Construction Financing Explained: Key Steps for Buyers

Over half of all American homebuyers say construction financing is more complicated than a standard mortgage. Building a new home or commercial property in the United States brings a maze of financial steps and requirements that can catch even experienced buyers off guard. Understanding the basics of American construction financing gives you a solid foundation to navigate costs, select the right lender, and avoid common pitfalls from the very first blueprint.

Table of Contents

- What Is Construction Financing and How It Works

- Types of Construction Loans Available

- Eligibility, Qualifications, and Required Documents

- Stages of the Construction Loan Process

- Costs, Risks, and Common Pitfalls

Key Takeaways

| Point | Details |

|---|---|

| Understanding Construction Financing | Construction financing is tailored for funding building projects, with funds released incrementally as milestones are met, ensuring oversight and financial accountability. |

| Types of Construction Loans | Different loan types cater to varied needs, including construction-to-permanent loans for seamless transitions to mortgages and stand-alone loans for separate financing phases. |

| Eligibility and Documentation | Higher credit scores and detailed project documentation are critical for loan approval; thorough organization of documents can streamline the application process. |

| Managing Risks | Construction projects face significant risks such as cost overruns and delays; maintaining contingency funds and choosing experienced contractors can mitigate these challenges. |

What Is Construction Financing and How It Works

Construction financing represents a specialized lending approach designed to help homebuyers and developers fund new building projects from groundbreaking to completion. Unlike traditional mortgages, these loans provide capital specifically tailored to cover the complex costs associated with constructing a new home or commercial property. Construction loans from financial institutions are typically secured by a first mortgage and disbursed in carefully controlled stages to ensure project progress and financial accountability.

The core mechanism of construction financing involves a unique draw schedule where funds are released incrementally as specific project milestones are achieved. Lenders conduct periodic inspections to verify work completion before authorizing subsequent payments, which protects both the borrower and the financial institution. This staged approach allows developers and homeowners to access necessary funds while providing the lender with ongoing oversight of the construction process. Typically, these loans have shorter terms compared to standard mortgages, often converting to traditional long-term financing once the construction is finalized.

Construction loans generally cover a wide range of expenses beyond just the basic building costs. These may include land purchase, architectural and engineering fees, building permits, construction materials, labor costs, and even a buffer for potential unexpected expenses. The loan amount is usually based on the projected completed value of the property, which requires detailed documentation including comprehensive building plans, budget estimates, and contractor credentials. Borrowers must demonstrate not just creditworthiness, but also the feasibility and potential success of their construction project.

Pro Tip – Builder Selection: Always choose a licensed, experienced contractor with a proven track record of completing similar projects on time and within budget, as this significantly improves your chances of securing construction financing and completing your project successfully.

Types of Construction Loans Available

Construction financing encompasses several specialized loan types designed to meet different project needs and borrower requirements. The Federal Deposit Insurance Corporation (FDIC) outlines multiple construction loan categories, each with unique characteristics and risk profiles. The primary types include construction-to-permanent loans, stand-alone construction loans, renovation construction loans, and owner-builder construction loans.

Construction-to-Permanent Loans represent a comprehensive financing option that seamlessly transitions from the construction phase to a traditional mortgage. These loans combine the initial construction financing with a permanent mortgage, reducing closing costs and simplifying the overall financing process. Borrowers appreciate this approach as it requires only a single loan application and provides a predetermined interest rate for the entire project duration. Typically, lenders disburse funds in stages as construction milestones are completed, with the loan automatically converting to a standard mortgage once the building is finished.

Alternative construction loan types cater to more specialized scenarios. Stand-Alone Construction Loans provide short-term financing specifically for the building phase, requiring borrowers to secure a separate mortgage after completion. Renovation Construction Loans are particularly useful for existing properties requiring significant upgrades or complete reconstruction, allowing homeowners to finance both the purchase and renovation costs within a single loan package. Owner-Builder Construction Loans offer a unique option for individuals who plan to act as their own general contractor, though these typically require extensive documentation and demonstrate higher risk for lenders.

Pro Tip – Loan Comparison: Carefully compare the terms, interest rates, and conversion options of different construction loan types, as the right choice can save thousands of dollars and significantly streamline your building project.

Here’s a quick comparison of major construction loan types and who they best serve:

| Loan Type | Key Benefits | Who It’s Best For |

|---|---|---|

| Construction-to-Permanent | Single closing, seamless to mortgage | Most homebuyers and developers |

| Stand-Alone Construction | Lower initial costs, flexible structure | Those seeking later refinancing |

| Renovation Construction | Funds for purchase plus improvements | Buyers remodeling existing homes |

| Owner-Builder Construction | Greater control, potential cost savings | Experienced builders managing project |

Eligibility, Qualifications, and Required Documents

Financial institutions carefully evaluate construction loan applicants using a comprehensive assessment of the borrower’s financial health, project viability, and risk profile. The eligibility criteria extend far beyond traditional mortgage requirements, focusing on three critical dimensions: borrower creditworthiness, project feasibility, and financial capacity. Lenders conduct an exhaustive review that examines credit scores, income stability, existing debt obligations, and the specific details of the proposed construction project.

Credit Requirements typically demand a higher credit score for construction loans compared to standard mortgages, with most lenders seeking scores of 680 or above. Borrowers must demonstrate a strong credit history, consistent income, and a debt-to-income ratio usually below 43%. Self-employed individuals face additional scrutiny, requiring multiple years of tax returns, profit and loss statements, and potentially more extensive documentation to verify income stability. Lenders also evaluate the borrower’s experience with similar construction projects, especially for owner-builder loans where the applicant acts as their own general contractor.

The documentation requirements for construction loans are significantly more comprehensive than traditional mortgage applications. Essential documents include detailed project plans, comprehensive budget estimates, contractor credentials, property appraisals, and thorough financial statements. Borrowers must typically provide proof of income (W-2 forms, tax returns, pay stubs), asset verification (bank statements, investment accounts), construction contracts, detailed project timelines, and comprehensive building plans. Professional contractors must submit additional documentation, including their license, insurance information, previous project portfolios, and references that demonstrate their capability to complete the proposed project.

Pro Tip – Documentation Preparation: Compile all financial and project documents well in advance of your loan application, organizing them systematically to streamline the review process and demonstrate your preparedness to potential lenders.

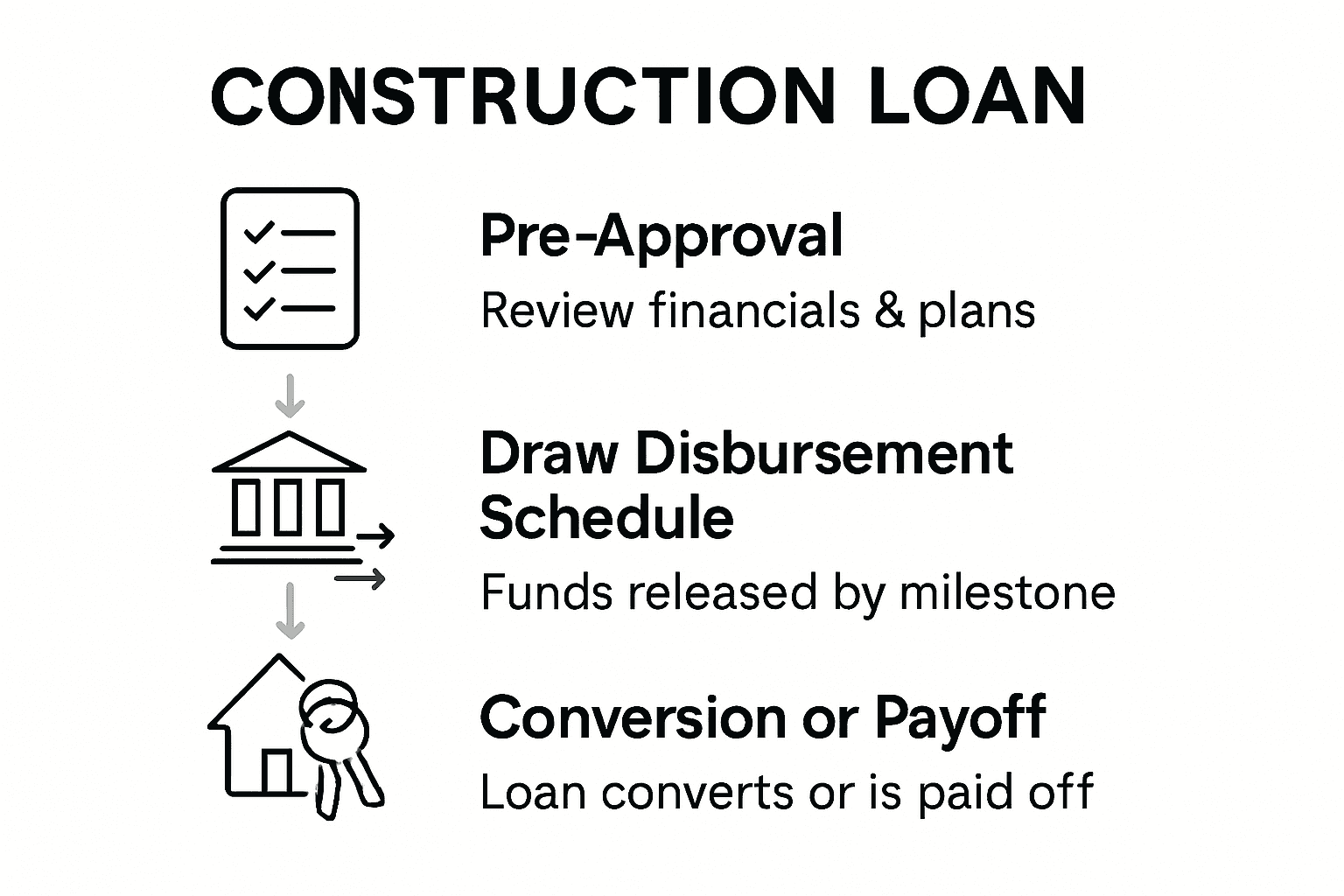

Stages of the Construction Loan Process

Financial institutions meticulously structure construction loan disbursements to minimize risk and ensure project accountability. The construction loan process typically involves multiple sequential stages that require comprehensive documentation, periodic inspections, and carefully controlled fund releases. Unlike traditional mortgages, these loans demand ongoing verification and assessment throughout the entire building project.

The initial stage involves a comprehensive pre-approval process where lenders evaluate the borrower’s financial credentials, project feasibility, and construction plans. This includes detailed review of architectural blueprints, contractor credentials, budget estimates, and comprehensive financial documentation. Once pre-approved, borrowers receive a preliminary loan commitment outlining specific terms, draw schedules, and performance expectations. Subsequent stages involve draw requests, where contractors submit completed work documentation to trigger specific fund releases. Lenders typically conduct on-site inspections to verify work quality, progress, and alignment with original project specifications before authorizing each payment.

Most construction loans follow a structured disbursement schedule broken into key milestones. These commonly include foundation completion, framing, rough mechanical installations, interior finishing, and final completion. Each milestone requires detailed documentation and typically involves an independent inspector verifying work quality and progress. Borrowers must maintain transparent communication with their lender, providing regular updates and promptly addressing any potential delays or budget modifications. As the project nears completion, the loan will either convert to a traditional mortgage or require refinancing, depending on the initial loan structure and borrower preferences.

Pro Tip – Documentation Tracking: Maintain a meticulous digital folder with all project documentation, including contracts, inspection reports, and draw request records, to streamline the loan process and provide immediate evidence of project progress.

Costs, Risks, and Common Pitfalls

Financial institutions carefully analyze construction loan risks to protect both lender and borrower investments. Construction financing involves complex financial dynamics that extend far beyond traditional mortgage structures, presenting unique challenges and potential financial vulnerabilities. The intricate nature of these loans demands comprehensive understanding of potential cost escalations, project complications, and strategic risk management.

Cost Overruns represent one of the most significant financial risks in construction projects. Typical budget inflation ranges between 10% to 25% of original estimates, driven by unexpected material price increases, labor shortages, design modifications, and unforeseen structural challenges. Borrowers must maintain substantial financial buffers and contingency funds to address potential unexpected expenses. Critical risk factors include inadequate initial project planning, unrealistic budget projections, insufficient contractor experience, and volatile market conditions that can dramatically impact material and labor costs.

Beyond financial considerations, construction loans involve complex legal and procedural risks. Common pitfalls include delays in project completion, contractor performance issues, permit challenges, and potential liens from subcontractors or suppliers. Borrowers face additional complications such as potential credit score impacts, interest rate fluctuations during extended construction periods, and potential penalties for missed milestones. Sophisticated borrowers mitigate these risks through comprehensive contract negotiations, thorough contractor vetting, detailed project timelines, and maintaining robust communication channels with both lenders and construction teams.

The following table summarizes the main risks in construction financing and some effective strategies to manage them:

| Common Risk | Typical Impact | How to Reduce It |

|---|---|---|

| Cost Overruns | Extra expenses, possible loan shortfall | Build 15-20% contingency fund |

| Contractor Delays | Project stalls, increased interest cost | Use proven, licensed contractors |

| Permit/Inspection Issues | Construction halts, regulatory penalties | Prepare thorough documentation |

| Interest Rate Changes | Higher repayment costs during build | Lock favorable rate early |

Pro Tip – Risk Mitigation: Develop a comprehensive contingency budget of at least 15-20% above your initial project estimate, and maintain detailed documentation of every contractual agreement and project milestone to protect your financial interests.

Simplify Your Construction Financing Journey with Expert Mortgage Solutions

Understanding the complexities of construction financing can feel overwhelming. From managing draw schedules and contractor approvals to navigating varied loan types like construction-to-permanent loans, you need a trusted partner who can guide you every step of the way. At Craigburn Capital, we specialize in tailored mortgage solutions designed to fit your unique construction project needs, whether you are a first-time builder, an experienced developer, or an owner-builder taking on your own project.

Take control of your construction financing today by partnering with a mortgage brokerage that offers competitive rates, exclusive lending opportunities, and expert advice personalized to your circumstances. Visit Craigburn Capital to explore how our range of financing options and knowledgeable team can help you avoid common pitfalls like cost overruns and contractor delays. Don’t let uncertainty delay your project. Connect with us now for a free consultation and step confidently toward your dream build.

Frequently Asked Questions

What is construction financing?

Construction financing is a specialized lending approach that provides capital to homebuyers and developers to fund new building projects from groundbreaking to completion. Unlike traditional mortgages, these loans cover costs specific to the construction process.

How does the draw schedule work in construction loans?

The draw schedule in construction loans involves releasing funds incrementally as specific project milestones are met. Lenders conduct inspections to verify progress before authorizing subsequent payments, ensuring financial accountability and project oversight.

What are the different types of construction loans available?

There are several types of construction loans, including construction-to-permanent loans, stand-alone construction loans, renovation construction loans, and owner-builder construction loans. Each type serves different financing needs and borrower circumstances.

What documentation is required for a construction loan application?

Applicants for construction loans need to provide comprehensive documentation, including detailed project plans, budget estimates, contractor credentials, proof of income, and asset verification. Proper documentation is crucial for loan approval and project feasibility assessment.

Recommended

- Home Financing Process Explained for First-Time Buyers – Craigburn Capital

- First-Time Homebuyer Step by Step Guide to Success – Craigburn Capital

- Mortgage Terms Explained: Keys to Smarter Home Buying – Craigburn Capital

- How to Qualify for a Mortgage: Step-by-Step Guide for Buyers – Craigburn Capital

- Timeshare Closing Process Explained for Owners – Complete Transfers

- Understanding Trade Finance Solutions: A Clear Guide – Worldwide Express, Inc.