What Is Home Equity and Why It Matters

Over 60 percent of American homeowners are building wealth every month without even realizing it. Understanding home equity can be a game changer for anyone trying to make the most of their property investment. Decoding how equity works helps you see your house as more than shelter. Get a clear, practical explanation of how American homeowners gain, use, and grow this hidden financial resource.

Table of Contents

- Home Equity Explained In Simple Terms

- How Home Equity Builds Over Time

- Common Ways To Access Home Equity

- Risks And Costs Of Using Home Equity

- Alternatives To Tapping Home Equity

Key Takeaways

| Point | Details |

|---|---|

| Understanding Home Equity | Home equity is the financial value homeowners possess in their property, calculated by deducting the mortgage balance from the market value. |

| Ways to Build Equity | Home equity grows through consistent mortgage payments and property appreciation, enhanced by smart home improvements. |

| Accessing Home Equity | Homeowners can access equity through home equity loans, HELOCs, or cash-out refinancing, but must evaluate risks and benefits. |

| Alternatives to Home Equity | Personal loans and budget optimization can provide financial relief without risking home ownership, offering safer pathways to access funds. |

Home Equity Explained in Simple Terms

Home equity represents the financial value a homeowner has accumulated in their property. It is essentially the portion of your home that you truly own, calculated by subtracting any outstanding mortgage balance from the property’s current market value.

Understanding home equity starts with recognizing how it grows. When you make mortgage payments, a portion goes toward reducing your principal balance, while property appreciation contributes additional value. First-time homebuyers can build equity through consistent mortgage payments and strategic property improvements that increase the home’s overall market value.

The concept of home equity is more than just a number. It functions as a powerful financial tool that homeowners can leverage for various purposes. Homeowners can potentially access their equity through methods like home equity loans or lines of credit, which provide flexible financing options for major expenses such as home renovations, debt consolidation, or educational investments. By understanding how home equity works, you transform your property from merely a living space into a dynamic financial asset that can support your long-term economic goals.

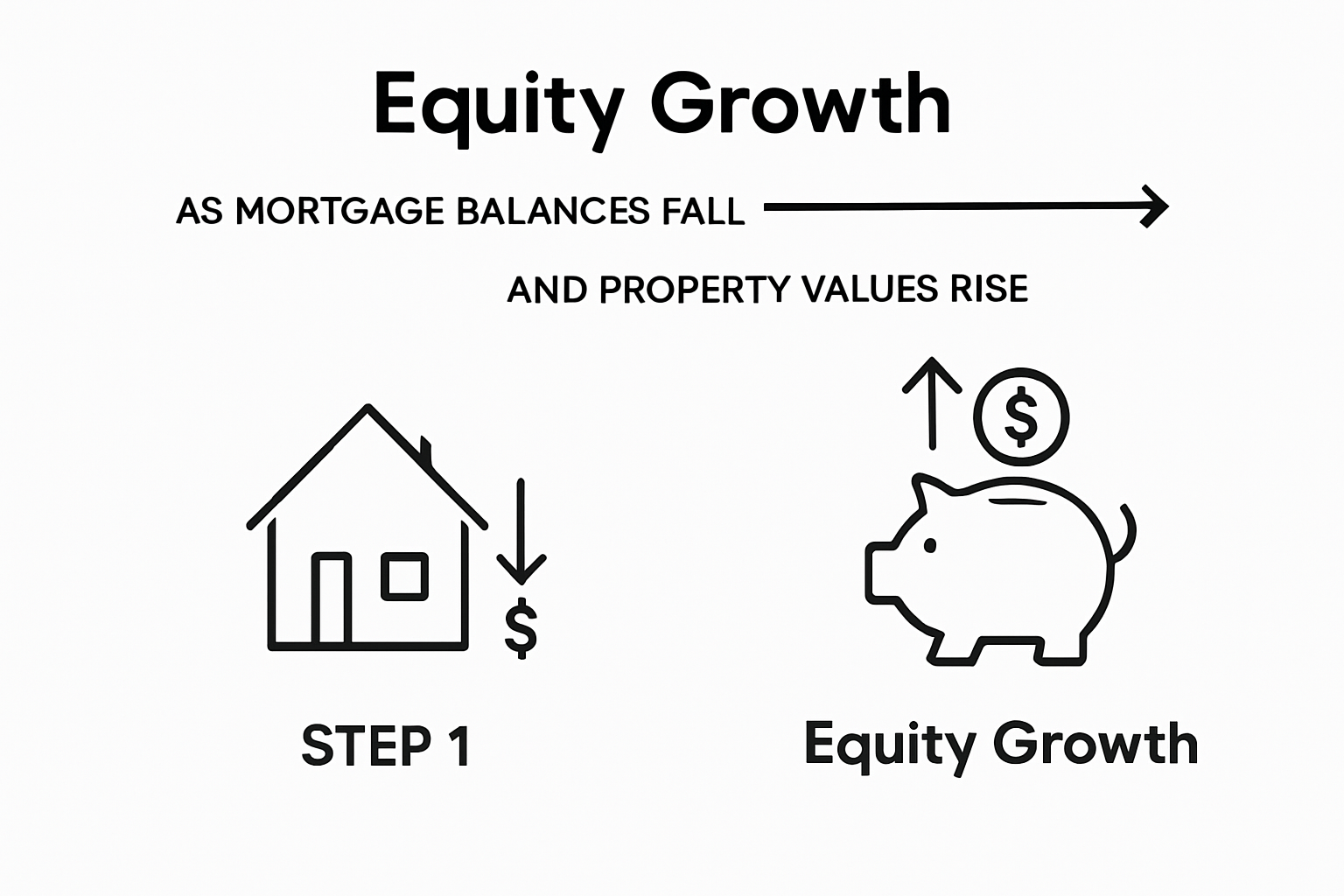

How Home Equity Builds Over Time

Home equity grows through two primary mechanisms: consistent mortgage payments and property value appreciation. When homeowners make monthly mortgage payments, a portion goes directly toward reducing the principal balance, which incrementally increases their ownership stake in the property.

Property appreciation plays a critical role in equity accumulation. Strategic home improvements can significantly boost a property’s market value, creating additional equity beyond standard mortgage payments. For example, targeted renovations like kitchen upgrades or energy-efficient installations can yield substantial returns by increasing the home’s overall market worth.

Homeowners can accelerate their equity growth through proactive strategies. Making extra principal payments, choosing shorter loan terms, and maintaining the property’s condition are powerful methods for building wealth. These approaches not only reduce outstanding mortgage balances faster but also position homeowners to maximize their long-term financial potential. By understanding and implementing these techniques, individuals can transform their home from a simple living space into a robust financial asset that contributes meaningfully to their personal wealth portfolio.

Common Ways to Access Home Equity

Home equity loans provide homeowners with multiple strategic options for accessing the value they have built in their property. First-time homebuyers and experienced property owners alike can leverage different financial instruments to tap into their home’s accumulated value.

Homeowners typically have three primary methods for accessing home equity: home equity loans, home equity lines of credit (HELOCs), and cash-out refinancing. Home equity loans offer a lump-sum payment with fixed interest rates, making them ideal for specific large expenses like home renovations or debt consolidation. HELOCs, in contrast, function more like a credit card, allowing borrowers to draw funds as needed up to a predetermined credit limit with typically variable interest rates.

Each equity access method comes with unique advantages and potential risks. Cash-out refinancing replaces the existing mortgage with a larger loan, enabling homeowners to receive the difference in cash. When considering these options, it’s crucial to evaluate factors such as current interest rates, personal financial goals, repayment capabilities, and potential tax implications. Careful assessment helps ensure that accessing home equity aligns with long-term financial strategies and doesn’t compromise overall financial stability.

Risks and Costs of Using Home Equity

Home equity borrowing comes with significant financial responsibilities that require careful evaluation. Guidelines for first-time buyers emphasize the critical importance of understanding potential risks before accessing home equity funds.

The most serious risk associated with home equity borrowing is the potential for foreclosure. When homeowners use their property as collateral, failure to meet repayment obligations can result in losing their home. This risk is particularly pronounced during economic downturns or personal financial challenges, making it essential to maintain a robust emergency fund and carefully assess repayment capabilities before accessing home equity.

Beyond foreclosure, home equity borrowing involves several additional financial considerations. Upfront costs can include origination fees, closing costs, and potential appraisal expenses that increase the overall borrowing expense. Variable interest rates, especially with home equity lines of credit, can lead to unpredictable monthly payments. Moreover, borrowing against home equity reduces the owner’s existing equity stake and can potentially leave homeowners underwater if property values decline, creating a scenario where they owe more than the home’s current market value.

Alternatives to Tapping Home Equity

Homeowners facing financial challenges have multiple strategies to explore before leveraging their home’s equity. Non-traditional income mortgage options can provide alternative pathways to accessing funds without risking home ownership.

Personal loans and credit card balance transfers represent two primary alternatives to home equity borrowing. These financial tools can help consolidate debt or cover unexpected expenses without putting your property at risk. Personal loans typically offer fixed interest rates and predictable repayment schedules, making them an attractive option for those seeking financial flexibility without using their home as collateral.

Budget optimization presents another powerful alternative to tapping home equity. By carefully reviewing monthly expenses, negotiating existing debt, and identifying potential savings opportunities, homeowners can often generate additional financial breathing room. Strategies like reducing discretionary spending, refinancing existing loans at lower interest rates, and exploring additional income streams can provide the financial relief sought through home equity borrowing, while preserving the long-term value of your most significant asset.

Turn Your Home Equity Into Financial Strength Today

Understanding home equity is the first step toward unlocking your home’s true financial potential. Whether you are looking to make strategic improvements, consolidate debt, or invest in your future, the challenge lies in accessing your equity wisely without risking your most valuable asset. At Craigburn Capital, we understand the concerns about repayment risks, foreclosure, and fluctuating interest rates discussed in the article “What Is Home Equity and Why It Matters.” That is why we specialize in personalized mortgage solutions designed to fit your unique financial situation.

Take control of your home equity with tailored lending options such as private lending, commercial financing, or specialized programs for first-time homebuyers. Visit Craigburn Capital now to explore how our competitive and exclusive rates can help you leverage your home’s value safely. Do not wait until financial pressure mounts. Act now to empower your financial future and build the security you deserve with expert guidance every step of the way.

Frequently Asked Questions

What is home equity?

Home equity is the financial value a homeowner has in their property, calculated by subtracting any outstanding mortgage balance from the property’s current market value.

How do I build equity in my home?

Equity can be built through consistent mortgage payments that reduce the principal balance, as well as property appreciation that increases the home’s market value. Strategic home improvements can also enhance equity.

What are the ways to access home equity?

Homeowners can access home equity through home equity loans, home equity lines of credit (HELOCs), and cash-out refinancing, each offering different features and benefits.

What are the risks associated with using home equity?

The primary risks include potential foreclosure if repayment obligations are not met, upfront costs associated with borrowing, and the possibility of being underwater on the mortgage if property values decline.