B-Lender Mortgages: Solutions for Imperfect Credit

More than one in five American homebuyers turns to non-traditional lenders when standard banks say no. For anyone facing unique income situations or past credit hiccups, understanding these alternatives can open new doors to homeownership. This guide breaks down how B-Lender mortgages give Americans flexible solutions that fit real life—even when traditional requirements seem out of reach.

Table of Contents

- What Sets A-B-Lender Mortgage Apart

- Types Of B-Lenders And Loan Scenarios

- Borrower Requirements And Eligibility Factors

- Interest Rates, Costs, And Key Risks

- Comparing B-Lender Mortgages To Other Options

Key Takeaways

| Point | Details |

|---|---|

| B-Lender Mortgages Offer Flexibility | B-Lenders cater to borrowers with non-standard financial profiles, such as self-employed individuals and those with credit challenges, providing an alternative to traditional lending. |

| Higher Costs and Interest Rates | B-Lender mortgages generally have higher interest rates and upfront fees to account for increased risk, making it essential for borrowers to evaluate total lifetime costs. |

| Comprehensive Financial Assessment | Eligibility for B-Lender mortgages involves detailed evaluations including income stability and overall financial health, moving beyond mere credit scores. |

| Diverse Lender Types Available | Borrowers can choose from various B-Lender types, including trust companies, credit unions, and alternative mortgage lenders, each offering unique strengths and tailored loan options. |

What Sets a B-Lender Mortgage Apart

B-Lender mortgages represent a critical alternative for borrowers who find themselves outside traditional lending parameters. Unlike conventional bank mortgages, these specialized lending solutions provide flexibility for individuals with non-standard financial profiles such as self-employed professionals, those with imperfect credit histories, or unconventional income streams.

The fundamental distinction of B-Lender mortgages lies in their more accommodating approval criteria. While traditional mortgage lenders typically require pristine credit scores and consistent employment documentation, B-Lenders evaluate borrowers through a more holistic lens. They consider factors beyond credit score, including:

- Overall financial health

- Income stability

- Asset portfolio

- Future earning potential

- Specific circumstances causing credit challenges

Interest rates for B-Lender mortgages are generally higher to compensate for the increased risk, but they provide a critical pathway to homeownership for borrowers who might otherwise be shut out of the real estate market. These lenders understand that credit challenges don’t always reflect an individual’s true financial responsibility or ability to manage mortgage payments.

Pro Tip: Strategic Credit Preparation: Before applying for a B-Lender mortgage, obtain a comprehensive credit report, address any outstanding negative items, and be prepared to provide detailed documentation explaining past financial challenges to improve your approval chances.

Types of B-Lenders and Loan Scenarios

B-Lenders encompass a diverse range of financial institutions that provide alternative mortgage solutions beyond traditional bank lending. These specialized lenders include private lending organizations that focus on creating flexible financing options for borrowers with unique financial circumstances.

The primary types of B-Lenders typically fall into three distinct categories:

- Trust Companies: Financial institutions offering more flexible lending criteria

- Credit Unions: Member-owned financial cooperatives with personalized lending approaches

- Alternative Mortgage Lenders: Specialized firms focusing exclusively on non-traditional mortgage products

Each B-Lender type presents specific loan scenarios tailored to different borrower needs. Trust companies might specialize in self-employed income verification, while credit unions often provide more personalized assessment of an individual’s financial history. Alternative mortgage lenders frequently develop innovative products for borrowers with complex income streams or credit challenges.

These lenders evaluate potential borrowers through a comprehensive lens that goes beyond traditional credit scoring. They assess factors such as income stability, future earning potential, and overall financial health rather than relying solely on credit history. This approach opens mortgage opportunities for professionals with non-traditional income, recent immigrants, and individuals recovering from past financial difficulties.

Here’s a concise summary of key differences between B-Lender mortgage types:

| Lender Type | Typical Borrower | Unique Strength |

|---|---|---|

| Trust Company | Self-employed professionals | Flexible income verification |

| Credit Union | Members with diverse backgrounds | Personalized loan assessment |

| Alternative Mortgage Lender | Non-traditional income earners | Innovative mortgage solutions |

Pro Tip: Strategic Lender Selection: Research multiple B-Lender options, compare their specific lending criteria, and prepare a detailed financial portfolio that highlights your strengths beyond traditional credit metrics to improve your mortgage approval chances.

Borrower Requirements and Eligibility Factors

Navigating B-Lender mortgage eligibility requires understanding a comprehensive set of requirements that differ significantly from traditional bank lending standards. Borrowers seeking mortgage qualification strategies must prepare for a more holistic financial assessment that goes beyond simple credit scores.

Key eligibility factors for B-Lender mortgages typically include:

- Income Verification: Flexible documentation options for self-employed or non-traditional income earners

- Credit History: More lenient credit score requirements compared to traditional lenders

- Debt Service Ratios: Comprehensive evaluation of overall financial health

- Down Payment: Often requiring higher down payment percentages

- Property Type: Willingness to consider diverse property categories

B-Lenders evaluate borrowers through a multifaceted lens that considers past financial challenges as potential learning experiences rather than permanent disqualifiers. They recognize that credit challenges can stem from temporary life circumstances such as medical emergencies, job loss, or unexpected financial disruptions.

The documentation requirements for B-Lender mortgages are typically more comprehensive than traditional lending. Borrowers should be prepared to provide detailed financial records, including tax returns, bank statements, proof of income, and a comprehensive explanation of any previous credit issues. This thorough approach allows B-Lenders to make more nuanced lending decisions based on individual financial narratives.

Pro Tip: Financial Documentation Preparation: Compile a comprehensive financial portfolio before applying, including detailed income documentation, explanatory letters for past credit challenges, and a clear breakdown of your current financial stability to maximize your approval potential.

Interest Rates, Costs, and Key Risks

B-Lender mortgages come with a unique financial landscape characterized by higher interest rates and more complex cost structures compared to traditional bank lending. Understanding the intricacies of mortgage terms becomes crucial for borrowers navigating these alternative financing options.

Interest rates for B-Lender mortgages typically range higher than conventional loans, reflecting the increased risk and flexibility these lenders provide. Key cost considerations include:

- Interest Rates: Generally 1-3% higher than traditional bank rates

- Origination Fees: Additional upfront costs ranging from 1-3% of loan value

- Legal and Administrative Fees: More comprehensive documentation requirements

- Prepayment Penalties: Often more stringent than traditional mortgage terms

- Refinancing Costs: Potentially higher transaction expenses

The primary risks associated with B-Lender mortgages extend beyond standard financial considerations. Borrowers must carefully evaluate potential long-term financial implications, including the possibility of higher cumulative costs over the mortgage’s lifetime. These lenders often structure loans with more complex terms that can include variable interest rates, shorter fixed-rate periods, and more aggressive adjustment mechanisms.

While B-Lender mortgages provide critical financing options for borrowers with non-traditional financial profiles, they require a sophisticated understanding of potential financial trade-offs. The increased flexibility comes with a corresponding increase in financial complexity, demanding careful analysis of total borrowing costs, potential future rate adjustments, and overall long-term financial strategy.

Use this table to evaluate costs and risks before choosing a B-Lender mortgage:

| Financial Aspect | B-Lender Mortgage | Traditional Bank |

|---|---|---|

| Rate Range | 1-3% higher than banks | Lowest market rates |

| Upfront Fees | 1-3% origination + legal | Minimal fees overall |

| Loan Terms | Often shorter, more variable | Long fixed-rate periods |

| Risk Profile | Higher cost, flexible approval | Lower risk, strict approval |

Pro Tip: Cost Comparison Strategy: Calculate the total lifetime cost of a B-Lender mortgage, including all fees and potential rate adjustments, and compare it against traditional lending options to make a fully informed financial decision.

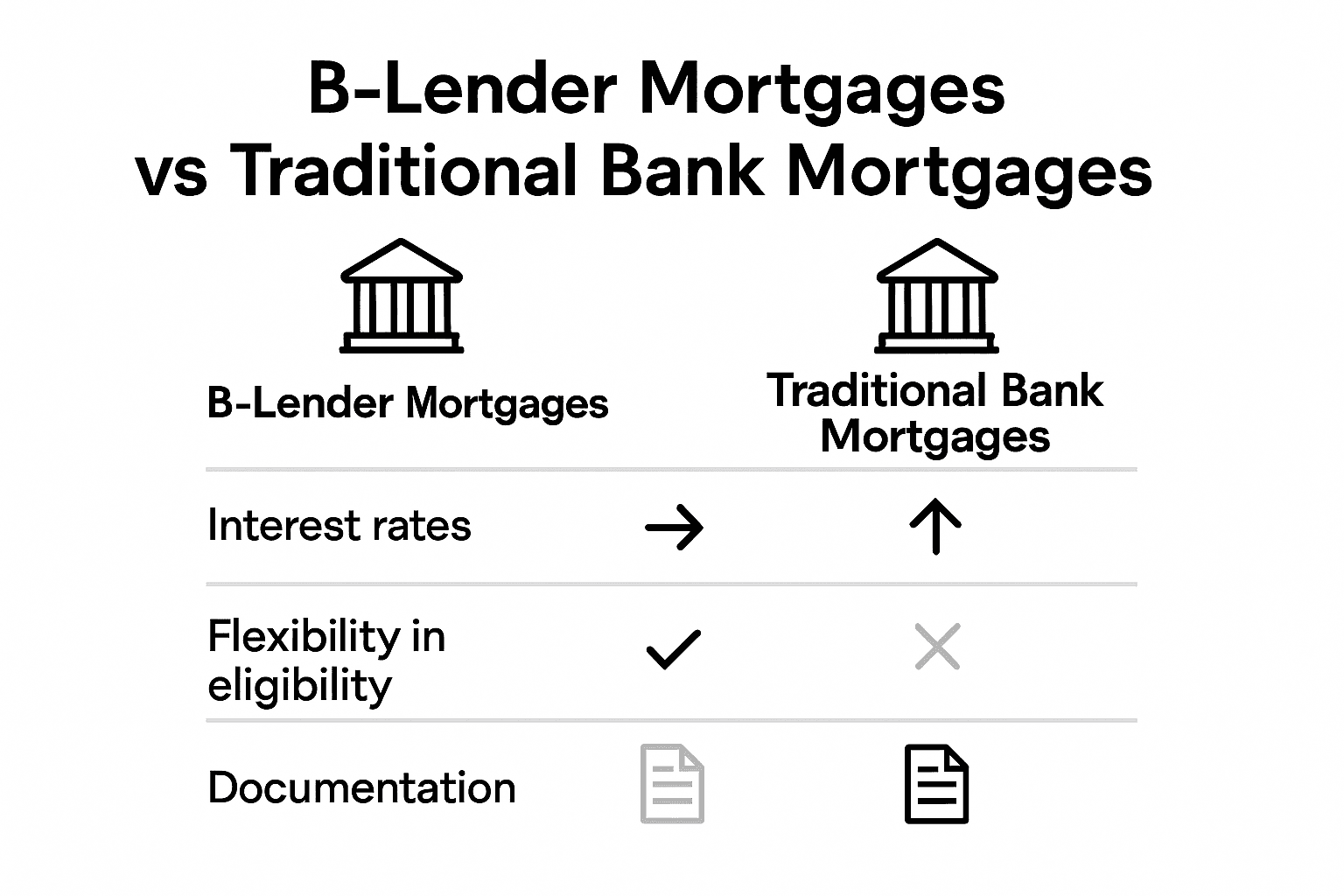

Comparing B-Lender Mortgages to Other Options

Navigating mortgage options requires a strategic understanding of how different lending approaches compare and contrast. Borrowers with non-traditional financial backgrounds often find specialized mortgage solutions crucial for achieving homeownership when conventional routes prove challenging.

Key comparative points between B-Lender and traditional mortgage options include:

-

Approval Criteria:

- Traditional Banks: Strict credit score requirements

- B-Lenders: Flexible, holistic financial assessment

-

Interest Rates:

- Traditional Banks: Lower rates for ideal borrowers

- B-Lenders: Higher rates reflecting increased lending flexibility

-

Documentation Requirements:

- Traditional Banks: Standardized, rigid documentation

- B-Lenders: Comprehensive, personalized financial review

-

Borrower Profiles:

- Traditional Banks: Prefer low-risk, standard income profiles

- B-Lenders: Accommodate self-employed, recent immigrants, credit-challenged individuals

Unlike traditional lenders who often apply a one-size-fits-all approach, B-Lenders evaluate borrowers through a more nuanced lens. They recognize that financial challenges do not necessarily indicate future lending risk, instead focusing on overall financial health, income stability, and potential for financial recovery.

The primary trade-off with B-Lender mortgages involves higher costs balanced against increased accessibility. While interest rates and fees are typically more expensive, these loans provide a critical pathway to homeownership for borrowers who would otherwise be excluded from the real estate market.

Pro Tip: Comprehensive Comparison Strategy: Conduct a detailed lifetime cost analysis comparing B-Lender and traditional mortgage options, factoring in interest rates, fees, and potential future refinancing opportunities to make an informed financial decision.

Unlock Homeownership With Expert Help for Imperfect Credit

Struggling to secure a mortgage because of imperfect credit or a non-traditional income? You are not alone. Many face the challenge of rigid lending requirements that overlook their true financial potential. The solution lies in a deeper financial understanding and flexible mortgage options like those discussed in the article on B-Lender mortgages. These specialized loans take into account your whole financial story and open doors when traditional banks close them.

Explore how private lending and alternative mortgage programs at Craigburn Capital can offer you tailored solutions suited to your unique financial situation. Our dedicated team helps self-employed professionals, individuals recovering from credit challenges, and others overlooked by conventional lenders find competitive interest rates and personalized mortgage plans. Don’t wait to take control of your home buying journey. Visit our site now to learn more about mortgage qualification strategies and start your path to approval today.

Frequently Asked Questions

What is a B-Lender mortgage?

A B-Lender mortgage is an alternative financing solution specifically designed for borrowers who may not meet the strict criteria of traditional lenders, such as those with imperfect credit, self-employed individuals, or unique income streams.

How do B-Lender mortgage eligibility requirements differ from traditional lenders?

B-Lender requirements are generally more flexible, assessing factors like overall financial health, income stability, and future earning potential, rather than focusing solely on credit scores and standard documentation.

Are interest rates for B-Lender mortgages higher than traditional mortgages?

Yes, interest rates for B-Lender mortgages typically range from 1-3% higher than conventional bank rates, reflecting the increased risk associated with these loans.

What should I prepare before applying for a B-Lender mortgage?

Before applying, obtain a comprehensive credit report, gather detailed financial records such as tax returns and bank statements, and be ready to explain any past credit challenges to improve your chances of approval.

Recommended

- Complete Guide to Credit Scores in Mortgages – Craigburn Capital

- Mortgage Terms Explained: Keys to Smarter Home Buying – Craigburn Capital

- Private Lending Explained: Benefits, Types, and Risks – Craigburn Capital

- Non-Traditional Income Mortgages Explained: Complete Guide – Craigburn Capital

- Roofing Financing Options Explained: Complete Guide – J. A. Kelly Contracting Services

- Pagare l’impianto dentale a rate: quali opzioni finanziarie esistono in Italia? – dentalnetcare.it