First-Time Homebuyer Step by Step Guide to Success

Over 65 percent of American adults dream of owning their own home, yet many feel overwhelmed by the process and unsure where to start. Getting from wishful thinking to a set of keys means understanding your finances, navigating mortgage choices, and knowing exactly what to expect at each step. This guide explains the entire journey, breaking down the essential decisions every buyer must make to help you approach American homeownership with confidence and practical knowledge.

Table of Contents

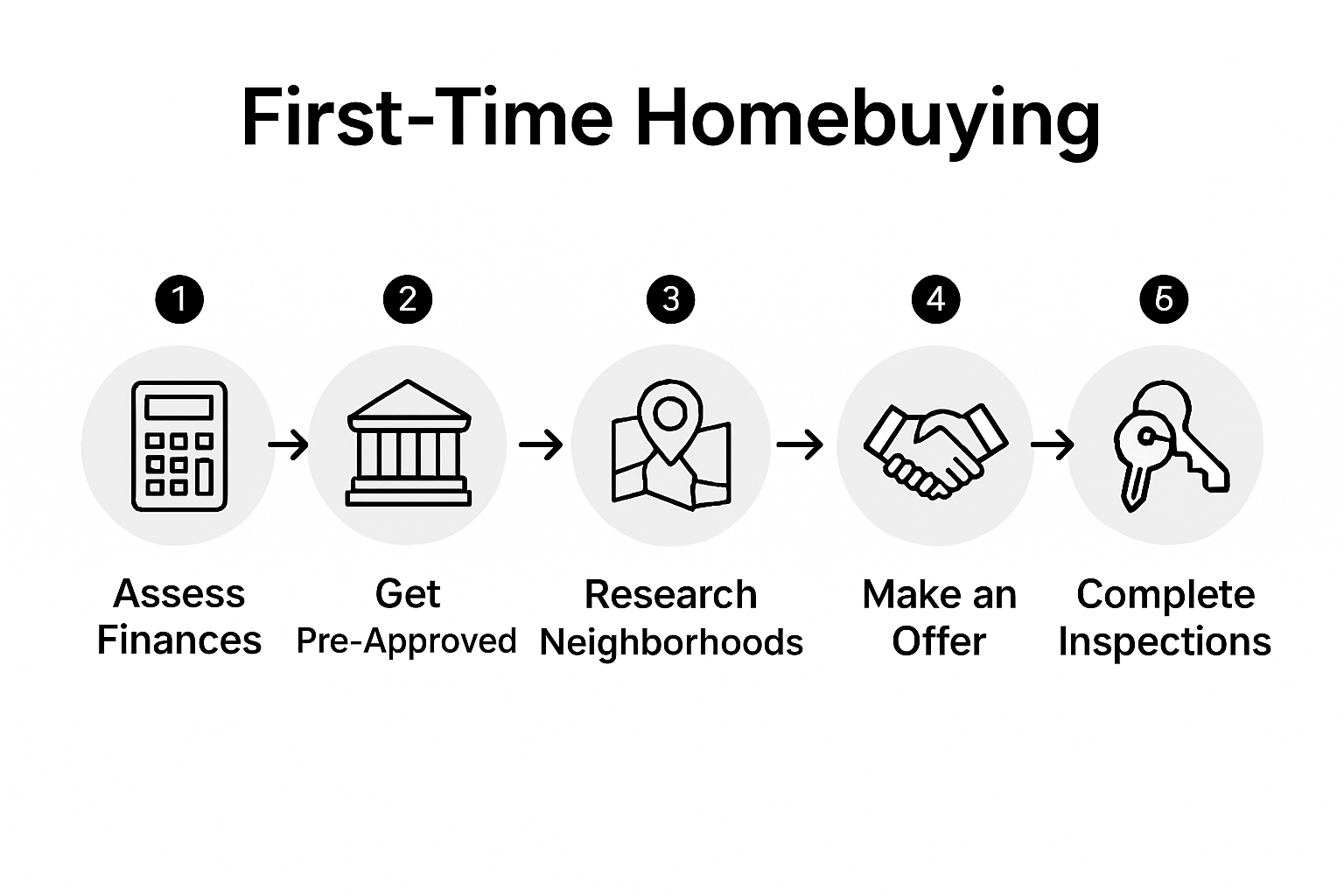

- Step 1: Assess Financial Readiness And Set A Budget

- Step 2: Explore Mortgage Options And Get Pre-Approved

- Step 3: Research Neighborhoods And Identify Ideal Homes

- Step 4: Make An Offer And Negotiate Terms

- Step 5: Complete Inspections And Secure Financing

- Step 6: Finalize Closing And Move Into Your New Home

Quick Summary

| Main Insight | Detailed Explanation |

|---|---|

| 1. Assess Financial Readiness First | Review your spending and financial health to determine how much home you can afford, aiming for housing expenses under 28% of your income. |

| 2. Explore Mortgage Options Thoroughly | Research different mortgage types and get pre-approved to understand borrowing power and show credibility to sellers. |

| 3. Conduct Detailed Neighborhood Research | Investigate neighborhoods carefully by examining local amenities and considering lifestyle factors to find a suitable location. |

| 4. Craft a Competitive Offer | Create offers based on market research and stay calm during negotiations, being ready to include contingencies for protection. |

| 5. Complete Inspections Before Closing | Hire a professional inspector to evaluate property condition and ensure there are no unexpected issues before finalizing your mortgage. |

Step 1: Assess Financial Readiness and Set a Budget

Home buying starts with understanding your financial landscape and setting realistic expectations. Before diving into property searches, you need a clear picture of what you can actually afford. The goal here is building a budget that supports your homeownership dreams without creating financial strain.

Begin by reviewing your monthly spending and financial health. Pull your credit reports and calculate your total monthly income after taxes. Track every expense meticulously credit card bills, utilities, groceries, entertainment, and existing debt payments. Your target should be having a comfortable buffer between your income and potential mortgage costs.

Most financial experts recommend that your total housing expenses not exceed 28% of your gross monthly income. This means if you earn $6000 monthly, aim to keep mortgage payments around $1680 or less. Remember to factor in additional costs beyond the mortgage principal and interest property taxes, homeowners insurance, potential private mortgage insurance, and maintenance expenses. A good rule of thumb is budgeting an extra 1 to 3% of your home’s value annually for repairs and upkeep.

Pro tip: Create a dedicated savings account for your home purchase. Aim to save at least 3 to 6 months of living expenses as an emergency fund before committing to a mortgage. This provides a critical financial safety net and makes you a more attractive candidate to lenders.

As you move forward, you will now transition into evaluating your down payment strategy and exploring mortgage options that align with your budget.

Step 2: Explore Mortgage Options and Get Pre-Approved

Now that you have a solid understanding of your financial readiness, it is time to dive into mortgage options and secure your pre-approval. This critical step transforms your home buying dream from a concept into a concrete plan by establishing exactly how much house you can afford and demonstrating your credibility to sellers.

Start by researching different mortgage types and understanding their unique requirements, which include conventional loans, Federal Housing Administration (FHA) loans, Veterans Affairs (VA) loans, and specialized first-time homebuyer programs. Each loan type comes with distinct advantages and qualification criteria. Conventional loans typically require higher credit scores and larger down payments, while FHA loans offer more flexibility for buyers with lower credit scores or smaller savings.

To get pre-approved, you will need to gather comprehensive financial documentation. This includes recent pay stubs, W-2 forms, tax returns for the past two years, bank statements, proof of additional income sources, and a detailed list of your assets and debts. Lenders will perform a thorough review of your financial history, checking your credit score, debt-to-income ratio, and overall financial stability. A strong pre-approval letter not only tells you exactly how much you can borrow but also signals to sellers that you are a serious and qualified buyer.

Pro tip: Shop around and get pre-approval letters from multiple lenders. Interest rates and loan terms can vary significantly between financial institutions. Do not simply accept the first offer you receive compare at least three different lenders to ensure you are getting the most competitive rates and terms for your specific financial situation.

As you complete the pre-approval process, you will be ready to start your home search with confidence knowing exactly what price range you can afford and having a powerful tool to make your offer stand out in competitive real estate markets.

Step 3: Research Neighborhoods and Identify Ideal Homes

With your mortgage pre-approval secured, you are now ready to embark on the exciting journey of finding your perfect home. This step transforms your financial groundwork into a tangible property search, focusing on discovering neighborhoods and homes that align with your lifestyle and long-term goals.

Begin by researching comprehensive neighborhood characteristics and community resources that will impact your quality of life. Look beyond the physical house and evaluate critical factors such as local school districts, crime rates, proximity to work, public transportation, healthcare facilities, and future development plans. Utilize online tools, municipal websites, and local government resources to gather detailed insights about potential neighborhoods. Consider factors like walkability scores, community amenities, local parks, shopping centers, and the overall demographic mix.

As you investigate potential homes, create a structured checklist of your must-have features and nice-to-have amenities. This list might include specific requirements like number of bedrooms, square footage, kitchen layout, outdoor space, or architectural style. Compare your ideal home criteria against available properties in your target neighborhoods. Do not compromise on your core requirements, but remain flexible about cosmetic features that can be modified later. Consider attending open houses, scheduling private viewings, and driving through neighborhoods at different times of day to get a comprehensive understanding of the area’s character and potential challenges.

Pro tip: Leverage technology and local expertise during your search. Use real estate websites with advanced filtering options, consult local real estate agents familiar with specific neighborhoods, and connect with current residents through community forums or social media groups. These resources can provide nuanced insights that online data might not reveal.

As you complete your neighborhood and home research, you will be prepared to make an informed decision and move forward with confidence in selecting a property that meets both your immediate needs and future aspirations.

Step 4: Make an Offer and Negotiate Terms

With your perfect home identified, you are now entering the critical phase of making an offer and negotiating the purchase terms. This stage requires strategic thinking, emotional discipline, and a clear understanding of market dynamics to successfully secure your dream property.

Understand the complexities of crafting a competitive real estate offer that balances your financial constraints with market realities. Your offer should be based on comprehensive research including recent comparable sales in the neighborhood, current market conditions, the property’s condition, and your pre-approval amount. Work closely with your real estate agent to determine a strategic initial offer price that is attractive to the seller while protecting your financial interests. Include specific contingencies that safeguard your investment such as home inspection, appraisal, and financing contingencies which provide legal exit points if significant issues arise during the due diligence process.

Prepare for potential counteroffers by establishing your maximum budget and walking away point before negotiations begin. Sellers may respond to your initial offer with alternative terms or pricing, and your ability to remain calm and objective is crucial. Consider non price-related negotiation points such as closing date flexibility, inclusion of appliances or furniture, repair credits, or other concessions that could make your offer more appealing. Your pre-approval letter and ability to provide a substantial earnest money deposit can also strengthen your negotiating position.

Pro tip: Always maintain professional communication and emotional neutrality during negotiations. Real estate transactions are business agreements where personal attachment can undermine your strategic positioning. Document every communication, respond promptly to counteroffers, and be prepared to compromise on non critical aspects while holding firm on your core requirements.

As negotiations progress, you will move closer to finalizing the purchase agreement and preparing for the comprehensive home inspection and appraisal process.

Step 5: Complete Inspections and Secure Financing

You are now entering the most critical phase of your home buying journey where thorough due diligence meets financial finalization. This step transforms your offer into a concrete transaction by ensuring the property meets your expectations and your financing is rock solid.

Navigate the comprehensive home inspection process with meticulous attention to detail. Hire a professional home inspector who will conduct an exhaustive examination of the property’s structural integrity, electrical systems, plumbing, roof condition, foundation, and potential hidden defects. Review the inspection report carefully and understand that not every issue requires renegotiation. Focus on significant structural problems, safety concerns, or expensive repair needs that could impact the home’s value or your future living conditions. Consider requesting repair credits or price adjustments for major issues discovered during the inspection.

Simultaneously, finalize your mortgage by carefully reviewing loan estimates and understanding all associated terms and conditions. Compare the final loan documents against your initial pre-approval, paying close attention to interest rates, closing costs, monthly payment structures, and any potential prepayment penalties. Work closely with your mortgage professional to ensure all financial documentation is accurate and complete. Verify that your loan terms align precisely with your initial expectations and that you fully comprehend all aspects of the mortgage agreement.

Pro tip: Maintain open communication with both your real estate agent and mortgage professional during this phase. Request detailed explanations for any complex terms or conditions you do not immediately understand. Do not hesitate to ask questions or seek clarification about any aspect of the inspection report or loan documents.

As you complete these final verification steps, you will be preparing for the ultimate milestone of closing on your new home and taking possession of your first property.

Step 6: Finalize Closing and Move Into Your New Home

You have reached the pinnacle moment of your home buying journey where months of planning and preparation culminate in officially becoming a homeowner. This final step transforms your dream into reality as you prepare to take legal possession of your new property.

Navigate the complex closing process with thorough preparation and attention to detail. Review your closing disclosure documents meticulously at least three days before the scheduled closing date. These documents outline your final loan terms, closing costs, and financial obligations. Bring a certified or cashier’s check for your down payment and closing expenses, along with multiple forms of government issued photo identification. Confirm the exact amount required with your closing agent beforehand to avoid any last minute complications. Attend the closing with your real estate agent or attorney who can help you understand each document you will be signing.

Prepare for the physical move by creating a strategic transition plan. Schedule utility transfers, update your address with postal services, banks, and important contacts, and arrange professional movers or coordinate with friends and family for assistance. Conduct a final walkthrough of the property immediately before closing to ensure the home is in the condition agreed upon in your purchase contract. Check that all negotiated repairs have been completed, no new damages have occurred, and the property is clean and ready for your arrival.

Pro tip: Bring a printed checklist to your closing and verify each document carefully. Do not feel pressured to sign anything you do not fully understand. Ask questions, request clarifications, and take your time reviewing each document. Remember that closing agents and professionals are there to guide you through this process.

As you complete the closing and receive your house keys, you will have officially achieved the significant milestone of homeownership and begun your exciting new chapter of personal and financial growth.

Take Charge of Your First Home Purchase with Expert Mortgage Solutions

Navigating the steps from budgeting to closing can feel overwhelming for first-time buyers. This guide highlights key challenges like setting a realistic budget, securing mortgage pre-approval, and negotiating offers. You want confidence, clarity, and competitive rates that fit your financial situation. At Craigburn Capital, we specialize in tailored mortgage solutions that empower you through every stage of your home buying journey. Whether you need help with private lending, first-time homebuyer programs, or overcoming credit hurdles, our team is ready to assist.

Ready to make your homeownership dream a reality without the stress and uncertainty? Visit Craigburn Capital today to explore options designed specifically for first-time buyers. Learn more about first-time homebuyer assistance and gain access to exclusive rates and personalized advice that can set you apart in a competitive market. Don’t wait until the last minute. Get expert support now and move confidently through every critical step toward buying your perfect home.

Frequently Asked Questions

What should I do first as a first-time homebuyer?

Start by assessing your financial readiness and setting a budget. Review your monthly income, expenses, and create a comfortable budget that supports your homeownership goals without financial strain.

How do I explore mortgage options as a first-time homebuyer?

Research different mortgage types and their requirements, including conventional, FHA, and VA loans. Gather necessary financial documentation and seek pre-approval to understand how much you can borrow before house hunting.

What factors should I consider when researching neighborhoods?

Evaluate key characteristics like local school districts, crime rates, and proximity to work. Use online tools to gather detailed insights about potential neighborhoods to ensure they align with your lifestyle goals.

How can I make a competitive offer on a home?

Craft a competitive offer based on your research of comparable sales and market conditions. Include contingencies for inspection and appraisal, and be prepared for counteroffers to strengthen your negotiation position.

What is the home inspection process, and why is it important?

The home inspection process involves hiring a professional to assess the property for defects and potential issues. This is crucial for understanding the home’s condition and can help you negotiate repairs or price adjustments if needed.

What should I do on closing day as a first-time homebuyer?

Review your closing disclosure carefully prior to the closing date and bring necessary payment methods and identification. Conduct a final walkthrough of the property to ensure it meets the agreed conditions before signing documents.

Recommended

- First-Time Homebuyer Assistance: Unlocking Homeownership – Craigburn Capital

- 7 Essential Steps in a First-Time Homebuyer Checklist – Craigburn Capital

- First-Time Homebuyer Programs: Unlocking Homeownership Opportunities – Craigburn Capital

- Complete Guide to Guidelines for First-Time Buyers – Craigburn Capital

- Mökki-projektin aloitusopas: Näin onnistut omassa hankkeessa – Huvila Seppälä

- How to Handle HVAC Repairs Step-by-Step for Homeowners