Complete Guide to Credit Scores in Mortgages

More than 80 percent of american home buyers find their credit score shapes not just their mortgage approval, but also how much they pay each month. Choosing the right path in the home loan process can be confusing when every lender seems to focus on a different number. Understanding how your credit score works in mortgages turns confusion into confidence and can help you secure better rates that save real money over time.

Table of Contents

- What Is A Credit Score In Mortgages?

- How Lenders Use Credit Scores

- Impact Of Credit Score On Approval And Rates

- Improving Credit Score For Mortgage Success

- Common Credit Score Mistakes To Avoid

Key Takeaways

| Point | Details |

|---|---|

| Understanding Credit Scores | A credit score reflects your financial trustworthiness and affects mortgage qualification and interest rates. Scores range from 300 to 850, with higher scores leading to better loan terms. |

| Lender Evaluation | Lenders assess credit scores from major agencies to determine loan approval, interest rates, and payment requirements. A strong score is essential for favorable mortgage terms. |

| Impact on Approval and Rates | Higher credit scores improve the likelihood of loan approval and access to competitive interest rates, potentially saving thousands over the mortgage term. |

| Avoiding Credit Pitfalls | Common mistakes include missing payments and opening multiple credit accounts before applying for a mortgage. Proactive credit management is crucial for mortgage success. |

What Is a Credit Score in Mortgages?

A credit score is a powerful numerical snapshot that reveals your financial trustworthiness to mortgage lenders. According to Consumer Finance, this score serves as a predictive tool that estimates how likely you are to repay debts on time, directly impacting your mortgage qualification and potential interest rates.

Typically ranging from 300 to 850, credit scores represent a complex calculation of your financial history and behaviors. FINRA explains that lenders use these scores to evaluate the risk of lending money, with higher scores signaling lower perceived risk and potentially unlocking more favorable loan terms.

Key Components of a Credit Score Include:

- Payment history

- Total debt levels

- Length of credit history

- Types of credit accounts

- Recent credit inquiries

Understanding your credit score isn’t just about numbers—it’s about positioning yourself strategically in the mortgage marketplace. A strong score can translate into significant savings, potentially reducing your long-term borrowing costs by securing more competitive interest rates. For those looking to maximize their mortgage potential, your credit score Archives can provide additional insights into improving your financial profile.

How Lenders Use Credit Scores

Credit scores serve as the primary financial fingerprint that mortgage lenders use to assess borrower reliability. Consumer Finance reveals that lenders meticulously examine scores from all three major credit reporting agencies—Equifax, Experian, and TransUnion—typically using the middle score to make critical lending decisions.

Federal Housing Finance Agency (FHFA) explains that credit scores are integral throughout the mortgage process, influencing everything from initial loan underwriting to final pricing strategies. Lenders strategically use these scores to evaluate risk, determine loan eligibility, and customize interest rates that reflect a borrower’s financial credibility.

Key Ways Lenders Analyze Credit Scores:

- Determining loan approval probability

- Setting personalized interest rates

- Assessing down payment requirements

- Evaluating overall financial risk

- Calculating potential mortgage terms

To maximize your mortgage potential, understanding how lenders interpret credit scores is crucial. A strong score can unlock more favorable lending terms, potentially saving thousands over your loan’s lifetime. For those interested in exploring unique financing options, Transunion Archives can provide additional insights into credit score intricacies and their impact on mortgage opportunities.

Impact of Credit Score on Approval and Rates

Consumer Finance reveals a critical truth about mortgages: your credit score directly impacts both your loan approval chances and the interest rates you’ll be offered. A higher score doesn’t just open doors—it can potentially save you thousands of dollars over the life of your mortgage by securing more favorable lending terms.

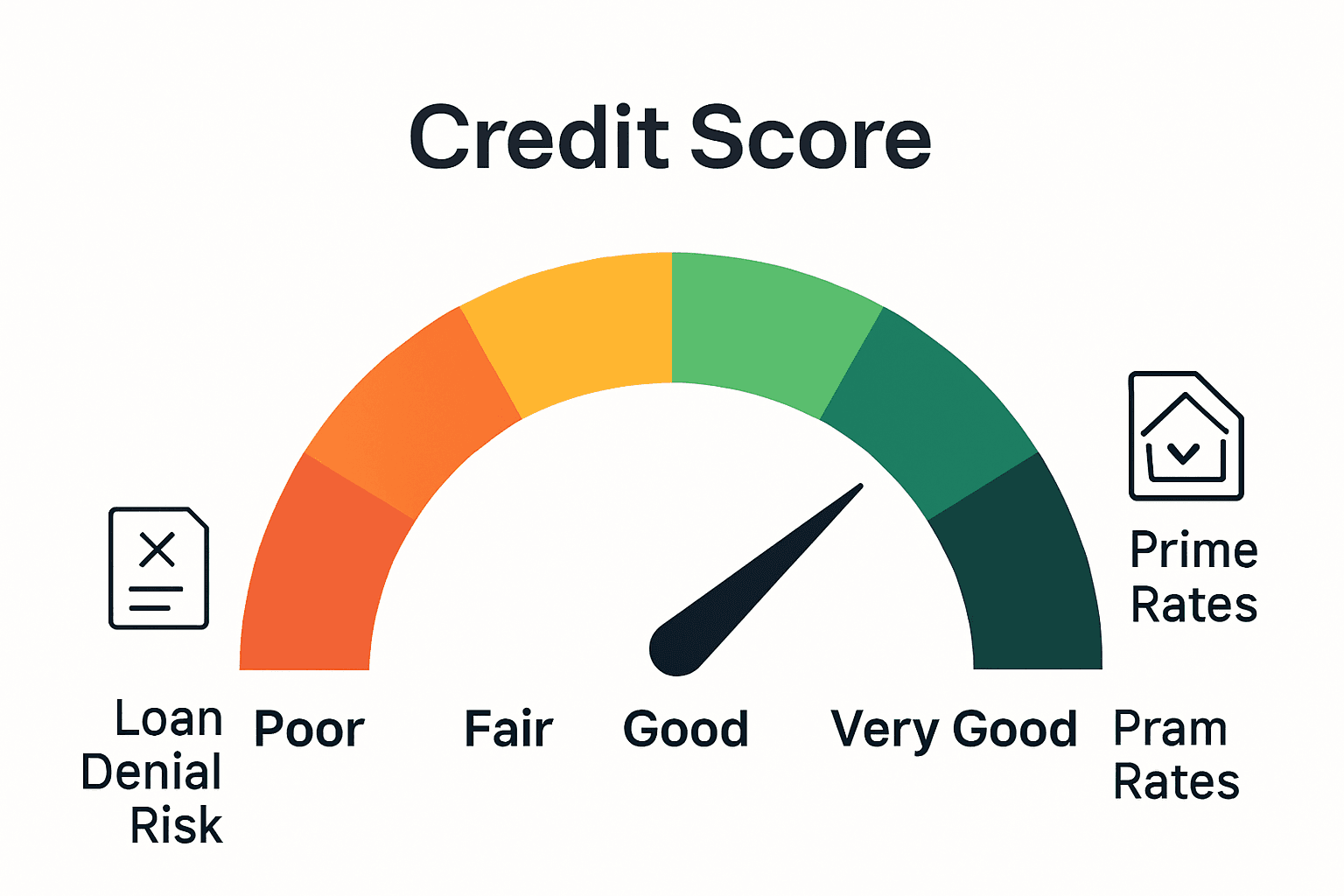

According to the Government Accountability Office (GAO), mortgage institutions establish clear credit score thresholds that dramatically influence loan accessibility. Borrowers with scores above 660 are typically viewed as low-risk, while those below 620 may encounter significant challenges in loan approval, potentially facing higher interest rates or requiring additional documentation.

Credit Score Impact Breakdown:

- Scores 760-850: Excellent (Prime rates)

- Scores 700-759: Very Good (Competitive rates)

- Scores 660-699: Good (Standard rates)

- Scores 620-659: Fair (Higher interest rates)

- Scores below 620: Poor (Potential loan denial)

Understanding these nuances can transform your mortgage strategy.

A strategic approach to improving your credit score can mean the difference between an affordable loan and a financially challenging mortgage. For those exploring specialized financing options, 100% financing Archives can provide additional insights into navigating complex lending landscapes.

Improving Credit Score for Mortgage Success

Improving your credit score is a strategic process that can dramatically enhance your mortgage opportunities. Consumer Finance recommends a proactive approach, starting with a comprehensive review of your credit reports to identify and dispute any potential errors that might be dragging down your score.

InCharge highlights several key strategies for boosting your credit profile before applying for a mortgage. These include maintaining consistent on-time payments, strategically reducing credit card balances, and carefully managing your credit mix to demonstrate financial responsibility to potential lenders.

Top Strategies for Credit Score Improvement:

- Pay all bills consistently and on time

- Keep credit card balances below 30% of your limit

- Avoid opening new credit accounts before mortgage application

- Maintain a diverse credit history

- Regularly monitor your credit report for accuracy

For those seeking a comprehensive roadmap to mortgage readiness, How to Qualify for a Mortgage: Step-by-Step Guide for Buyers can provide additional insights into transforming your financial profile and positioning yourself as an ideal mortgage candidate.

Common Credit Score Mistakes to Avoid

Consumer Finance reveals several critical credit mistakes that can devastate your mortgage prospects. Applying for multiple new credit accounts in quick succession, missing payment deadlines, and maintaining high credit card balances are red flags that can dramatically lower your credit score and potentially derail your home buying dreams.

FINRA emphasizes the importance of proactive credit management. Neglecting to regularly check your credit reports for inaccuracies, allowing late payments to accumulate, and consistently maxing out credit limits can create long-lasting damage to your financial reputation that extends far beyond a simple numerical score.

Top Credit Score Pitfalls to Dodge:

- Opening multiple credit lines before mortgage application

- Missing payment due dates

- Maxing out credit card limits

- Ignoring credit report errors

- Closing old credit accounts unexpectedly

- Cosigning loans without careful consideration

Navigating the complex world of credit requires strategic thinking and careful planning. For those seeking deeper insights into credit management, 5 c’s of credit Archives can provide additional strategies to strengthen your financial profile and improve your mortgage readiness.

Take Control of Your Mortgage Journey with Expert Guidance

Navigating the complex world of credit scores can feel overwhelming, especially when your mortgage approval and interest rates hang in the balance. This article has shown how crucial your credit score is in securing the best loan terms and avoiding costly mistakes. If you are aiming to improve your credit profile or understand how lenders assess your financial trustworthiness, you need personalized solutions tailored to your unique situation.

At Craigburn Capital, we specialize in turning credit challenges into home buying opportunities. Whether you are a first-time buyer, self-employed, or working to rebuild a less-than-perfect credit history, our expert team offers exclusive mortgage programs and competitive interest rates designed just for you. Don’t let credit score concerns hold you back any longer. Visit Craigburn Capital now to explore how our customized lending solutions can make mortgage success possible. Start taking the right steps today by reading How to Qualify for a Mortgage: Step-by-Step Guide for Buyers and deepen your understanding with insights from 100% financing Archives.

Empower yourself with the knowledge and support you deserve. Contact Craigburn Capital and unlock mortgage options that fit your financial goals.

Frequently Asked Questions

What is a credit score and how does it affect my mortgage eligibility?

A credit score is a numerical representation of your financial trustworthiness, ranging from 300 to 850. It affects your mortgage eligibility as lenders use it to assess risk, determining your loan approval and interest rates based on your score.

How can I improve my credit score before applying for a mortgage?

To improve your credit score, consistently pay all bills on time, keep credit card balances below 30% of your limit, avoid opening new credit accounts just before your mortgage application, and regularly monitor your credit report for errors.

What are the typical credit score ranges and their impact on mortgage rates?

Credit scores typically fall into ranges: 760-850 (Excellent), 700-759 (Very Good), 660-699 (Good), 620-659 (Fair), and below 620 (Poor). Higher scores correspond to lower perceived risk and can lead to more favorable interest rates and loan terms.

What common mistakes should I avoid to maintain a good credit score for my mortgage application?

Common mistakes include opening multiple new credit lines before applying, missing payment due dates, maxing out credit card limits, ignoring credit report errors, and unexpectedly closing old credit accounts, which can negatively affect your score.