Home Financing Process Explained for First-Time Buyers

Over 60 percent of American home buyers report feeling unprepared for their first mortgage meeting. For anyone dreaming of owning a home, this uncertainty can lead to financial stress or costly setbacks. Learning how to assess your finances, explore the right mortgage options, and navigate the approval process gives you the control and clarity needed for a successful purchase. This guide breaks down each step so you can make informed choices and approach home buying with confidence.

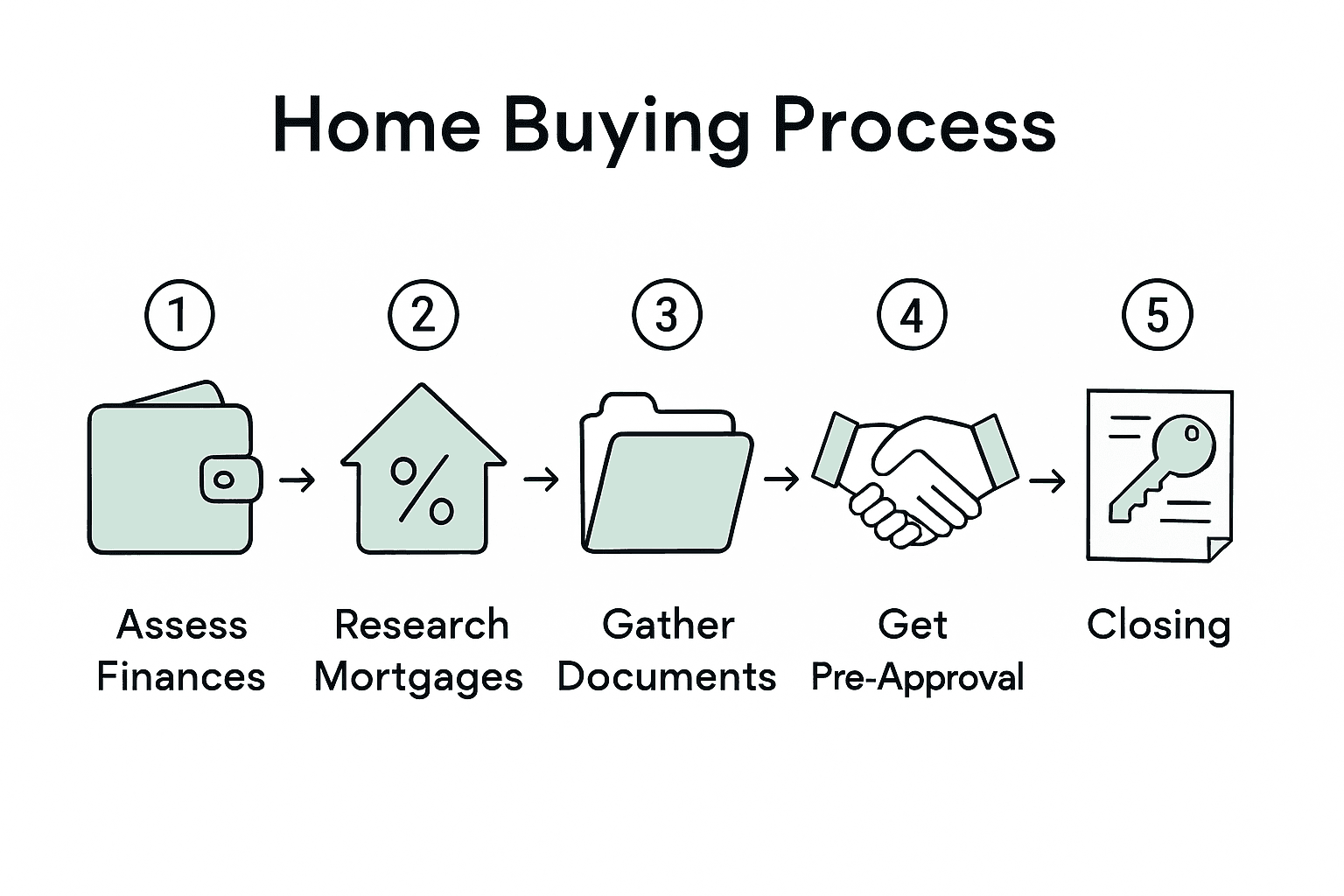

Table of Contents

- Step 1: Assess Your Financial Readiness

- Step 2: Research Mortgage Options and Rates

- Step 3: Gather and Submit Required Documentation

- Step 4: Obtain Pre-Approval From a Lender

- Step 5: Finalize Your Home Loan and Complete Closing

Quick Summary

| Key Takeaway | Explanation |

|---|---|

| 1. Assess Financial Readiness | Evaluate your income, credit, and debts to gauge mortgage eligibility and potential borrowing capacity before buying a home. |

| 2. Research Mortgage Options | Explore different mortgage types, their requirements, and costs to determine the best fit for your financial profile and long-term goals. |

| 3. Gather Necessary Documentation | Compile essential financial documents like tax returns and pay stubs to streamline your mortgage application and avoid delays. |

| 4. Obtain Pre-Approval from Lender | Seek pre-approval to clarify your budget and show sellers you are a serious buyer, making your home search more competitive. |

| 5. Understand Closing Costs | Prepare for closing expenses, typically 2% to 5% of the purchase price, to ensure no surprises at the finalization of your mortgage. |

Step 1: Assess Your Financial Readiness

Before embarking on your home buying journey, understanding your financial landscape is critical. This step involves taking a comprehensive look at your current financial health to determine your mortgage readiness and potential borrowing capacity.

Start by thoroughly evaluating your income stability, credit profile, and existing financial obligations. Key financial qualifications include analyzing your debt to income ratio, employment history, and consistent income streams. Mortgage lenders will scrutinize these factors to assess your ability to manage monthly mortgage payments. Calculate your current monthly income after taxes and subtract all existing debt payments including credit cards, student loans, car payments, and other recurring expenses.

A strong financial foundation requires strategic preparation. Review your credit report, ensuring all information is accurate and your credit score meets minimum lending requirements. Most lenders prefer credit scores above 620, with the most competitive rates available to borrowers scoring 740 or higher. Save aggressively for your down payment, aiming for at least 3.5% to 20% of the home’s purchase price to avoid additional private mortgage insurance costs.

Pro tip: Create a dedicated savings account specifically for your home purchase and automate monthly transfers to build your down payment fund systematically and consistently.

Step 2: Research Mortgage Options and Rates

Navigating the complex world of mortgage options requires strategic research and a clear understanding of how different loan types can impact your financial future. This step involves exploring various mortgage products to find the most suitable financing solution for your specific needs and financial circumstances.

Begin by examining multiple mortgage types including conventional, FHA, VA, and adjustable rate mortgages. Each option carries unique advantages and potential drawbacks. Pay close attention to comprehensive comparison rates that reveal the true cost of borrowing beyond simple interest rates. These rates encompass additional fees and charges, providing a more transparent view of your potential financial commitment. Contact multiple lenders to request detailed loan estimates, comparing interest rates, closing costs, and potential prepayment penalties.

Dig deeper by analyzing how different mortgage terms align with your long term financial goals. Fixed rate mortgages offer stability with consistent monthly payments, while adjustable rate mortgages might provide lower initial rates but carry potential future payment fluctuations. Consider factors like how long you plan to stay in the home, your income stability, and overall risk tolerance when selecting your mortgage product.

Here’s a comparison of common mortgage types to help you identify which may fit your needs:

| Mortgage Type | Down Payment Requirement | Key Benefit | Typical Borrower Profile |

|---|---|---|---|

| Conventional | 5%–20%, varies by lender | Flexible terms, competitive rates | Strong credit and savings habits |

| FHA | Minimum 3.5% | Easier credit qualification | First-time or lower-credit buyers |

| VA | 0% for eligible veterans | No down payment, lower costs | U.S. veterans and service members |

| Adjustable Rate (ARM) | 3%–10%, lender dependent | Low initial rates, variable later | Short-term owners or rate risk-takers |

Pro tip: Create a comprehensive spreadsheet comparing mortgage offers from at least three different lenders, tracking interest rates, closing costs, and total loan expenses to make an informed decision.

Step 3: Gather and Submit Required Documentation

Prepping your mortgage application requires meticulous document collection and organization. This critical step involves assembling a comprehensive financial portfolio that lenders will scrutinize to evaluate your loan eligibility.

Systematic document preparation is essential for a smooth mortgage approval process. Compile a comprehensive file that typically includes proof of income tax returns from the past two years, recent pay stubs covering 30 days, W2 forms, bank statements showing checking and savings account balances, documentation of additional income sources like alimony or rental income, and detailed records of your current assets and liabilities. For self employed applicants this means providing additional documentation such as profit and loss statements and business tax returns.

Each financial document plays a crucial role in demonstrating your fiscal stability and borrowing potential. Mortgage lenders will carefully examine your employment history, verifying consistent income and job stability. Be prepared to provide contact information for your current employer and potentially previous employers to facilitate verification. Include detailed information about any investment accounts retirement savings and additional financial resources that showcase your overall financial strength.

Below is a summary of required documentation you should prepare before applying for a mortgage:

| Document Type | Purpose | Common Examples |

|---|---|---|

| Proof of Income | Verifies ability to repay loan | Pay stubs, tax returns, W-2 forms |

| Asset Statements | Confirms available funds | Bank, retirement, investment accounts |

| Debt Documentation | Assesses monthly obligations | Loan statements, credit card bills |

| Employment History | Validates job stability | Employer contact info, past records |

Pro tip: Create a dedicated digital folder with high resolution scans of all required documents organized chronologically to streamline the application process and quickly respond to any lender requests.

Step 4: Obtain Pre-Approval from a Lender

Securing a mortgage pre-approval is a pivotal milestone in your home buying journey that transforms your home ownership dreams from theoretical to practical. This critical step provides a clear financial roadmap and signals to sellers that you are a serious and qualified buyer.

Strategic pre-approval preparation involves working closely with a lender to thoroughly evaluate your financial standing. During this process, lenders will conduct a comprehensive review of your credit history, income, employment stability, and overall financial health. They will issue a pre-approval letter specifying the maximum loan amount you qualify for based on their detailed assessment. This document not only helps you understand your precise home buying budget but also demonstrates to real estate agents and sellers that you have been financially vetted by a professional lending institution.

When pursuing pre-approval, expect to provide extensive documentation including proof of income, tax returns, bank statements, and detailed information about your assets and liabilities. Some lenders may require additional documentation depending on your specific financial situation. The pre-approval process typically involves a hard credit inquiry, which might temporarily impact your credit score, so timing and preparation are crucial. Remember that pre-approval is different from pre-qualification pre-approval carries more weight and provides a more accurate representation of your borrowing potential.

Pro tip: Request pre-approval letters from multiple lenders within a 14 day window to minimize the impact on your credit score and compare potential loan terms effectively.

Step 5: Finalize Your Home Loan and Complete Closing

The closing stage represents the culmination of your home buying journey where ownership officially transfers and your mortgage becomes a reality. This critical phase demands meticulous attention to detail and comprehensive understanding of the legal and financial processes involved.

Comprehensive closing documentation requires careful review and verification of multiple critical financial documents. During the closing meeting you will sign numerous legal papers including the promissory note affirming your commitment to repay the mortgage loan, the mortgage or deed of trust that secures the loan against the property, and the closing statement detailing all financial transactions. Your lender will have a closing agent or attorney present to guide you through each document ensuring you understand the terms and obligations associated with your home financing.

Expect to pay closing costs which typically range between 2% to 5% of the total home purchase price. These expenses include loan origination fees, appraisal costs, title insurance, property taxes, and other administrative expenses. Bring a certified or cashiers check to cover these costs or arrange for a wire transfer in advance. Prior to closing you will conduct a final walkthrough of the property to confirm its condition matches the initial agreement and no unexpected damages have occurred. Once all documents are signed and funds are transferred you will receive the keys to your new home marking the official completion of your home buying process.

Pro tip: Request a detailed closing cost breakdown at least three days before your closing date to review all expenses and ensure there are no unexpected charges or discrepancies.

Empower Your First-Time Home Buying Journey with Expert Mortgage Solutions

Navigating each step of the home financing process can feel overwhelming, especially when assessing your financial readiness, comparing mortgage options, organizing documentation, or securing pre-approval. If you are a first-time buyer striving to overcome credit challenges, self-employment income complexities, or simply seeking competitive rates, tailored guidance is essential. The article highlights common pain points such as understanding down payment requirements, coordinating paperwork, and finding the right loan type that fits your unique financial profile.

Discover how Craigburn Capital specializes in turning these challenges into opportunities with personalized mortgage solutions designed for first-time buyers. Benefit from access to exclusive unadvertised rates, specialized programs for less-than-perfect credit, and expert support throughout your financing journey. Don’t let paperwork or confusing mortgage terms hold you back. Act now by visiting Craigburn Capital’s homepage to explore how their first-time homebuyer assistance programs and private lending options can help you secure your dream home with confidence.

Frequently Asked Questions

What should I assess before starting the home financing process as a first-time buyer?

Before starting the home financing process, assess your financial readiness by reviewing your income stability, credit profile, and current debts. Gather your income statements and calculate your debt-to-income ratio to determine how much you can realistically borrow.

How do I choose the right mortgage option for my situation?

To choose the right mortgage option, research various types such as conventional, FHA, VA, and adjustable rate mortgages, comparing their advantages and disadvantages. List your financial needs and long-term goals to find the mortgage that best fits your circumstances, whether you prefer stable payments or lower initial rates.

What documents do I need to prepare for my mortgage application?

You need to prepare essential documents including proof of income, asset statements, and debt documentation for your mortgage application. Organize your tax returns, pay stubs, and bank statements in a digital folder to streamline the process and ensure all information is readily available when requested by lenders.

How can I get pre-approved for a mortgage?

To get pre-approved for a mortgage, contact a lender and provide your financial information such as income, debts, and assets. Expect to receive a pre-approval letter specifying the maximum loan amount you qualify for, which demonstrates to sellers that you are a serious buyer.

What should I expect during the closing process of my home loan?

During the closing process, you will sign legal documents including the mortgage deed and the closing statement, transferring ownership of the property. Prepare to pay closing costs, typically ranging from 2% to 5% of the purchase price, and conduct a final walkthrough to ensure the property is in the agreed condition.

How can I manage closing costs effectively?

To manage closing costs effectively, request a detailed breakdown from your lender at least three days before your closing date. This allows you to review all expected expenses and resolve any discrepancies, preventing unexpected charges on closing day.