What Is Mortgage Term? Impact on First-Time Buyers

Most first-time homebuyers in Halifax and Surrey are surprised to learn that nearly 60 percent of American buyers choose a 30-year mortgage term, but not for the reasons most expect. The idea of finding a mortgage when your credit is less than perfect feels daunting, yet understanding how term lengths work can open doors you may not realize exist. This guide clears up common myths around mortgage terms and highlights what actually matters for first-time buyers hoping to secure their new home in Canada.

Table of Contents

- Mortgage Term Defined And Common Myths

- Different Mortgage Term Lengths Explained

- How Mortgage Term Affects Monthly Payments

- Fixed Versus Variable Mortgage Terms Compared

- Common Mistakes When Choosing A Term

Key Takeaways

| Point | Details |

|---|---|

| Understand Mortgage Terms | Mortgage terms, typically 15 to 30 years, significantly influence monthly payments and total interest paid. Choosing the right term requires analyzing personal financial circumstances and long-term goals. |

| Shorter vs. Longer Terms | Shorter terms often have lower interest rates but higher monthly payments, while longer terms provide lower monthly payments but result in higher total interest. Balance your payment structure with your financial ability. |

| Fixed vs. Variable Rates | Fixed-rate mortgages offer stability with consistent payments, whereas variable-rate mortgages may start lower but carry the risk of increasing payments. Assess your risk tolerance when making this decision. |

| Avoid Common Pitfalls | First-time buyers should avoid focusing solely on monthly payments, ensuring to consider total loan costs and potential rate fluctuations to make well-informed decisions. |

Mortgage Term Defined and Common Myths

A mortgage term represents the duration agreed between a borrower and lender for repaying a home loan, typically ranging from 15 to 30 years. When first-time homebuyers in Canada explore financing options, understanding this fundamental concept becomes critical. The mortgage fundamentals involve transferring property interest as security for loan repayment, which impacts overall financial planning.

Common myths about mortgage terms can significantly mislead potential homeowners. Many people incorrectly assume that shorter terms always mean lower total interest payments or that longer terms are universally disadvantageous. In reality, mortgage terms involve nuanced considerations:

- Shorter terms (15 years) typically offer lower interest rates

- Longer terms (30 years) provide lower monthly payments

- Term length affects total interest paid over the loan’s lifetime

- Prepayment options and penalties vary by specific loan agreement

First-time buyers should recognize that mortgage terms are not one-size-fits-all financial products. Each term presents unique advantages depending on individual financial circumstances, income stability, and long-term housing goals. Some borrowers might prioritize lower monthly payments, while others aim to minimize total interest expenditure.

Pro Tip: Mortgage Term Strategy: Consult a professional mortgage broker to model multiple term scenarios using your specific financial profile, allowing you to understand potential long-term financial implications before committing to a specific mortgage structure.

Different Mortgage Term Lengths Explained

Mortgage term lengths play a critical role in determining financial strategy for first-time homebuyers. Mortgage terms globally vary, with standard durations differing across countries, but in North America, 15- and 30-year terms dominate the residential lending landscape. Understanding these options requires careful analysis of personal financial goals and current economic conditions.

Typical mortgage term lengths offer distinct advantages and challenges:

-

15-Year Mortgage

- Lower overall interest payments

- Faster equity building

- Higher monthly payment requirements

- Ideal for buyers with stable, higher incomes

-

30-Year Mortgage

- Lower monthly payments

- Greater financial flexibility

- Higher total interest paid over loan lifetime

- Better suited for buyers seeking budget predictability

Beyond traditional terms, some lenders offer alternative durations like 20-year or 40-year mortgages. These specialized terms can provide unique benefits for borrowers with specific financial situations. The key is matching the mortgage term to individual income patterns, long-term housing plans, and overall financial health.

Financial experts recommend comprehensive analysis before selecting a mortgage term. Factors such as expected income trajectory, potential career changes, and retirement planning should all factor into the decision-making process.

Here’s a summary comparing the long-term financial effects of different mortgage term lengths:

| Mortgage Term | Typical Borrower Profile | Total Interest Paid | Equity Build Speed |

|---|---|---|---|

| 15-Year | High, stable income | Lower overall | Very fast |

| 20-Year | Moderate, steady income | Moderate | Faster than 30-year |

| 30-Year | Budget-focused or variable income | Highest overall | Slowest |

Pro Tip: Mortgage Term Selection Strategy: Request detailed amortization schedules from multiple lenders to visually compare how different term lengths impact your total loan cost and monthly obligations.

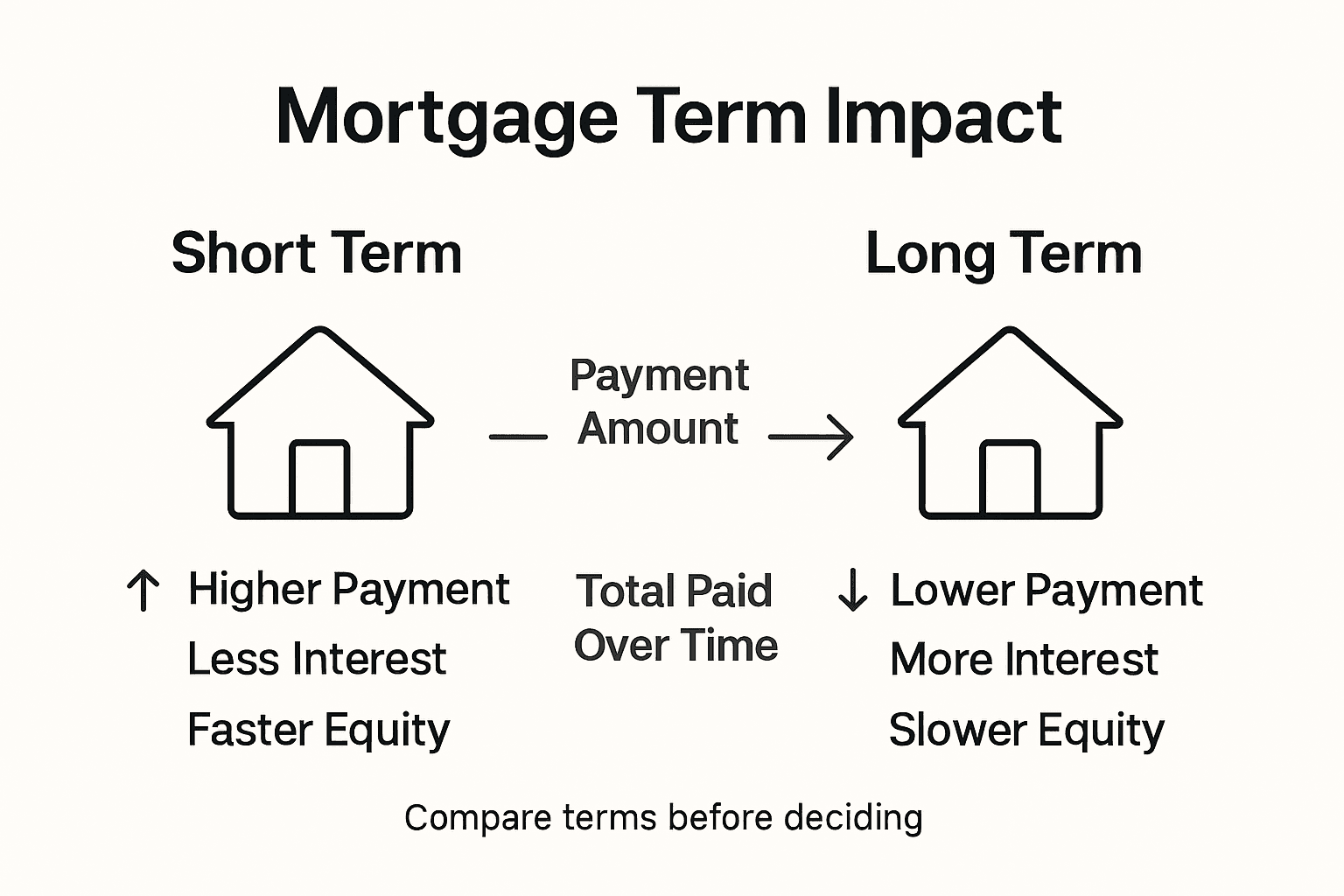

How Mortgage Term Affects Monthly Payments

Understanding how mortgage terms impact monthly payments is crucial for first-time homebuyers navigating the complex world of real estate financing. Longer mortgage terms result in significantly lower monthly payments, making homeownership more accessible, though they come with important financial trade-offs that require careful consideration.

The mathematical relationship between mortgage term length and monthly payments is straightforward but profound:

-

15-Year Mortgage Dynamics

- Higher monthly payment amounts

- Substantially reduced total interest paid

- Faster principal balance reduction

- Accelerated home equity accumulation

-

30-Year Mortgage Dynamics

- Lower monthly payment amounts

- Extended time for principal repayment

- Increased total interest expenditure

- Greater short-term financial flexibility

Homebuyers must recognize that monthly payment calculations involve complex interactions between principal, interest rates, loan duration, and additional factors like property taxes and insurance. A 30-year mortgage might reduce monthly obligations by 25-40% compared to a 15-year term, providing breathing room in household budgets but ultimately costing more in long-term interest.

Financial experts emphasize the importance of aligning mortgage terms with personal financial goals. Factors such as income stability, future earning potential, and overall financial strategy should guide the decision-making process.

Pro Tip: Monthly Payment Strategy: Create detailed spreadsheet comparisons of different mortgage terms, factoring in your specific income, anticipated career trajectory, and long-term financial objectives to make an informed selection.

Fixed Versus Variable Mortgage Terms Compared

First-time homebuyers face a critical decision when choosing between fixed and variable mortgage terms, each presenting unique financial implications. Fixed-rate mortgages offer stability with unchanging payments, while variable-rate mortgages can start with lower rates but carry the risk of increasing payments, making the selection a nuanced financial strategy.

Key characteristics of each mortgage type reveal distinct advantages and potential risks:

-

Fixed-Rate Mortgage

- Consistent monthly payments

- Predictable budgeting

- Protection against interest rate fluctuations

- Higher initial interest rates

- Ideal for risk-averse borrowers

-

Variable-Rate Mortgage

- Lower initial interest rates

- Potential for reduced total interest payments

- Payments can increase with market changes

- Greater financial uncertainty

- Suitable for borrowers comfortable with risk

The selection between fixed and variable rates depends on multiple factors, including personal risk tolerance, current economic conditions, and individual financial stability. Borrowers must carefully evaluate their income predictability, long-term housing plans, and ability to absorb potential payment increases when making this critical decision.

Below is a side-by-side comparison of fixed-rate and variable-rate mortgage features:

| Feature | Fixed-Rate Mortgage | Variable-Rate Mortgage |

|---|---|---|

| Payment Predictability | Constant through entire term | Can fluctuate over time |

| Initial Interest Level | Slightly higher at start | Lower at start |

| Risk Level | Low, stable environment | Higher, depends on market |

| Ideal Borrower | Values stability, risk-averse | Flexible, comfortable with uncertainty |

Economic indicators and market trends play a significant role in determining the most advantageous mortgage structure. Interest rate forecasts, inflation expectations, and broader economic conditions should inform this important financial choice.

Pro Tip: Rate Comparison Strategy: Request comprehensive rate comparisons from multiple lenders, analyzing potential payment scenarios over 5- and 10-year periods to understand the full financial impact of your mortgage term selection.

Common Mistakes When Choosing a Term

First-time homebuyers frequently encounter pitfalls when selecting mortgage terms that can significantly impact their long-term financial health. Borrowers often overlook the critical implications of variable interest rates, naively assuming initial low rates will remain constant, which can lead to unexpected financial strain and potential economic challenges.

Most common mistakes in mortgage term selection include:

-

Ignoring Total Cost Perspective

- Focusing solely on monthly payments

- Neglecting cumulative interest expenses

- Failing to calculate long-term financial implications

- Underestimating potential rate fluctuations

-

Risk Miscalculation

- Overestimating personal income stability

- Underestimating potential economic changes

- Choosing terms without comprehensive financial modeling

- Disregarding personal risk tolerance

The psychological tendency to prioritize short-term affordability over long-term financial strategy can prove devastating. Many borrowers select variable-rate mortgages based on initially attractive low rates, without fully understanding the potential for significant payment increases during economic shifts. This approach can transform what seems like an affordable mortgage into a financial burden.

Financial experts recommend comprehensive scenario planning that goes beyond current economic conditions. Potential job changes, market volatility, and personal life transitions should all factor into mortgage term selections. Borrowers must develop a holistic view of their financial landscape, considering not just current income but potential future scenarios.

Pro Tip: Term Selection Strategy: Create multiple financial projection models that simulate different interest rate scenarios, ensuring you understand potential payment variations before committing to a specific mortgage structure.

Find Your Perfect Mortgage Term with Expert Guidance

Choosing the right mortgage term can feel overwhelming, especially with all the myths and financial risks involved. Whether you are worried about locking into a fixed or variable rate or unsure if a 15-year or 30-year term fits your budget and long-term goals, you are not alone. Many first-time buyers struggle to balance monthly payment affordability with minimizing total interest paid.

At Craigburn Capital, we specialize in tailoring mortgage solutions that fit your unique financial profile and future plans. Our team understands critical concepts like mortgage term length, payment predictability, and risk tolerance so we can help you avoid common mistakes when selecting your mortgage.

Take control of your homebuying journey and protect your financial future by partnering with mortgage experts who provide personalized advice and access to competitive rates, including exclusive offers not always advertised. Start with a free consultation at Craigburn Capital and explore how different mortgage terms impact your monthly payments and long-term costs so you can buy your first home with confidence. For more insights on navigating first-time buyer challenges, visit our blog and learn how our special programs can support your needs.

Frequently Asked Questions

What is a mortgage term?

A mortgage term is the duration agreed upon between a borrower and lender for repaying a home loan, typically ranging from 15 to 30 years.

How does the length of a mortgage term affect monthly payments?

Longer mortgage terms result in lower monthly payments compared to shorter terms, but they also lead to higher total interest payments over the life of the loan.

What are the main differences between fixed-rate and variable-rate mortgages?

Fixed-rate mortgages offer stable monthly payments and predictability, while variable-rate mortgages may start with lower rates but can fluctuate based on market conditions, presenting financial uncertainty.

What common mistakes should first-time homebuyers avoid when selecting a mortgage term?

First-time homebuyers should avoid focusing solely on monthly payments, overlooking total costs, miscalculating personal risk, and failing to plan for potential changes in income or economic conditions.