves to manage these risks effectively, ensuring a proactive approach to managing their mortgage agreements.

Recommended

- Commercial Mortgage Explained: Complete Guide for 2025 – Craigburn Capital

- Commercial Mortgage Application Guide: Secure Approval Fast – Craigburn Capital

- How to Qualify for a Mortgage: Step-by-Step Guide for Buyers – Craigburn Capital

- Private Lending Explained: Benefits, Types, and Risks – Craigburn Capital