Types of Mortgage Financing – Which Is Right for You?

Over 60 percent of first-time Canadian and American homebuyers report feeling overwhelmed by the range of mortgage options available today. For those in Halifax and Surrey, especially with limited credit history, the search for affordable home financing can be both stressful and confusing. Understanding how modern mortgage solutions work and which tailored options fit your situation best can make the difference between uncertain guesswork and confident homeownership.

Table of Contents

- What Mortgage Financing Means Today

- Fixed-Rate, Variable, and Hybrid Mortgages Explained

- Government-Backed Mortgages and Their Benefits

- Mortgages for Buyers With Limited Credit

- Comparing Costs, Risks, and Long-Term Impact

- Common Mistakes First-Time Buyers Make

Key Takeaways

| Point | Details |

|---|---|

| Understand Mortgage Types | Familiarize yourself with fixed-rate, adjustable-rate, and hybrid mortgages to find the best fit for your financial situation. |

| Explore Government-Backed Options | Consider FHA, VA, and USDA loans for flexible qualification criteria and lower down payments for homeownership. |

| Assess Total Costs | Evaluate the full financial implications of different mortgage options, including taxes and maintenance, beyond just the monthly payment. |

| Avoid Common Buyer Mistakes | Plan for all costs associated with homeownership to prevent financial strain and ensure you’re financially prepared before buying. |

What Mortgage Financing Means Today

Mortgage financing represents a sophisticated financial arrangement where lenders provide funds for property acquisition, enabling individuals to purchase homes without requiring full upfront payment. Modern mortgage financing has dramatically transformed from traditional models, now offering diverse strategies that accommodate varying financial profiles and risk tolerances.

The contemporary mortgage landscape incorporates innovative products designed to balance borrower needs with lender risk management. Hybrid adjustable-rate mortgages (ARMs) exemplify this evolution, combining fixed and variable interest rate periods to create more flexible lending structures. These sophisticated financial instruments allow borrowers to benefit from initial lower rates while providing lenders with mechanisms to adjust for market fluctuations.

Today’s mortgage financing ecosystem extends far beyond simple lending transactions. Borrowers now have access to multiple financing options including conventional mortgages, government-backed loans, jumbo mortgages, and specialized programs for first-time homeowners. Each option carries unique qualification requirements, interest rates, and long-term financial implications. Factors like credit score, income stability, down payment capabilities, and debt-to-income ratios significantly influence mortgage accessibility and terms.

Pro Tip: Research Multiple Options: Before committing to a mortgage, thoroughly compare at least three different lender offerings to ensure you secure the most favorable terms and interest rates for your specific financial situation.

Fixed-Rate, Variable, and Hybrid Mortgages Explained

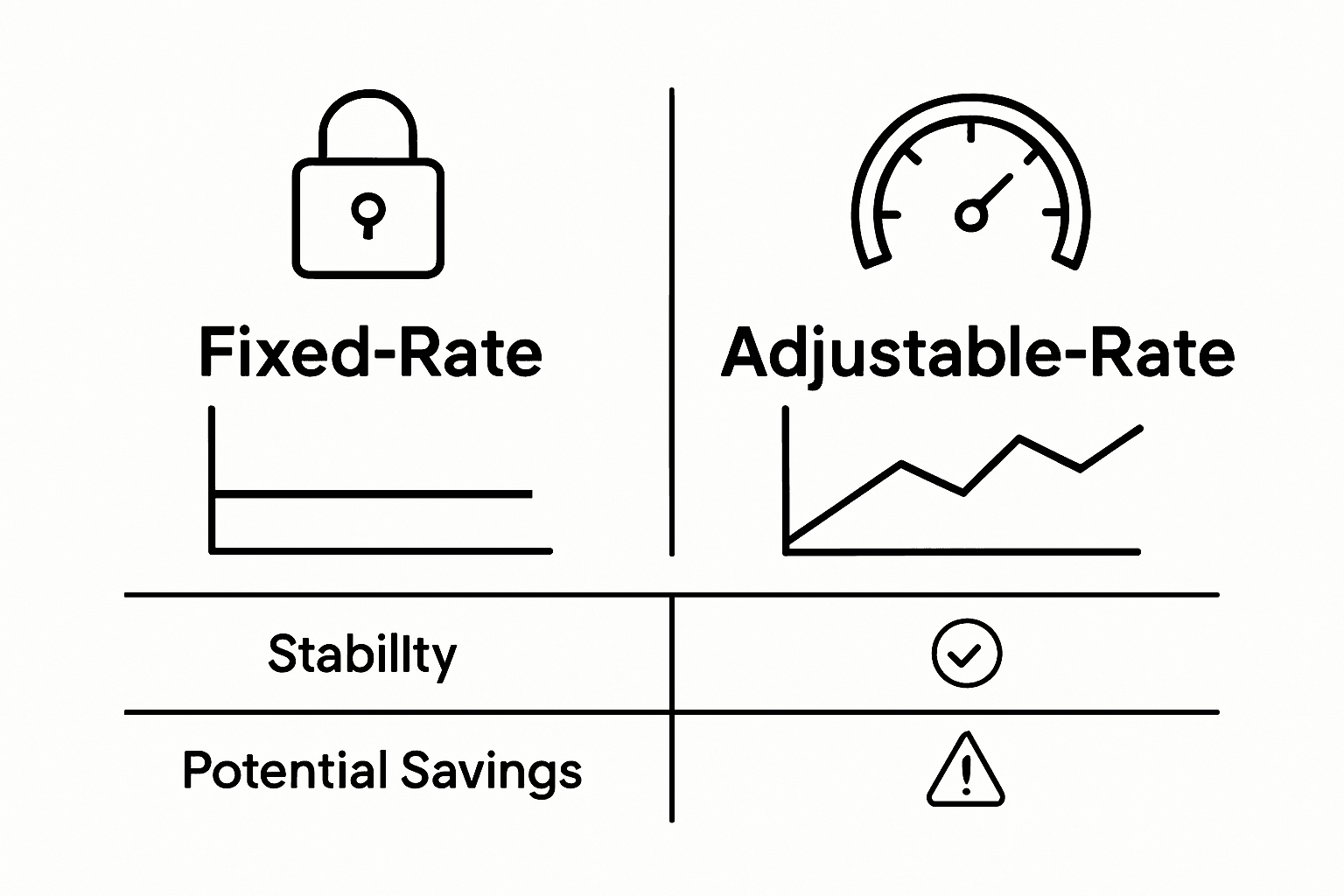

Fixed-rate mortgages represent a cornerstone of home financing, offering predictable and stable payment structures for homeowners. This mortgage type maintains a consistent interest rate throughout the entire loan term, allowing borrowers to create precise long-term financial planning without worrying about unexpected payment fluctuations. Homeowners appreciate the reliability of fixed-rate mortgages, as monthly principal and interest payments remain constant, providing a sense of financial security.

Adjustable-rate mortgages (ARMs) present a more dynamic approach to home lending. These mortgage products feature interest rates that periodically adjust based on specific market indexes, creating potential for both opportunities and risks. Initial ARM rates are typically lower than fixed-rate mortgages, which can make them attractive for borrowers expecting short-term ownership or anticipating income increases. However, the potential for rate adjustments means monthly payments could increase significantly over time, requiring careful financial assessment.

Hybrid mortgages blend characteristics of fixed and adjustable-rate structures, offering a sophisticated compromise for borrowers seeking flexibility. These innovative financial products typically start with a fixed-rate period (often 5, 7, or 10 years) before transitioning to an adjustable-rate framework. This approach allows borrowers to benefit from initial stability while maintaining potential long-term rate adjustments. The specific terms and transition mechanisms vary, making it crucial for potential homeowners to carefully analyze the complete mortgage structure before commitment.

Pro Tip: Rate Comparison Strategy: Always calculate the total potential cost over the full loan term, not just initial monthly payments, to understand the true financial impact of different mortgage types.

Here’s a comparison of common mortgage types and who they best serve:

| Mortgage Type | Typical Borrower Profile | Key Benefit | Main Risk/Consideration |

|---|---|---|---|

| Fixed-Rate | Long-term planners | Predictable payments | Higher initial interest rate |

| Adjustable-Rate | Short-term owners, risk-tolerant | Lower starting rate | Payments may rise significantly |

| Hybrid/ARM | Those wanting initial stability | Mix of stability/flexibility | Rate may adjust after set period |

| Government-Backed | First-time or credit-challenged | Easier qualification | Specific eligibility requirements |

| Jumbo | Buyers of high-value properties | Higher loan limits | Stricter qualification standards |

Government-Backed Mortgages and Their Benefits

Government-backed mortgages represent a critical pathway to homeownership for many Americans who might struggle with traditional lending requirements. These specialized mortgage programs, typically offered through agencies like the Federal Housing Administration (FHA), Department of Veterans Affairs (VA), and United States Department of Agriculture (USDA), provide unique opportunities for individuals with limited financial resources or unconventional financial backgrounds.

The primary advantages of government-backed mortgages include significantly reduced barriers to entry for homeownership. These programs often feature more flexible credit score requirements, allowing borrowers with less-than-perfect credit histories to qualify for home loans. Additionally, many government-backed mortgage options offer lower down payment thresholds compared to conventional loans, sometimes as low as 3.5% or even zero down payment for qualified veterans, making homeownership substantially more accessible for first-time buyers and those with limited savings.

Each government-backed mortgage program comes with distinct eligibility criteria and unique benefits. FHA loans typically appeal to first-time homebuyers and those with moderate credit scores, offering more lenient qualification standards. VA loans provide exceptional benefits for military service members and veterans, often featuring no down payment requirements and competitive interest rates. USDA loans target rural and suburban homebuyers, providing zero-down-payment options for those purchasing homes in designated areas. These specialized programs demonstrate the government’s commitment to expanding homeownership opportunities across diverse population segments.

Pro Tip: Documentation Preparation: Gather all necessary financial documents, including tax returns, employment verification, and credit reports, before applying for a government-backed mortgage to streamline the application process and improve your approval chances.

This summary helps you quickly compare government-backed loan options:

| Program | Who Qualifies | Down Payment | Unique Benefit |

|---|---|---|---|

| FHA Loan | Moderate credit homebuyers | As low as 3.5% | Flexible credit standards |

| VA Loan | Veterans, service members | Zero | No PMI, competitive rates |

| USDA Loan | Rural/suburban buyers | Zero | Location-specific eligibility |

Mortgages for Buyers With Limited Credit

Mortgage options for buyers with limited credit represent a critical financial lifeline for individuals struggling to navigate traditional lending landscapes. These specialized financing solutions acknowledge that credit history does not always perfectly reflect an individual’s financial responsibility or ability to make consistent mortgage payments. Alternative lending approaches have emerged to address the unique challenges faced by borrowers with minimal or challenged credit profiles.

Alternative mortgage strategies for credit-challenged buyers include several targeted approaches. Government-backed programs like FHA loans provide more flexible credit requirements, often accepting credit scores as low as 580 with appropriate down payment provisions. Some lenders offer non-traditional credit assessment methods, examining consistent payment histories for utilities, rent, and other recurring expenses instead of relying solely on conventional credit scores. This approach allows responsible individuals with limited formal credit histories to demonstrate financial reliability through alternative documentation.

Additional pathways for buyers with limited credit include seeking co-signers with strong credit profiles, exploring private mortgage insurance options, and working with specialized B-lender programs designed for borrowers outside traditional lending parameters. Some innovative financing models incorporate manual underwriting processes, where loan officers conduct comprehensive financial reviews that go beyond standard credit score metrics. These strategies recognize that creditworthiness encompasses more than numerical credit ratings, considering factors like employment stability, income consistency, and overall financial management.

Pro Tip: Credit Building Strategy: Start establishing a positive credit history at least 12 months before applying for a mortgage by opening a secured credit card, making small recurring purchases, and consistently paying the full balance each month.

Comparing Costs, Risks, and Long-Term Impact

Research on mortgage financial strategies reveals the critical importance of understanding the nuanced financial implications of different mortgage structures. Each mortgage type presents a unique balance of immediate affordability and long-term financial consequences, requiring borrowers to carefully evaluate their personal financial landscape, career trajectory, and risk tolerance before making a commitment.

Fixed-rate mortgages offer predictable monthly payments and protection against market volatility, typically featuring higher initial interest rates that provide stability throughout the loan term. Adjustable-rate mortgages, conversely, present lower introductory rates with the potential for significant payment fluctuations based on market conditions. Economic research indicates that variable-rate mortgages can create more pronounced financial system impacts during interest rate shocks, making them a higher-risk option for financially sensitive borrowers.

Comprehensive mortgage cost analysis extends beyond simple interest rate comparisons. Potential homebuyers must consider additional factors such as private mortgage insurance requirements, potential refinancing costs, tax implications, and long-term equity building potential. Some mortgage structures may appear more affordable initially but could result in substantially higher total payments over the loan’s lifetime. Critical evaluation involves calculating total cost of ownership, including closing costs, potential rate adjustments, and the impact of different loan terms on overall financial health.

Pro Tip: Financial Projection Strategy: Create a detailed spreadsheet comparing total lifetime costs for different mortgage options, factoring in potential interest rate changes, additional fees, and your expected income growth to make a truly informed decision.

Common Mistakes First-Time Buyers Make

First-time homebuyers frequently encounter financial pitfalls that can significantly impact their long-term financial stability. Navigating the complex mortgage landscape requires careful preparation and a thorough understanding of the potential mistakes that can derail homeownership dreams. Awareness and strategic planning are essential to avoiding these common financial traps.

One of the most critical errors first-time buyers make involves underestimating the total cost of homeownership. Beyond the mortgage payment, potential homeowners must budget for property taxes, homeowners insurance, maintenance costs, and unexpected repairs. Many buyers focus solely on the monthly mortgage payment without considering additional expenses like utility bills, landscaping, home repairs, and potential homeowners association fees. These overlooked costs can quickly transform an seemingly affordable home into a financial burden.

Another significant mistake is failing to thoroughly assess personal financial readiness. Buyers often rush into homeownership without establishing a robust emergency fund, maintaining a stable credit history, or understanding their true budget limitations. Some individuals stretch their finances too thin by purchasing at the maximum loan amount they qualify for, leaving no financial cushion for unexpected expenses or potential income disruptions. Additionally, first-time buyers frequently neglect to get pre-approved for a mortgage, which can lead to disappointment and wasted time searching for homes outside their actual affordability range.

Pro Tip: Financial Preparation Strategy: Create a comprehensive budget that includes all housing-related expenses, aiming to keep total housing costs below 28% of your gross monthly income, and maintain a separate emergency fund covering at least 3-6 months of total housing expenses.

Discover Your Ideal Mortgage Solution with Expert Guidance

Choosing the right mortgage financing option can feel overwhelming with so many choices like fixed-rate, adjustable-rate, hybrid mortgages, and government-backed loans. The challenge is not just in understanding terms but in matching these options to your unique financial situation, goals, and risk tolerance. Many borrowers struggle with concerns about fluctuating payments, qualifying with limited credit, or finding special programs tailored for first-time buyers or self-employed individuals.

At Craigburn Capital, we understand these critical pain points and offer tailored mortgage solutions designed to empower you. Whether you need assistance navigating government-backed loans, want competitive rates on private lending, or require specialized commercial financing, our expertise can simplify the process. Act now to avoid costly home-buying mistakes and secure a mortgage that fits your lifestyle.

Ready to explore mortgage options that truly work for you Visit Craigburn Capital for access to exclusive rates and personalized advice. Don’t wait—your perfect mortgage is just a conversation away. Explore our first-time homebuyer assistance and discover how we help buyers with credit challenges overcome obstacles. Start your journey to smart home financing today at Craigburn Capital.

Frequently Asked Questions

What are the different types of mortgage financing available today?

The main types of mortgage financing include fixed-rate mortgages, adjustable-rate mortgages (ARMs), hybrid mortgages, government-backed loans, and jumbo loans. Each has unique features and benefits suitable for different borrowers.

How do fixed-rate and adjustable-rate mortgages differ?

Fixed-rate mortgages have a consistent interest rate for the entire loan term, providing predictable payments, while adjustable-rate mortgages feature interest rates that can change over time, often starting lower but carrying the risk of increased payments.

What are government-backed mortgages, and who can benefit from them?

Government-backed mortgages, such as FHA, VA, and USDA loans, provide options for buyers with lower credit scores or limited financial resources. They typically have lower down payment requirements, making homeownership more accessible, especially for first-time buyers.

How can I improve my chances of qualifying for a mortgage?

To improve your chances of qualifying, maintain a stable income, build your credit score, minimize debt-to-income ratio, and gather necessary financial documents to streamline the application process.

Recommended

- Commercial Mortgage Explained: Complete Guide for 2025 – Craigburn Capital

- Mortgage Terms Explained: Keys to Smarter Home Buying – Craigburn Capital

- Mortgage Insurance in Canada – How It Impacts Homebuyers – Craigburn Capital

- Why Work With Mortgage Brokers: Smarter Home Financing – Craigburn Capital